Opportunity in the rate curve

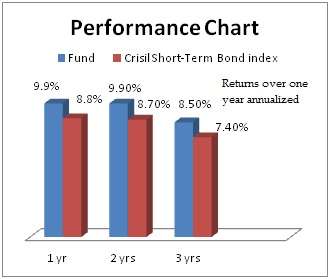

Investors with limited risk appetite and looking for opportunities in the debt product spectrum can consider investing in PineBridge India Short Term Fund. This fund has adeptly shuffled its portfolio to deliver 9.9 per cent in the last one year, higher than benchmark Crisil Short-Term Bond index’ return of 8.8 per cent.

Its three-year return of 8.6 per cent annually is also superior to the benchmark’s return of 7.4 per cent and category average of 8.1 per cent. While this is a short-term fund, that it has maintained a superior record for a longer period of three years, is an indication of well-timed moves, both in rising and falling interest rate scenarios.

Suitability

PineBridge India Short Term fund is suitable for investors with a time frame of 15-18 months and willing to take higher risks than liquid or ultra short-term funds. Consider investing lump sum in the fund now, if you have a goal at least 1.5 years away.

Among other short-term funds, a few such as Templeton India Short Term Income Plan and JP Morgan Short Term Income have delivered superior returns in the past and may do so again given their higher portfolio maturity.

But such higher average portfolio maturity and elevated exposure to bonds/debentures entails assuming higher risks.

While the said funds also remain investment worthy, our choice of PineBridge India Short Term Fund stems from the fund’s high exposure to less risky and more liquid certificates of deposits (CDs) from banks. That CDs may see a rally over the next month or two (read on to know how), enhances the fund’s chances of delivering well.

Added to this, PineBridge India Short Term is perhaps one of the few short-term funds that do not have an exit load. Simply put, you can exit any time, like you would with a liquid fund. That said, it would nevertheless be safer to stick to the time period mentioned by us, to reduce any impact of volatility and also enhance your returns.

Like all other debt funds, the fund would be taxed at your income tax slab for short-term capital gains of less than a year and at 10 per cent without indexation (20 per cent with indexation) for holdings of over a year.

Opportunity in the short end

Typically, when interest rates peak, most debt market institutional investors prefer to take exposure to long-end gilt funds, which will gain from a price rally, when rates fall. But we believe this may be a good time to play the short-end of the curve for the following reason: RBI data suggests that the liquidity pressure in the banking system remains; both Central and state government borrowing in the month of February only adds to the pressure.

Liquidity requirement is also set to be higher in the Month of March on account of advance tax payment by companies. Banks too, have been drawing down their liquidity as deposit growth has been lower than credit growth thus far this fiscal.

All this is likely to add to the pressure on short-term liquidity. That means run-up in the yield of short-term instruments such as CDs. More importantly, Indian banking system has been traditionally short of liquidity in the run up to March and the condition slowly eases post April. Such a trend is obvious when one looks at the bank CD rates from January – April of every year in the past few years. The rates typically start rising post January and ease post April. Tightening rates are already visible now with 12-month CD rates rising to 9.35 per cent (mid-February) from 8.8 per cent a month ago.

The data suggests that CD rates ease around April, thus providing some capital gains as rate declines trigger a price rally. Rate cuts, if any, in April, can also be expected to accentuate such a decline. But what if liquidity remains stiff and rates hold? Even then, the less than one-year bank CD holdings of PineBridge India Short Term are likely to ensure good accrual income (interest income from the CDs) if the fund simply holds them to maturity.

Portfolio and performance

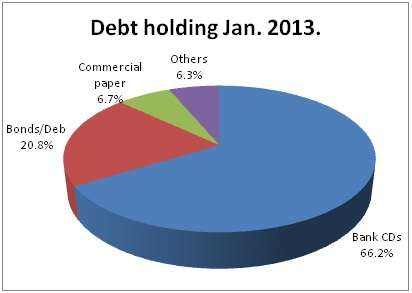

The fund held 66 per cent of its assets in bank CDs as of January, higher than top short-term funds from the Templeton and JP Morgan stable. Its average portfolio maturity (including bonds and commercial paper) was 1.62 years, as against the 2-plus years for a good number of peers. A lower portfolio maturity not only reduces risk but helps participate in gains arising from liquidity easing.

The fund holds only P1+ and AAA-rated instruments – these ratings being the top in each category.

PineBridge India Short Term Fund beat its benchmark 94 per of the times on a rolling one-year return basis for the past three years. The fund was launched in March 2008 and is managed by Mr Vikrant Mehta.

