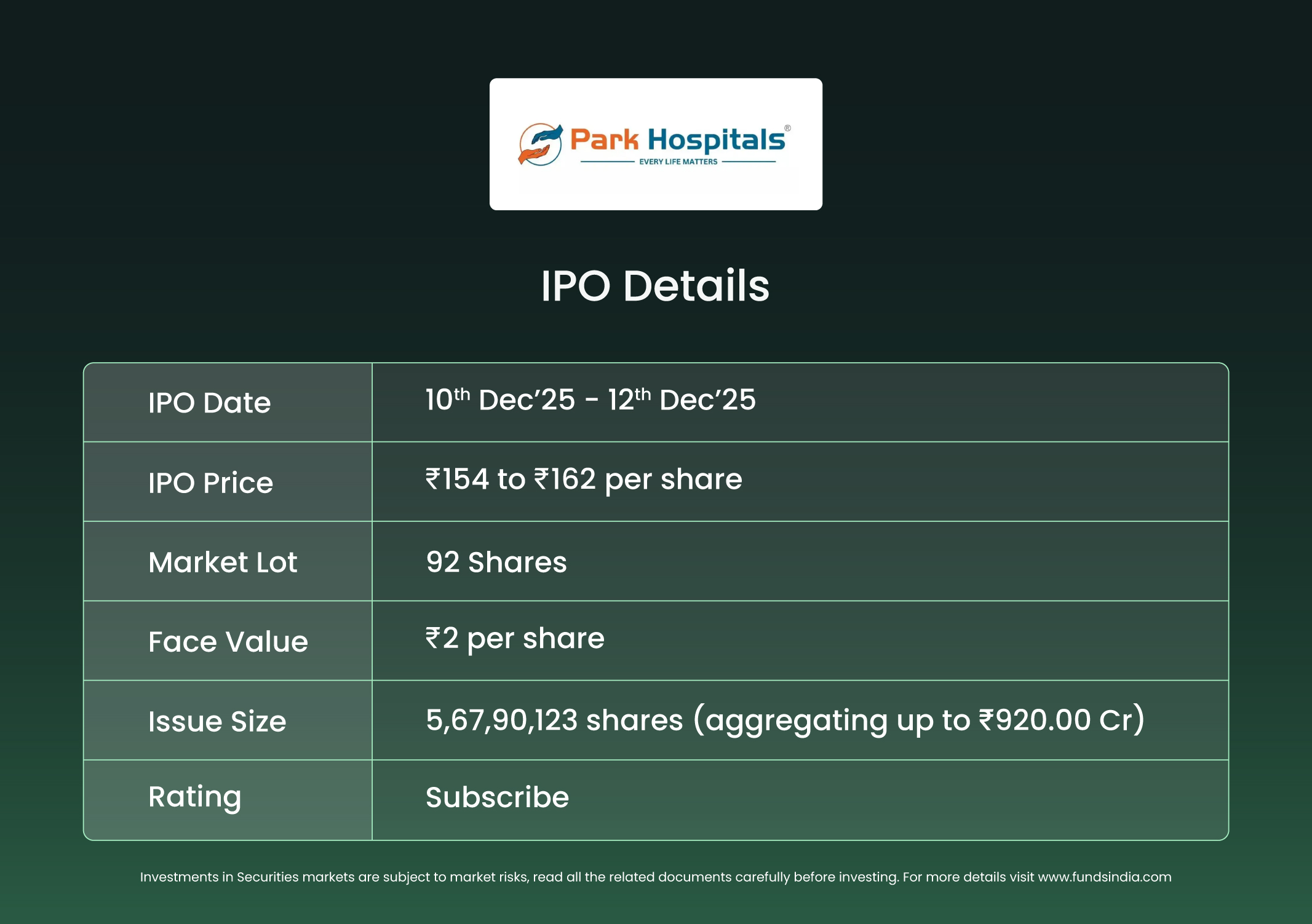

Company Overview

PMWL is a multi-super specialty healthcare services provider and the largest private hospital chain in North India by number of operational beds among peers. As of September 30, 2025, the company operated a cluster-based network of 14 NABH-accredited hospitals with a total capacity of 3,250 beds, including 870 ICU beds and 67 operation theatres, along with two dedicated cancer units, concentrated across Delhi, Haryana, Rajasthan and Punjab. It also has approvals to perform kidney transplants at five hospitals and has deployed robot-assisted surgery systems (iMARS) to support complex minimally invasive procedures. The company’s comprehensive healthcare services span across specialties such as cardiac sciences, neurosciences, orthopedics, transplant care, renal sciences, gastro sciences, and oncology.

