- Short-term debt fund

- Invests in top-rated corporate bonds

Why

- Delivered FD-beating returns since inception in June 2010

- Seeks to reduce chances of negative returns

Who

- Investors with 2-year time frame looking for better-than FD returns

- Investors who cannot handle sharp fall in their funds

FD-beating returns, low chance of temporary negative returns and low risk of default in papers held – these summarise the key characteristics of HDFC Short Term Opportunities (HDFC ST Opportunities) fund. A month ago, we had covered Axis Banking & PSU Debt fund, another low-risk fund in the short-term debt category. HDFC ST Opportunities has a marginally higher risk profile (than the Axis fund) that helps generate slightly higher returns without posing any credit risk to investors. It also has a longer track record.

The fund & suitability

HDFC ST Opportunities is an open-ended short-term debt fund with an average portfolio maturity of little less than 2 years. In funds that predominantly earn returns from the interest income in the papers they hold, the fund’s average maturity (the maturity of the papers held) is an indication of how long you should hold the fund.

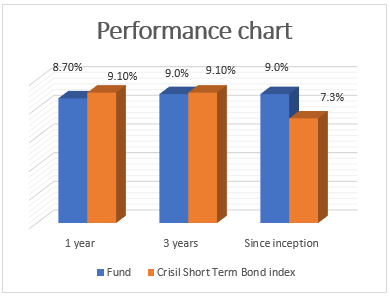

The fund has generated an annual return of 9 per cent (point-to-point) since its inception in June 2010. This is significantly higher than its benchmark (Crisil Short Term Bond index) return of 7.3 per cent. This performance is also noteworthy as most debt funds find it difficult to beat their benchmarks as practical considerations of building a portfolio, facing redemptions (which tend to be higher in debt than in equity) and expenses prevent them from beating a theoretically built index.

HDFC ST Opportunities is suitable for investors with a minimum 2-year time frame and those who do not expect their fund to remain positive every single day of their holding. On the other hand, investors can take comfort that this is one of the least risk, less volatile funds in the entire category. If one is willing to stay invested for the minimum time frame, they can aspire to earn FD-beating returns; with the added advantage of indexation benefit if held for over 3 years.

Investments can be considered in lumpsums like a FD or SIPs if you do not have much surplus.

Performance

HDFC ST Opportunities’ average rolling 2-year returns, when rolled daily since its inception comes to an annualised 9.3 per cent. This return of course, comes on the back of a positive scenario for debt funds for a good part of the fund’s life, and may not be possible always. Nevertheless, the fund has shown low-volatility and consistent returns since its launch. For example, the worst 2-year returns it delivered was 8 per cent and this too came in one of the most difficult periods for mutual funds in 2013. As 2013 was a low point, the returns it delivered over the 2-year time frames from 2013 to 2015 hit double digits and was as high as 11 per cent at times. But then, those are extraordinary scenarios.

Suffice to know that the fund has, since its inception, comfortably beat the average FD return of 8.4 per cent (pre-tax) in the 1-3 year FD bucket.

Very importantly, the fund has a very strong track record when it comes to containing declines. When its returns were rolled every month since inception, it generated negative returns just 1.8 per cent of the times (benchmark fell 4.8 per cent of the times) and this occurred entirely during the months of July and August of 2013, an extremely turbulent period for debt market, when even liquid funds generated negative returns for a short while. The fund did not have any 1-year periods of negative returns.

Banking & PSU funds are the only ones in this category to boast of containing declines well but then most of them do not have a track record of facing difficult markets like 2013.

Portfolio

It may not be right to compare HDFC ST Opportunities with all the funds in the short-term category. This is because the credit profile and the average maturity profile of many schemes are very different. For example, there are funds that have over a third of their portfolio in papers with rating of AA or lower. That means higher returns, from higher risk. Then there are funds like HDFC ST Opportunities that have held less than 10 per cent (on an average) in AA-rated papers or below in the past 3 years and since inception. Higher credit risk enhances the interest (coupon rate) that the fund derives from the papers, thus delivering higher returns.

Funds like HDFC ST Opportunities try to make up for low credit risk (and low yields) by gaining from any capital appreciation opportunities in their traded AAA-rated papers. That is, they sell the papers at a profit when yields fall. That they do this is evident when we compare the yield to maturity (average residual interest rate of papers in the portfolio) to the actual returns of the fund. The yield to maturity was an average 7.7 per cent in 2016 but the fund has clearly been ticking better returns than that so far.

HDFC ST Opportunities also avoids volatility arising from interest rate movements by keeping its average maturity at less than 2 years. Lower duration of a paper means the volatility is limited when interest rates move up or down.

