Build a foundation with blue chips

If you wish to start building an equity portfolio with mutual funds, then ICICI Pru Focused Bluechip Equity (ICICI Pru Bluechip) can be a good fund to start your core portfolio. A basket made up of the top large-cap companies in the listed universe, active fund management that throws in a few mid-cap stocks for returns and a bit of derivatives to hedge the portfolio from market volatility have all worked in favour of this fund since its launch in May 2008.

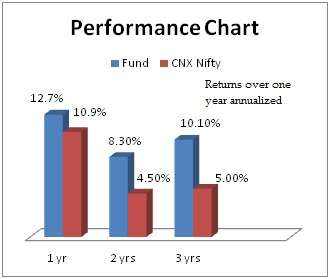

Had you invested in the fund since its inception using the SIP mode, it would have delivered 15.7%, higher than the 9.5% return of its benchmark CNX Nifty.

But a point-to-point return would suggest that the fund lagged its benchmark by less than a percentage point. This is simply because the Nifty had fallen quite a bit by mid-2008, while the fund, just launched and starting off with cash, did not have such a low base to contend with.

Suitability

As stated earlier, the fund is suitable for those who wish to start an equity portfolio. But be prepared for a fall in your portfolio in a bear market as holding blue chips does not entirely insulate your portfolio from market fall. It may, at best, reduce the impact and possibly bounce back faster on a revival.

If you are a very conservative investor and want a tryst with equities without getting hurt, then balanced equity-oriented funds will be a better route.

Opt for the growth strategy and have a time frame of at least 3-5 years. Consider an SIP of not less than 3 years to average costs well. If you are building a long-term portfolio then have longer SIPs. If you become familiar with markets, buy this fund with a small lump sum (besides the regular running SIPs), in market corrections of 5-10%.

Performance

ICICI Pru Bluechip has an exemplary record of beating its benchmark 98% of the times on a rolling one-year return basis since its inception. But it is to be noted that the few instances of underperformances, occurred in 2012. As the quantum of under performance was less than a percentage point in all these instances, it does not cause any undue concern.

It is also worth noting that the sudden rally in the later half of 2012 may have caught the fund unaware, especially given that it uses a bit of derivatives. While the fund management did change hands in 2012 (from Prashant Kothari to Manish Gunwani), we do not see any fundamental change in the strategy or performance of the fund that warrants concern.

ICICI Pru Bluechip has a risk-adjusted return superior to older large-cap funds such as Franklin India Bluechip and HDFC Top 200 in the last three years.

That said, it has limited room to maneuver outside of the large-cap stocks. Hence, HDFC Top 200 may overtake the fund in rallies that are not very large-cap focused.

But to its credit, its returns do not deviate much from its mean and it also contains declines better than most other large-cap peers, thanks to its occasional use of derivatives, sometimes using the index futures and at other times more stock-specific futures for hedging purposes.

Portfolio

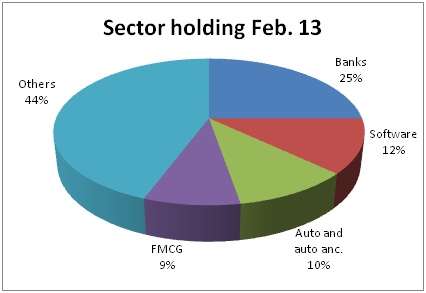

As is the case with most large-cap funds, the fund is heavy on banks. ICICI Pru Bluechip, in fact, increased its exposure to this sector over the last one year.

The usual large-cap performers, HDFC Bank, ICICI Bank and SBI, besides Kotak Mahindra Bank together accounted for a fifth of the portfolio.

While IT sector was the second largest holding, FMCG stocks interestingly saw an increase in exposure in the space of a year, with United Spirits and Nestle coming in, even as Marico exited the portfolio, in the later part of 2012. Auto and auto ancillaries too were in the top 5 sector exposures.

Energy stocks such as Petronet LNG, Cairn India and PGCIL offer some balance in terms of ‘value’ exposure, against the otherwise ‘growth-heavy’ portfolio.

Hi Vidya,

I have a good surplus in my hand right now. Is it a good idea to invest the entire amount in ICICI pru liquid fund and initiate a weekly/daily STP to ICICI Pru Foc Bluchip Equity for say 3 months?

Note: I also have a regular monthly SIP on Bluchip fund.