Hi Vidya,

Can you tell me the difference between primebridge india short term fund and IDFC super saver income fund. One is in short term category and other is an income fund, but for both the funds the benchmark is CRISIL short term bond. Then why the difference in classification. I think IDFC SSI fund is also having a duartion of <2.

Thanks,

karthik

Hello Karthik, IDFC SSI has two categories – IDFC SSI Short Term Plan and IDFC SSI Medium Term Plan. We are not sure which one you meant. IDFC SSI Short Term, has a less than 2-year portfolio maturity. However, it has higher exposure to bonds/debentures and does not also have a very inspiring track record.

IDFC Medium Term Plan is a more flexi-income fund (we gave a recommendation on this fund a while ago) . It can go for short-term maturities or go long based on debt market conditions. This fund too has Crisil Short Term Bond index. Because it is a flexi fund, its choice of index cannot be very accurate. In equity funds for example, a diversified fund will have Nifty as its index but it will very much invest in mid-cap stocks as well. The index choice in debt is also something similar. IDFC SSI Medium Term currently has a portfolio maturity of 3.27 years.

PineBridge India Short Term on the other hand does not have too much flexibility to go long. Hence it is essentially a short-term income fund. Its portfolio has more CDs than the other 2 and has a maturity of about 1.6 years. Hope this helps. – Tks Vidya

Thanks for the clarification.

I was refering to IDFC SSI Medium Term fund. In Continuum to the discussion we are having, what is your view on flexi debt funds. I remember reading a report in moneylife stating that flexi debt/income funds are not out of line except for expense ratio. Can you express your opinion/ views

Thanks,

Karthik

Hello Karthik, go-anywhere debt funds or dynamic or income funds are basically the counterparts of diversified equity fund in equity category. But as you stated earlier, these funds will have a key strategy, it could be playing the credit risk or interest rate risk or a combination of both or simply an accrual strategy or sometimes making capital gains from gilts. As they are more dynamically managed, their expense ratio will be slightly higher than say plain vanilla liquid funds or ultra-short-term funds. But much lower than equity funds. I am not sure what you meant by ‘out of line’ but certainly, these funds require a longer time frame and some appetite for risk by an investor when compared with short-term or liquid funds. If you take pure gilt funds, they are credit=safe but have high interest rate risk. But income funds would have a bit of both the risks but not too much. So they are indeed different in the debt category. tks, Vidya

Interesting suggestion Vidhya, but a logical one. As always its very informative and refreshing to read your recommendations than the run of the mill recommendations in other sites. Have a small request, can you review any of the FOFs in the market. For example, FT Life Stage FoF 40s. I see a mixed reaction about these and would like to hear your views on them.

Hello Ram, Thanks. We will keep your suggestion in mind. Meanwhile, if you wish to know specifically about the FT fund you mentioned, you may check its features in an article I wrote when I was with the Hindu Business Line. While the portfolio would have changed, the basic characteristics of the fund remains the same. Here’s the link, if you wish to check out: http://www.thehindubusinessline.com/features/investment-world/mutual-funds/article3483249.ece Tks Vidya

Thanks for the link. Thats a nice write-up and similar lines to what I thought. I was dabbling with investing in it for my Vacation goals which will be realized every 3-4 years since it gives nice balance given the medium term I am looking at, your analysis seems to add positive points to it. Hope you will review FOFs in FI 🙂

Hi vidya, I liked your article on Pinebridge short term. So you say its a good fund to take exposure. But would you recommend FMPs in the current scenarios–say the short term one of 3m to 1 year FMPs?

Hi Uma, at this time of the year, FMPs that are little over a year will be more attractive as they will enjoy double indexation benefit (for long-term capital gain). A 3-month to 1 year FMP’s returns may not be too high at a time when interest rates are beginning to fall. As FMPs simply lock your investment and give you the accrual income (interest income from debt instruments), they will not be actively managed.This coupled with the short-term capital gain (your tax bracket of 10%, 20% or 30%) do not make short-term FMPs attractive right now. Tks, Vidya

Hey Vidya,

thanks for that quick response. I am a moderately aggresive investor….so from the looks of it, can i safely conclude that a short term fund would be better to invest in rather than am FMP( 3m to 1yr)?