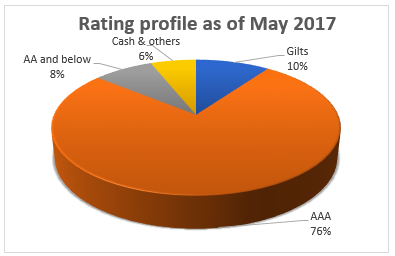

HDFC ST Opportunities held 76 per cent in AAA-rated papers and about 10 per cent in government securities as of May 2017. It had about 6 per cent in AA-rated papers with rest in cash and very short-term securities. The fund is managed by Anil Bamboli since inception.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

hi,

what is your opinion of reliance small cap fund.. i have 5000 rs monthly sip on other small caps like dsp microcap,franklin small companies . Also have sips in large cap / midcap/ balanced / diversified as well (total monthly sip around 45000) ..is reliance small cap fund good for a 10 – 15 year investment horizon .?

thanks

thomas

Small cap funds are currently finding it difficult to find opportunities and are moving a bit to midcaps. It is better to keep exposure restricted to 10-15% in this category. thanks, Vidya

Hi,

Please can you compare the ST with the HDFC Medium Term (MT) opportunities fund (and the HDFC liquid)

My perspective,

1. MT gains seems to be on the higher side. (same period approx 1 year)

2. MT is also classified as DEBT fund – so income taxation wise same as ST or Liquid.

3. Both have exit load NIL

So investor can come out at any point – need not wait until “Mid-Term” period is over.

(maybe in under 1 month as well)

4. Currently NAV for both is nearly the same.

5. So given point 1 and 3, why even park in HDFC Liquid ?

thanks

Jeevan.

(been investing thru FI for 5 years now and have invested in HDFC MT and Liquid)

Hi Jeevan,

This is a long reply 🙂 Please go through it carefully. We’ve provided links at the end for your better understanding. We’d urge you to read those too!

HDFC Short Term is a short-term debt fund. It’s average maturity is less than 2 years, with the portfolio yield at around 7.2%. HDFC Medium Term Opportunities is an income fund, with an average maturity of more than 3 years, and a yield of 7.5%. Both funds invest in different debt instruments -one invests in short-term papers and the other invests in long-term instruments. The holding period for both is different – HDFC ST needs 1.5 to 2 years and HDFC MT needs more than 2 years. HDFC Liquid is a liquid fund, which invests in commercial paper, treasury bills, certificate of deposits etc which are less than 90 days in maturity. Now, coming to your points:

1. MT gains seems to be on the higher side. Longer term funds usually deliver higher returns than shorter-term funds, since longer the duration, higher the risk. Also, it would be prudent to avoid looking at single point-to-point returns.

2. MT is also classified as DEBT fund – so income taxation wise same as ST or Liquid. HDFC MT, HDFC ST, HDFC Liquid are all debt funds; they all invest in debt instruments of banks, companies, and government. The average maturities and the nature of the instruments they invest in make each distinct from the other. All have the same taxation as they are all debt funds.

3. Both have exit load NIL. Even so, the holding period required for each fund is different. No exit load doesn’t mean you can get out at any time. You’d need to hold a fund for a certain period if you are to earn the best possible returns. An equity fund, for example, has an exit load up to one year, but you wouldn’t invest in an equity fund with a 1-year horizon, would you? Your chances of loss are high and you know that equity delivers best in the long term. Short-term and income funds have a part of their portfolio subject to market price fluctuations, so if you were to hold it only for a month, chances are you may be in losses. Short-term funds need a 1-2 year holding and income funds need a 2-year holding in order to earn the optimal returns. Please read this article:

4. Currently NAV for both is nearly the same. Absolute NAVs do not matter. A high NAV fund is not better or worse than a low NAV fund. Its the fund’s returns and potential to deliver returns that is important. This blog will tell you more.

5. So given point 1 and 3, why even park in HDFC Liquid? Liquid funds usually do not deliver losses even on a 1-day basis, since they invest in extremely short-term papers and have no component of their portfolio that is listed or has market prices. Other debt funds have this market price component. That’s why you have liquid funds. It is a higher-returning substitute for your bank account. You use it to park emergency money, or when you’d need the proceeds in a couple of weeks or at any time, or when you want to do STPs into equity. Liquid funds are not for you to earn high returns, and they will not match the returns of income funds or dynamic bond funds, or even short-term funds.

Please read the following blogs. It will help you understand the points above and debt funds better:

https://blog.fundsindia.com/blog/general/fundsindia-explains-what-are-debt-funds/8982

https://blog.fundsindia.com/blog/general/fundsindia-explains-how-do-debt-funds-deliver-returns/9021

You can also scroll through the articles here for a detailed understanding of each type of debt fund (and equity fund :-)) https://blog.fundsindia.com/blog/category/investment-definitions

Thanks,

Bhavana

Hi Bhavana – this is just to say ‘Thank You’ for giving a complete and very informative reply to the above query, and especially for attaching links to suitable articles at every point. Wonderful answer!