Hi Karthik, systematic investments work well over longer time frames – typically three years or more. Averaging for 3 months may seldom make a huge difference, unless you are lucky to have a down market in those 3 months (where you will have opportunity to buy the fund at lower NAVs). Hence, while there is no harm in doing such an STP, you can also consider setting triggers for investing in to the fund on market dips of say 5% or NAV dip or 10% or more. Of course, this strategy works if you have followed the markets and can fix your own level to invest or book profits. Tks, Vidya

Hi Vidya,

Thanks for the response. I have a monthly SIP on the said fund and I believe I will continue it for atleast 3 years.

The doubt I have is regarding the surplus cash I recently accumulated.I just came across some comments in some other website that STP from liquid to equity is a better way to invest surplus cash than buying the equity fund units entirely in one shot. Correct me if I am wrong.

Hi Karthik, It is true that it is not a great idea to invest in equities in lump sum. If you get your timing bad (say at the peak), then your investments can take a hit. But whether you use an SIP or STP, what you try to do is average out your investments in a phased manner. Such averaging does not work over short frames, it works over long time frames. Hence, unless the quantum of money is large enough to support an STP for say 2-3 years, there may not be great advantage in doing so. This is what I meant by saying that averaging over say 3 months may not be very effective. hence, if you wish to do an STP do so, but once the STP is done with (that too in 3 months), initiate an SIP in the equity fund and do not stop with the few months of STPs. Tks, Vidya

Hi Vidya,

I have a good surplus in my hand right now. Is it a good idea to invest the entire amount in ICICI pru liquid fund and initiate a weekly/daily STP to ICICI Pru Foc Bluchip Equity for say 3 months?

Note: I also have a regular monthly SIP on Bluchip fund.

Hi Karthik, systematic investments work well over longer time frames – typically three years or more. Averaging for 3 months may seldom make a huge difference, unless you are lucky to have a down market in those 3 months (where you will have opportunity to buy the fund at lower NAVs). Hence, while there is no harm in doing such an STP, you can also consider setting triggers for investing in to the fund on market dips of say 5% or NAV dip or 10% or more. Of course, this strategy works if you have followed the markets and can fix your own level to invest or book profits. Tks, Vidya

Hi Vidya,

Thanks for the response. I have a monthly SIP on the said fund and I believe I will continue it for atleast 3 years.

The doubt I have is regarding the surplus cash I recently accumulated.I just came across some comments in some other website that STP from liquid to equity is a better way to invest surplus cash than buying the equity fund units entirely in one shot. Correct me if I am wrong.

Hi Karthik, It is true that it is not a great idea to invest in equities in lump sum. If you get your timing bad (say at the peak), then your investments can take a hit. But whether you use an SIP or STP, what you try to do is average out your investments in a phased manner. Such averaging does not work over short frames, it works over long time frames. Hence, unless the quantum of money is large enough to support an STP for say 2-3 years, there may not be great advantage in doing so. This is what I meant by saying that averaging over say 3 months may not be very effective. hence, if you wish to do an STP do so, but once the STP is done with (that too in 3 months), initiate an SIP in the equity fund and do not stop with the few months of STPs. Tks, Vidya

Hi Vidhya,

I am new to mutual funds interested in Investing through SIP.My age is 23 and monthly i like to invest around 2000. Suggest me good funds

Hi Satheesh, we would typically advice new investors to use our ‘Ask Advisor’ feature (available in their fundsindia account on completing opening formalities) to provide fund suggestions. This is because we would need details of your time frame, goal if any and also risk appetite to know whether you can invest in equity or debt. Alternatively, you can use the SIP designer tool in your fundsIndia account; that will help you assess your risk and suggest funds accordingly.

But to broadly answer your question: if your time frame is not less than 3 yrs and you are a first time investor, then balanced (equity-oriented) funds can be a good choice. You can check for those in: http://www.fundsindia.com/select-funds

Pl. look under hybrid funds- moderate risk

tks

Vidya

Hi Vidhya,

I am new to mutual funds interested in Investing through SIP.My age is 23 and monthly i like to invest around 2000. Suggest me good funds

Hi Satheesh, we would typically advice new investors to use our ‘Ask Advisor’ feature (available in their fundsindia account on completing opening formalities) to provide fund suggestions. This is because we would need details of your time frame, goal if any and also risk appetite to know whether you can invest in equity or debt. Alternatively, you can use the SIP designer tool in your fundsIndia account; that will help you assess your risk and suggest funds accordingly.

