Admit it; had you been looking at the five-year point-to-point returns of equity funds in the last few months, you would have been tempted to simply stash your money in FDs. I am not blaming. I mean, a 4.5 per cent category-average 5-year return of equity funds would take you nowhere! And inflation rose at 7.6 per cent annually over the same period.

Does this shock you? It should, because there is no better example than this period to showcase to you the perils of lump sum investing in equity markets. On the flip side, there is no better example than this to tell why you should not be looking at point-to-point fund returns alone to arrive at your fund buy-sell decision.

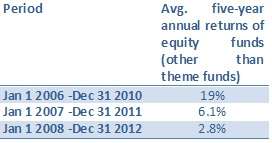

The five-year misery

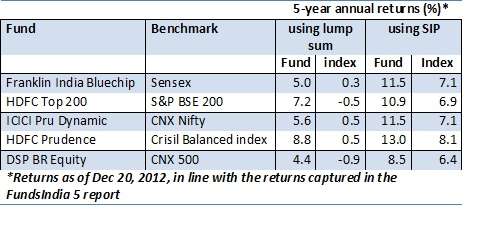

Let us take the example of our recent report ‘ The FundsIndia 5’ (if you haven’t had a chance to read this, login to your FundsIndia account and click the link on the top right) ; five funds that stood the test of time for over a decade.

We had the five and ten-year point-to-point returns of these funds mentioned in the report and what a contrast they were. The ten-year returns were in high double digits while the five-year returns were in the range of 4-8 per cent. Now, that set quite a few of you wondering how these funds were investment worthy in the first place. Others felt, funds simply reflect markets. If the markets were at a peak in 2007 (our five-year period was Dec 2007-12), then funds can’t be any better.

The number game

Yes, some of you were right that funds cannot perform too differently from the markets. After all, that is where they invest. And that is the reason why when markets move, fund performance can change drastically.

See the table given alongside. Returns from peak markets of 2007 and early 2008 clearly delivered poor returns because both the market and your funds would have been at a high then. But 2006 was different as the market was just entering a bull phase.

Simply put, the base matters when it comes to returns; or in other words, when you invested matters (if you invest through lump sum). Calculate from a peak and your returns are low. Calculate from a low and the scene changes drastically. The former is what we have been seeing in recent months.

Now coming back to FundsIndia 5, see table below. Compare the SIP returns over the same period compared with the 5-year point-to-point returns. The former is superior and does not alarm you.

Agreed, that it was a tough period overall and superior return was hard to come by (pl. note that some funds managed better returns than this but for illustrative purposes we chose FundsIndia 5).

Now if you are a regular, systematic investor, this is what you should be looking at, in your portfolio, not just the flash in the pan point-to-point returns. (please note that your portfolio at FundsIndia provides you the IRR of your SIPs of over one year and also that of the whole portfolio) Otherwise, there is a risk of your making a sell decision (or sometimes a buy decision) based on the point-to-point returns.

Does it mean that you should never go for lump sum? You can, if you have a very long-term goal of say 8-10 years or more. In such as case, even if you time your entry poorly, chances are that markets go through multi-cycles in those 10 years or more to deliver decent returns.

If you have a medium-term goal of five years are so, SIPs can be a less risky bet. At best, you may supplement it with lump sums when you see a market correction of say 5 per cent or more if you wish to prop up your portfolio returns.

Hi Vidya Madam,

I liked the article. But why we Indians are so obsessed with returns? Why can’t we ask questions like, “How many analysts team up with fund manager?” “How many times in the last 5 yeas scheme ABC was in the top decile or quartile?” “What processes you follow in AMC? “Do you have a separate team for risk management or mitigation?” “What instant alerts can u send when u come across cases like Satyam in 2009 and bribery case in LIC Housing Finance?” “Do your analyst meet company top management and ask hard questions at AGMs???

Regards,

Aditya

Hello sir,

Very good questions. But these are something only followers of market or well-informed investors can ask. Often times, mutual funds serve as a vehicle to get decent returns for investors who do not have the time or wherewithal to know how funds are run. Hence, while I totally agree that investors need to spend time or doing their groundwork on this, and understanding he importance of the facctors you mentioned, it may not be easy for them to do so. At the same time, we do have to gradually get out of this mode of ‘chasing returns’. It is not only dangerous (wrong decisions can be made) but can also lead to disappointment, often pushing investors out of the equity markets and back to unorganised forms of investments. At FundsIndia we do our research taking in to account these factors. But not of these amy mentioned in the article you get. Tks Vidya

Thanks for the reply mam. I follow you since your innings with Business Line. Really appreciate your writing and knowledge on the subject.

Rgds,

Aditya

Thanks Aditya.

Dear Fundsindia Team,

I want to invest in Gold ETF. Call me at 9885555008

Hi,

I like the idea of investing in debt and tranfer IT to equity fund. Could You please guide me how to go for it and the best funds for IT.