Yes truly a wonderful answer. Thanks a lot Bhavana.

Hi,

Please can you compare the ST with the HDFC Medium Term (MT) opportunities fund (and the HDFC liquid)

My perspective,

1. MT gains seems to be on the higher side. (same period approx 1 year)

2. MT is also classified as DEBT fund – so income taxation wise same as ST or Liquid.

3. Both have exit load NIL

So investor can come out at any point – need not wait until “Mid-Term” period is over.

(maybe in under 1 month as well)

4. Currently NAV for both is nearly the same.

5. So given point 1 and 3, why even park in HDFC Liquid ?

thanks

Jeevan.

(been investing thru FI for 5 years now and have invested in HDFC MT and Liquid)

Hi Jeevan,

This is a long reply 🙂 Please go through it carefully. We’ve provided links at the end for your better understanding. We’d urge you to read those too!

HDFC Short Term is a short-term debt fund. It’s average maturity is less than 2 years, with the portfolio yield at around 7.2%. HDFC Medium Term Opportunities is an income fund, with an average maturity of more than 3 years, and a yield of 7.5%. Both funds invest in different debt instruments -one invests in short-term papers and the other invests in long-term instruments. The holding period for both is different – HDFC ST needs 1.5 to 2 years and HDFC MT needs more than 2 years. HDFC Liquid is a liquid fund, which invests in commercial paper, treasury bills, certificate of deposits etc which are less than 90 days in maturity. Now, coming to your points:

1. MT gains seems to be on the higher side. Longer term funds usually deliver higher returns than shorter-term funds, since longer the duration, higher the risk. Also, it would be prudent to avoid looking at single point-to-point returns.

2. MT is also classified as DEBT fund – so income taxation wise same as ST or Liquid. HDFC MT, HDFC ST, HDFC Liquid are all debt funds; they all invest in debt instruments of banks, companies, and government. The average maturities and the nature of the instruments they invest in make each distinct from the other. All have the same taxation as they are all debt funds.

3. Both have exit load NIL. Even so, the holding period required for each fund is different. No exit load doesn’t mean you can get out at any time. You’d need to hold a fund for a certain period if you are to earn the best possible returns. An equity fund, for example, has an exit load up to one year, but you wouldn’t invest in an equity fund with a 1-year horizon, would you? Your chances of loss are high and you know that equity delivers best in the long term. Short-term and income funds have a part of their portfolio subject to market price fluctuations, so if you were to hold it only for a month, chances are you may be in losses. Short-term funds need a 1-2 year holding and income funds need a 2-year holding in order to earn the optimal returns. Please read this article:

4. Currently NAV for both is nearly the same. Absolute NAVs do not matter. A high NAV fund is not better or worse than a low NAV fund. Its the fund’s returns and potential to deliver returns that is important. This blog will tell you more.

5. So given point 1 and 3, why even park in HDFC Liquid? Liquid funds usually do not deliver losses even on a 1-day basis, since they invest in extremely short-term papers and have no component of their portfolio that is listed or has market prices. Other debt funds have this market price component. That’s why you have liquid funds. It is a higher-returning substitute for your bank account. You use it to park emergency money, or when you’d need the proceeds in a couple of weeks or at any time, or when you want to do STPs into equity. Liquid funds are not for you to earn high returns, and they will not match the returns of income funds or dynamic bond funds, or even short-term funds.

Please read the following blogs. It will help you understand the points above and debt funds better:

https://blog.fundsindia.com/blog/general/fundsindia-explains-what-are-debt-funds/8982

https://blog.fundsindia.com/blog/general/fundsindia-explains-how-do-debt-funds-deliver-returns/9021

You can also scroll through the articles here for a detailed understanding of each type of debt fund (and equity fund :-)) https://blog.fundsindia.com/blog/category/investment-definitions

Thanks,

Bhavana

Hi Bhavana – this is just to say ‘Thank You’ for giving a complete and very informative reply to the above query, and especially for attaching links to suitable articles at every point. Wonderful answer!

Yes truly a wonderful answer. Thanks a lot Bhavana.

hi,

what is your opinion of reliance small cap fund.. i have 5000 rs monthly sip on other small caps like dsp microcap,franklin small companies . Also have sips in large cap / midcap/ balanced / diversified as well (total monthly sip around 45000) ..is reliance small cap fund good for a 10 – 15 year investment horizon .?

thanks

thomas

Small cap funds are currently finding it difficult to find opportunities and are moving a bit to midcaps. It is better to keep exposure restricted to 10-15% in this category. thanks, Vidya