But to broadly answer your question: if your time frame is not less than 3 yrs and you are a first time investor, then balanced (equity-oriented) funds can be a good choice. You can check for those in: http://www.fundsindia.com/select-funds

Pl. look under hybrid funds- moderate risk

tks

Vidya

Hi Vidhya,

Thanks for your answer. Let me elebrote my goals to invest in SIP 2000 rs per month for 3 years for my marriage . To get around 5lakhs in which mutual funds i should invest . What is risk profile i should follow.

Hi Vidhya

Thanks for your Reply. TO be specific I need 5lakhs in 3 years SIP in 2000 Rs per month. Please suggest me the risk profile and which funds i should invest

Hello Satheesh, Thank you for writing in. As mentioned earlier, you may choose balanced funds (hybrid moderate risk) from our select funds list or seek our free portfolio advisory service as a customer. Currently, I am constrained from giving individual portfolio advice in a common forum as it is a value add we do for our investors. Once you complete your one-time documentation, you can fully make use of this service. Many tks, Vidya

Dear Vidya,

I calculated the difference of investing through a broker like Funds India and through direct plan option.

For 1 lakh investment for a period of 20years,there is a difference of 18% in the final fund considering a 1% difference in charges.

Though I understand that Funds India is here for doing business,Why don’t you promote ethics by voluntarily advocating this and promote investing through the direct route and not through brokers like funds India. Let people be richer!

Not sure if you would publish this comment 🙂

Hi Prem,

We do not hold back comments just because you have a different view 🙂

First, on the calculations. The diff between direct and regular plan expense ratio can go up to 0.75% (min abt 0.25%) and for Rs 1 lakh for 20 years with a pre-expense return of 15% the post-expense returns is 12.1% annually with a regular plan and 12.9% annually with a direct plan. The absolute differential is 16%.

Now to answer your suggestion:

1. There is no ethical issue involved in this. Distributors are not allowed to sell direct plans. So the question of FundsIndia suggesting it does not even arise.

2. the differential in returns will be more than compensated by timely and right advice received on funds and on asset allocation. Just take a fund/portfolio that delivered 12% annual returns and another with 15% annual returns. Rs 10,000 would have grown to Rs 9.64 lakh at 12% annually and to Rs 16.4 lakh at 15% annually. In absolute return terms the 15% annual delivering portfolio/funds would have delivered 69% higher! You may view this against the 16% (or 18% as you took) differential for the entire period. As you will be aware, the difference in annual returns can be as high as 10 percentage points over a 20-year period between a well-performing fund and a mediocre one. Investors need to be confident of being able to weed out laggards on a regular basis and choose performing ones, besides optimally rebalancing their portfolio, if they think the direct plan differential matters.

3.Within the universe of funds, we have stayed clear of any biased view and have purely suggested funds on grounds of merit alone, not allowing other factors to influence us. Again, on this account, you can stay assured that ethical questions do not arise.

4. We are confident that the convenience of transacting and viewing in a single platform like FundsIndia, getting highly flexible online transacting tools not available elsewhere, unbiased advisory service and automated advisory services like Smart Solutions will more than make up for the differential when it comes to building a long-term portfolio.

Thanks.

I want to invest 10000 rs per month in mutual fund for 2 years. My goal is to get around 3.5 lakhs. Plz suggest funds.

Hi Jitendra,

Individual fund recommendations/reviews are made by our advisory team through the ‘Ask Advisor’ feature available free of cost for all FundsIndia investors. Request you to activate your account if you have not, to enable us to help you with fund advisory and review. Thanks.

Hi,

I am 30 yr old unmarried govt. employee & i want to invest 1000 pm through two SIP (500*2) in bluchip and any other funds for next 5 years or more , please suggest me which fund will be better to invest.

Hello varun,

Sorry for the delayed response. For fund specific/portfolio queires, pl use your FundsIndia account, if youa re an account holder to raise the query using Advisor support (in help tab). This is a free service to all our investors. thanks, Vidya

Already investins rs 2500 each in hdfc top 200 , idfc premier equity , icici pru dynamic for 15 yrs term , which mf would make better addition to my portfolio _ICICI PRU FOCUSSED BLUECHIP or Franklin bluechip ?