Hi Saji, the funds you choose for a STP from liquid to equity should be in the same AMC to effect such transactions. For building a portfolio with SIP, request you to send your detailed query, with amount, risk appetite and time frame for equity funds through our Ask Advisor feature (see the following space in your FundsIndia account: http://content.fundsindia.com/images/GettingAdvice.png ). You can either choose the email option or schedule a call, wherein our advisors will call you back. Tks Vidya

HI Vidya,

During the change over from a mutual fund to another ,Is it advisable to Put lumpsum or the same through SIP ?My idea is that park the redeemed fund in a Liquid plan and invest by SWP.

But by the new Tax laws the Liquid fund has become less attractive due to the dividend distribution hike by 50 %. Can you comment on this ?

Hello Jinny,

It is better to invest in a phased manner when you are investing in equity/gold/long-term debt. Investing a lumpsum in a liquid fund and then investing using STP to other equity/debt funds is a good option. Liquid funds do not fluctuate like equities. Hence, there is no harm in investing in lumpsums in them. Infact they are best suited for short-term lump sums. Our article discusses only on the perils of investing in equities in lump sum.

Liquid funds have not become less attractive as they had DDT of 25% even earlier and continue to have the same. Only ultra short-term and other debt funds have been proposed a hike in DDT in the recent budget. Tks Vidya

Hi,

I like the idea of investing in debt and tranfer IT to equity fund. Could You please guide me how to go for it and the best funds for IT.

Hi Saji, the funds you choose for a STP from liquid to equity should be in the same AMC to effect such transactions. For building a portfolio with SIP, request you to send your detailed query, with amount, risk appetite and time frame for equity funds through our Ask Advisor feature (see the following space in your FundsIndia account: http://content.fundsindia.com/images/GettingAdvice.png ). You can either choose the email option or schedule a call, wherein our advisors will call you back. Tks Vidya

Hi Vidya,

Very appropriate article. I had also invested in the highs and the CAGR over 5 years is only 4 to 5%. Will it make sense for me to liquidate the investment and re-invest the amounts in a source liquid fund and through that into an equity fund on a SIP basis.. This is just to rejig and capture the volatility in the market and enhance the performance of the investment.

Hello sir,

We cannot comment on liquidation without knowing the funds. But if you have stayed that long and earned 4-5% it is likely that they are infrastructure or related funds. While this has been one under performer that has chances of revival in a growth market, no one can guess how long that will take. Hence, it does make sense to take the opportunity in the current market and move to better funds. if the amount is not huge, you need not even use liquid funds. do a simple SIP. If the amount is large, then use a liquid fund to transfer. Tks, Vidya

Hi Vidya,

Thanks for your quick response. The funds in question are HDFC Top 200, HDFC Prudence and DSPBR Equity. I had made lump sum investments in these funds in January 2008 and then again in December 2010 and the amounts are large. Appreciate your views. Thanks.

Hi Vidya,

Thanks for your quick response. The funds that I invested in are HDFC Top 200, HDFC Prudence and DRSPBR Equity. I made a lump sum investment in these funds in January 2008 and then thru a six month SIP between May and December 2010. The returns have been dismal. YThe funds are large. Appreciate your views on whether liquidation and then reinvesting the proceeds thru a liquid fund into a robust equity fund by SIP would be advisable. Thanks again.

Also , I must say your articles and responses are well written, lucid, simple and very appropriate.

Hello sir,

You have invested in some good funds but you have been unfortunate twice: once, when investing as lump sum in market peak and two, investing through a very short SIP tenure between May and Dec 2010, again an upmarket. Had this SIP been extended to whole of 2011, you would have averaged well at lower costs and 2012 would have been a better year for you. In general, if you go for SIPs, you would require at least a 3-year time frame simply to average. That is the typical time taken by the market to see an up cycle and down cycle thus helping you average.

Moving to your funds, you will have to exit only if you need the money now. Otherwise, it is best that you hold it. It is normally not a very prudent idea to remove the money and re-enter just because the market levels are lower. This would make sense if the funds you are holding are not good and need to be sold. Otherwise, you would lose the full benefit of compounding, if you are going to take the money out and do an SIP from the start.

Hence my suggestion is that if you have at least a 5-year time frame then you should stay put. If you are working towards a goal and need to save more, then this is a good time to start an SIP, esp, in a balanced fund (some debt returns will also come by now). But pl. ensure that your SIP is at least 3 years.

If you need this money in 2-3 years, then it is best that you move gradually to debt funds or other safer debt avenues.

Tks,

Vidya

Thanks Vidya, got it.

HI Vidya,

During the change over from a mutual fund to another ,Is it advisable to Put lumpsum or the same through SIP ?My idea is that park the redeemed fund in a Liquid plan and invest by SWP.