Hi Uma, Yes, as an investment option, I would say the short-term fund scores right now. But Pl. go through the time frame mentioned by us in the article for this short-term fund. Hope you are willing to hold it for at least a year. While there is no exit load, it is safer to hold a fund nearer to its average portfolio maturity to avoid volatility. Tks Vidya

Hi vidya, looking at the budget and the emphasis given to infrastructure, am sure infrastrucutre fudns will surely be the flavor in the coming months. I as an investor have alwasy beleived in the infrastrucutre theme and optimistic that they will perfrom from a 3-5 yr time horizon. I have inveastment in ICICI Infra fund. also a DSP TIGER fund. Are they good funds or should i be looking at any other fund?

Hi Uma, we do not hold an opinion on theme funds barring banking funds as they are a more secular theme. The emphasis given to infrastructure in this budget is no different from earlier budgets. But implementation has been a challenge. Environmental clearance, land acquisition, funding etc are problems that have not been solved thus far despite creation of debt infrastructure funding. If these road blocks are cleared then the sector can really turn around. Hence, I would not rely on the budget alone for delivering.

That said, good blue chip companies like L&T or BHEL (power equipment) are available at good valuations. Hence there is select opportunity in the space. Right now, ICICI Pru Infra and Canara Robeco Infra have thrived the tough times quite well. The call on theme funds, though, will be entirely yours. Given a five-year under-performance track record by these funds, it will not be easy for me to defend this sector at a time when central elections are due in about a year’s time. Tks, Vidya

Shoudl we invest lumpsum in this fund or like SIP.

A lump sum is good for this fund at this point, if you can spare. Otherwise go for shorter term SIP as this is essentially a 1-1.5 year fund. Tks Vidya

Hi

Can I go for this PineBridge India Short Term for a value 5L for period of 2-3 year, & planing for a STP for a MIDCAP / Oppurtunities for a same period from this, any suggestion on this.

Hello sir, If you will stay in the short-term fund for 1-1.5 years and then make your STP, you may do so. If you wish to start your STP right away, you will be better off with liquid funds to avoid the hassle of short-term capital gains. Tks, Vidya

Hi Vidya,

Do you think its a good time to park a lumpsum of 1 lakh in it with a horizon of 1.5 to 2 yrs?

Hello Ram, If you are talking about the fund in this article, yes it is. Given the rate puase, short-term liquidity requirements is likely to increase thus improving prospects of short-term funds. tks, Vidya

Thanks for the link. Thats a nice write-up and similar lines to what I thought. I was dabbling with investing in it for my Vacation goals which will be realized every 3-4 years since it gives nice balance given the medium term I am looking at, your analysis seems to add positive points to it. Hope you will review FOFs in FI 🙂

Shoudl we invest lumpsum in this fund or like SIP.

A lump sum is good for this fund at this point, if you can spare. Otherwise go for shorter term SIP as this is essentially a 1-1.5 year fund. Tks Vidya

Hi vidya, I liked your article on Pinebridge short term. So you say its a good fund to take exposure. But would you recommend FMPs in the current scenarios–say the short term one of 3m to 1 year FMPs?

Hi Uma, at this time of the year, FMPs that are little over a year will be more attractive as they will enjoy double indexation benefit (for long-term capital gain). A 3-month to 1 year FMP’s returns may not be too high at a time when interest rates are beginning to fall. As FMPs simply lock your investment and give you the accrual income (interest income from debt instruments), they will not be actively managed.This coupled with the short-term capital gain (your tax bracket of 10%, 20% or 30%) do not make short-term FMPs attractive right now. Tks, Vidya

Hey Vidya,

thanks for that quick response. I am a moderately aggresive investor….so from the looks of it, can i safely conclude that a short term fund would be better to invest in rather than am FMP( 3m to 1yr)?

Hi Uma, Yes, as an investment option, I would say the short-term fund scores right now. But Pl. go through the time frame mentioned by us in the article for this short-term fund. Hope you are willing to hold it for at least a year. While there is no exit load, it is safer to hold a fund nearer to its average portfolio maturity to avoid volatility. Tks Vidya

Hi vidya, looking at the budget and the emphasis given to infrastructure, am sure infrastrucutre fudns will surely be the flavor in the coming months. I as an investor have alwasy beleived in the infrastrucutre theme and optimistic that they will perfrom from a 3-5 yr time horizon. I have inveastment in ICICI Infra fund. also a DSP TIGER fund. Are they good funds or should i be looking at any other fund?