Hello Kenny, It would depend on your risk appetite. Franklin India Bluechip would be steady but not top notch. Do ask our advisors to assess your requirement and help choose a fund – through the help mode in your FundsIndia account, if you have one. thanks, Vidya

Already investins rs 2500 each in hdfc top 200 , idfc premier equity , icici pru dynamic for 15 yrs term , which mf would make better addition to my portfolio _ICICI PRU FOCUSSED BLUECHIP or Franklin bluechip ?

Hello Kenny, It would depend on your risk appetite. Franklin India Bluechip would be steady but not top notch. Do ask our advisors to assess your requirement and help choose a fund – through the help mode in your FundsIndia account, if you have one. thanks, Vidya

Dear Vidya,

I calculated the difference of investing through a broker like Funds India and through direct plan option.

For 1 lakh investment for a period of 20years,there is a difference of 18% in the final fund considering a 1% difference in charges.

Though I understand that Funds India is here for doing business,Why don’t you promote ethics by voluntarily advocating this and promote investing through the direct route and not through brokers like funds India. Let people be richer!

Not sure if you would publish this comment 🙂

Hi Prem,

We do not hold back comments just because you have a different view 🙂

First, on the calculations. The diff between direct and regular plan expense ratio can go up to 0.75% (min abt 0.25%) and for Rs 1 lakh for 20 years with a pre-expense return of 15% the post-expense returns is 12.1% annually with a regular plan and 12.9% annually with a direct plan. The absolute differential is 16%.

Now to answer your suggestion:

1. There is no ethical issue involved in this. Distributors are not allowed to sell direct plans. So the question of FundsIndia suggesting it does not even arise.

2. the differential in returns will be more than compensated by timely and right advice received on funds and on asset allocation. Just take a fund/portfolio that delivered 12% annual returns and another with 15% annual returns. Rs 10,000 would have grown to Rs 9.64 lakh at 12% annually and to Rs 16.4 lakh at 15% annually. In absolute return terms the 15% annual delivering portfolio/funds would have delivered 69% higher! You may view this against the 16% (or 18% as you took) differential for the entire period. As you will be aware, the difference in annual returns can be as high as 10 percentage points over a 20-year period between a well-performing fund and a mediocre one. Investors need to be confident of being able to weed out laggards on a regular basis and choose performing ones, besides optimally rebalancing their portfolio, if they think the direct plan differential matters.

3.Within the universe of funds, we have stayed clear of any biased view and have purely suggested funds on grounds of merit alone, not allowing other factors to influence us. Again, on this account, you can stay assured that ethical questions do not arise.

4. We are confident that the convenience of transacting and viewing in a single platform like FundsIndia, getting highly flexible online transacting tools not available elsewhere, unbiased advisory service and automated advisory services like Smart Solutions will more than make up for the differential when it comes to building a long-term portfolio.

Thanks.

Hi Vidhya,

Thanks for your answer. Let me elebrote my goals to invest in SIP 2000 rs per month for 3 years for my marriage . To get around 5lakhs in which mutual funds i should invest . What is risk profile i should follow.

Hi Vidhya

Thanks for your Reply. TO be specific I need 5lakhs in 3 years SIP in 2000 Rs per month. Please suggest me the risk profile and which funds i should invest

Hello Satheesh, Thank you for writing in. As mentioned earlier, you may choose balanced funds (hybrid moderate risk) from our select funds list or seek our free portfolio advisory service as a customer. Currently, I am constrained from giving individual portfolio advice in a common forum as it is a value add we do for our investors. Once you complete your one-time documentation, you can fully make use of this service. Many tks, Vidya

Hi,

I am 30 yr old unmarried govt. employee & i want to invest 1000 pm through two SIP (500*2) in bluchip and any other funds for next 5 years or more , please suggest me which fund will be better to invest.

Hello varun,

Sorry for the delayed response. For fund specific/portfolio queires, pl use your FundsIndia account, if youa re an account holder to raise the query using Advisor support (in help tab). This is a free service to all our investors. thanks, Vidya

I want to invest 10000 rs per month in mutual fund for 2 years. My goal is to get around 3.5 lakhs. Plz suggest funds.

Hi Jitendra,

Individual fund recommendations/reviews are made by our advisory team through the ‘Ask Advisor’ feature available free of cost for all FundsIndia investors. Request you to activate your account if you have not, to enable us to help you with fund advisory and review. Thanks.