But by the new Tax laws the Liquid fund has become less attractive due to the dividend distribution hike by 50 %. Can you comment on this ?

Hello Jinny,

It is better to invest in a phased manner when you are investing in equity/gold/long-term debt. Investing a lumpsum in a liquid fund and then investing using STP to other equity/debt funds is a good option. Liquid funds do not fluctuate like equities. Hence, there is no harm in investing in lumpsums in them. Infact they are best suited for short-term lump sums. Our article discusses only on the perils of investing in equities in lump sum.

Liquid funds have not become less attractive as they had DDT of 25% even earlier and continue to have the same. Only ultra short-term and other debt funds have been proposed a hike in DDT in the recent budget. Tks Vidya

Dear Fundsindia Team,

I want to invest in Gold ETF. Call me at 9885555008

Hi Vidya Madam,

I liked the article. But why we Indians are so obsessed with returns? Why can’t we ask questions like, “How many analysts team up with fund manager?” “How many times in the last 5 yeas scheme ABC was in the top decile or quartile?” “What processes you follow in AMC? “Do you have a separate team for risk management or mitigation?” “What instant alerts can u send when u come across cases like Satyam in 2009 and bribery case in LIC Housing Finance?” “Do your analyst meet company top management and ask hard questions at AGMs???

Regards,

Aditya

Hello sir,

Very good questions. But these are something only followers of market or well-informed investors can ask. Often times, mutual funds serve as a vehicle to get decent returns for investors who do not have the time or wherewithal to know how funds are run. Hence, while I totally agree that investors need to spend time or doing their groundwork on this, and understanding he importance of the facctors you mentioned, it may not be easy for them to do so. At the same time, we do have to gradually get out of this mode of ‘chasing returns’. It is not only dangerous (wrong decisions can be made) but can also lead to disappointment, often pushing investors out of the equity markets and back to unorganised forms of investments. At FundsIndia we do our research taking in to account these factors. But not of these amy mentioned in the article you get. Tks Vidya

Thanks for the reply mam. I follow you since your innings with Business Line. Really appreciate your writing and knowledge on the subject.

Rgds,

Aditya

Thanks Aditya.

Hi Vidya,

Very appropriate article. I had also invested in the highs and the CAGR over 5 years is only 4 to 5%. Will it make sense for me to liquidate the investment and re-invest the amounts in a source liquid fund and through that into an equity fund on a SIP basis.. This is just to rejig and capture the volatility in the market and enhance the performance of the investment.

Hello sir,

We cannot comment on liquidation without knowing the funds. But if you have stayed that long and earned 4-5% it is likely that they are infrastructure or related funds. While this has been one under performer that has chances of revival in a growth market, no one can guess how long that will take. Hence, it does make sense to take the opportunity in the current market and move to better funds. if the amount is not huge, you need not even use liquid funds. do a simple SIP. If the amount is large, then use a liquid fund to transfer. Tks, Vidya

Hi Vidya,

Thanks for your quick response. The funds in question are HDFC Top 200, HDFC Prudence and DSPBR Equity. I had made lump sum investments in these funds in January 2008 and then again in December 2010 and the amounts are large. Appreciate your views. Thanks.

Hi Vidya,

Thanks for your quick response. The funds that I invested in are HDFC Top 200, HDFC Prudence and DRSPBR Equity. I made a lump sum investment in these funds in January 2008 and then thru a six month SIP between May and December 2010. The returns have been dismal. YThe funds are large. Appreciate your views on whether liquidation and then reinvesting the proceeds thru a liquid fund into a robust equity fund by SIP would be advisable. Thanks again.

Also , I must say your articles and responses are well written, lucid, simple and very appropriate.

Hello sir,

You have invested in some good funds but you have been unfortunate twice: once, when investing as lump sum in market peak and two, investing through a very short SIP tenure between May and Dec 2010, again an upmarket. Had this SIP been extended to whole of 2011, you would have averaged well at lower costs and 2012 would have been a better year for you. In general, if you go for SIPs, you would require at least a 3-year time frame simply to average. That is the typical time taken by the market to see an up cycle and down cycle thus helping you average.

Moving to your funds, you will have to exit only if you need the money now. Otherwise, it is best that you hold it. It is normally not a very prudent idea to remove the money and re-enter just because the market levels are lower. This would make sense if the funds you are holding are not good and need to be sold. Otherwise, you would lose the full benefit of compounding, if you are going to take the money out and do an SIP from the start.

Hence my suggestion is that if you have at least a 5-year time frame then you should stay put. If you are working towards a goal and need to save more, then this is a good time to start an SIP, esp, in a balanced fund (some debt returns will also come by now). But pl. ensure that your SIP is at least 3 years.

If you need this money in 2-3 years, then it is best that you move gradually to debt funds or other safer debt avenues.

Tks,

Vidya

Thanks Vidya, got it.