Hi Uma, we do not hold an opinion on theme funds barring banking funds as they are a more secular theme. The emphasis given to infrastructure in this budget is no different from earlier budgets. But implementation has been a challenge. Environmental clearance, land acquisition, funding etc are problems that have not been solved thus far despite creation of debt infrastructure funding. If these road blocks are cleared then the sector can really turn around. Hence, I would not rely on the budget alone for delivering.

That said, good blue chip companies like L&T or BHEL (power equipment) are available at good valuations. Hence there is select opportunity in the space. Right now, ICICI Pru Infra and Canara Robeco Infra have thrived the tough times quite well. The call on theme funds, though, will be entirely yours. Given a five-year under-performance track record by these funds, it will not be easy for me to defend this sector at a time when central elections are due in about a year’s time. Tks, Vidya

Hi

Can I go for this PineBridge India Short Term for a value 5L for period of 2-3 year, & planing for a STP for a MIDCAP / Oppurtunities for a same period from this, any suggestion on this.

Hello sir, If you will stay in the short-term fund for 1-1.5 years and then make your STP, you may do so. If you wish to start your STP right away, you will be better off with liquid funds to avoid the hassle of short-term capital gains. Tks, Vidya

Hi Vidya,

Can you tell me the difference between primebridge india short term fund and IDFC super saver income fund. One is in short term category and other is an income fund, but for both the funds the benchmark is CRISIL short term bond. Then why the difference in classification. I think IDFC SSI fund is also having a duartion of <2.

Thanks,

karthik

Hello Karthik, IDFC SSI has two categories – IDFC SSI Short Term Plan and IDFC SSI Medium Term Plan. We are not sure which one you meant. IDFC SSI Short Term, has a less than 2-year portfolio maturity. However, it has higher exposure to bonds/debentures and does not also have a very inspiring track record.

IDFC Medium Term Plan is a more flexi-income fund (we gave a recommendation on this fund a while ago) . It can go for short-term maturities or go long based on debt market conditions. This fund too has Crisil Short Term Bond index. Because it is a flexi fund, its choice of index cannot be very accurate. In equity funds for example, a diversified fund will have Nifty as its index but it will very much invest in mid-cap stocks as well. The index choice in debt is also something similar. IDFC SSI Medium Term currently has a portfolio maturity of 3.27 years.

PineBridge India Short Term on the other hand does not have too much flexibility to go long. Hence it is essentially a short-term income fund. Its portfolio has more CDs than the other 2 and has a maturity of about 1.6 years. Hope this helps. – Tks Vidya

Thanks for the clarification.

I was refering to IDFC SSI Medium Term fund. In Continuum to the discussion we are having, what is your view on flexi debt funds. I remember reading a report in moneylife stating that flexi debt/income funds are not out of line except for expense ratio. Can you express your opinion/ views

Thanks,

Karthik

Hello Karthik, go-anywhere debt funds or dynamic or income funds are basically the counterparts of diversified equity fund in equity category. But as you stated earlier, these funds will have a key strategy, it could be playing the credit risk or interest rate risk or a combination of both or simply an accrual strategy or sometimes making capital gains from gilts. As they are more dynamically managed, their expense ratio will be slightly higher than say plain vanilla liquid funds or ultra-short-term funds. But much lower than equity funds. I am not sure what you meant by ‘out of line’ but certainly, these funds require a longer time frame and some appetite for risk by an investor when compared with short-term or liquid funds. If you take pure gilt funds, they are credit=safe but have high interest rate risk. But income funds would have a bit of both the risks but not too much. So they are indeed different in the debt category. tks, Vidya

Interesting suggestion Vidhya, but a logical one. As always its very informative and refreshing to read your recommendations than the run of the mill recommendations in other sites. Have a small request, can you review any of the FOFs in the market. For example, FT Life Stage FoF 40s. I see a mixed reaction about these and would like to hear your views on them.

Hello Ram, Thanks. We will keep your suggestion in mind. Meanwhile, if you wish to know specifically about the FT fund you mentioned, you may check its features in an article I wrote when I was with the Hindu Business Line. While the portfolio would have changed, the basic characteristics of the fund remains the same. Here’s the link, if you wish to check out: http://www.thehindubusinessline.com/features/investment-world/mutual-funds/article3483249.ece Tks Vidya

Hi Vidya,

Do you think its a good time to park a lumpsum of 1 lakh in it with a horizon of 1.5 to 2 yrs?

Hello Ram, If you are talking about the fund in this article, yes it is. Given the rate puase, short-term liquidity requirements is likely to increase thus improving prospects of short-term funds. tks, Vidya