Its business model is centred around pure-play healthcare services, with no revenue from sale of pharmaceutical or healthcare products reported in FY23–FY25, and in-patient services contributing over 95% of FY25 service income, while out-patient services form a relatively smaller share.

Objects of the offer

- To enable repayment/ prepayment, in full or in part, of outstanding borrowings availed by the Company and its Subsidiaries.

- To fund capital expenditure for development of new hospital by Subsidiary, Park Medicity (NCR).

- To fund capital expenditure for purchase of medical equipment by the Company and its Subsidiaries, Blue Heavens and Ratangiri.

- To fund unidentified inorganic acquisitions and general corporate purposes

Investment Rationale

- Strategic leadership in an undersupplied North India healthcare market – PMWL is the largest private hospital chain in North India by operational beds among peers, operating 3,250 beds across 14 NABH-accredited hospitals in Delhi, Haryana, Rajasthan and Punjab. North India has the lowest healthcare penetration among major regions in India, with only ~15–16 beds (global mean is 33 beds per 10,000 population) and ~7 doctors per 10,000 population yet is expected to grow at a 12–14% CAGR to Rs.3.3–3.4 trillion by FY29. PMWL primarily serves middle-income patients under government and PSU healthcare schemes, supported by robust empanelment. This enables high-volume, essential care delivery in regions where credible tertiary capacity is scarce, creating a market position that benefits from both structural undersupply and strong patient access pipelines through large institutional payors.

- Strong operational efficiency despite affordability-led pricing – PMWL operates with healthy utilization in high-acuity specialties, reporting 68.14% occupancy in H1FY26 and an ALOS (Average length of stay) of 6.53–6.66 days across FY24–FY25. Despite a significantly lower ARPOB (Average revenue per occupied bed) of Rs.27,105 in H1FY26 compared with premium chains such as Fortis Healthcare (Rs.68,200), Global Health (Rs.65,600) and KIMS (Rs.42,500), the company delivered a higher EBITDA margin of 26.85% in H1FY26 than these peers. It also maintains efficient asset deployment, with gross block per bed of Rs.3.65 million and fixed-asset turnover of 0.76x in H1FY26. This ability to sustain profitability at significantly lower price points reflects a cost-competitive operating model well aligned with high-volume underserved markets in North India.

- Financial Performance – The company delivered a consolidated revenue from operations of Rs.1,394 crore in FY25, rising 13% YoY from Rs.1,231 crore in FY24. EBITDA was recorded at Rs.372 crore in FY25 with a margin of 26.71% up from Rs.310 crore in FY24, marking a 20% YoY growth. PAT for FY25 stood at Rs.213 crore, translating to a margin of 15%, an increase of 40% YoY. Despite network expansion and newly added assets, the company maintained double-digit returns with ROE of 21% and ROCE of 17%.

Key Risks

- High Dependence on Government Schemes and PSUs – A significant majority of revenue is derived from government schemes and PSU-funded patients, making collections vulnerable to delayed payments or claim rejections from public agencies. Such delays may adversely affect cash flows and working capital.

- Geographic Concentration in Haryana – Hospitals in Haryana contributed 73.43% of revenue from operations in FY25. Any local regulatory tightening, policy changes, or adverse developments in the state may materially impact business performance.

- OFS-Risk – A substantial portion of the IPO is an Offer for Sale, allowing promoters to partly monetize holdings without a direct capital infusion into the business. The offer comprises the sale of stake worth Rs.1,500 million by promoter Dr Ajit Gupta.

Outlook

Park Medi World has demonstrated sustained revenue growth, strong operating margins, and efficient capital deployment within the North India hospital market. Its focus on high-acuity specialties, cluster-based expansion model, and affordability-led positioning provide a solid platform for continued scale and utilization improvement. A meaningful allocation of IPO proceeds toward debt reduction and network expansion is expected to strengthen balance sheet flexibility and support incremental bed additions. According to the RHP, Fortis Healthcare Ltd, Apollo Hospitals Enterprise Ltd, Max Healthcare Institute Ltd are a few of its listed peers. The peers are trading at an average P/E of 69.11x with the highest P/E of 101.54x and the lowest being 48.6x. At the higher price band, the listing market cap of Park Medi World will be ~Rs. 6,997 crore and the company is demanding a P/E multiple of 33x based on post issue diluted FY25 EPS of Rs.4.93. When compared with its peers, the issue seems to be fully priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.