Zensar Technologies Ltd – Enabling Enterprise Velocity

Headquartered in Pune, Zensar Technologies Ltd. is a leading technology solutions company. Zensar stands out as a premier technology services provider with a distinguished engineering pedigree. The company is focused on industry verticals, such as Hi-tech & Manufacturing, Consumer services, and Banking, Financial Services and Insurance (BFSI). The company has majority of its revenue coming from North America, followed by UK/Europe and South Africa. With 10,500+ workforce across 30+ global location (as on 31 March 2023), it is a part of USD 4.4 billion RPG Group. Founded by legendary industrialist Dr. R. P. Goenka, RPG Group is a global diversified business group with operations in the areas of Information Technology, Infrastructure, Tyres, Pharmaceuticals, Energy and Agribusiness.

Products and Services

The company offers majorly 5 key services:

Experience services: Experience design, Experience engineering, Brand, content and creative

Advance engineering services: Cloud strategy and operating model, Digital engineering, Cloud transformation and operations

Data engineering and analytics: AI and ML services, Automation, Visualisation and analytics, Data engineering

Application services: Application management, Quality engineering, Oracle services, Salesforce services, SAP services

Foundation services: Digital operations, Digital workspace, Digital security, Digital experience management, Digital infrastructure

Subsidiaries: As of 31 March 2023, the company had 14 Subsidiaries.

Key Rationale

- Significant wins – During Q3FY24, the company provided service to a connectivity platform provider, through Data Engineering and Analytics to integrate IoT in their cloud-based product aligned to IoT Security Architecture. It provided Integrated Advance Engineering Service solutions to tackle Security loopholes for one of the USA’s smart cities by reducing cost and advancing their existing technology to give better business uptime. The company also delivered end to end product engineering on microservice architecture for one of the largest payment corporations. Additionally, it provided digital foundational service to migrate and upgrade Global E-business instance on AWS cloud for one of the largest vacation ownership companies.

- Segment performance – Banking, Financial Services and Insurance (BFSI) grew 12.6% YoY, Manufacturing and Consumer Services grew by 5.5%. While the company had good volume growth across many of the service lines, revenue was impacted by seasonal headwinds. Hi-tech segment marked a decline in revenue by 9.6%. A reduction in revenue by 14% was experienced in Healthcare and Life Sciences segment as well. Region-wise, Europe and South-Africa generated 12% and 18% increase in year-over-year revenue, however in the US region revenue fell by 4.2%.

- Q3FY24 – Company recorded revenue of Rs.1,204 crores, a marginal growth of 1% compared to the Rs.1,198 crores of Q3FY23, revenue being taken down by the continued pressure in hi-tech vertical and higher furloughs. EBITDA increased from Rs.135 crores of Q3FY23 to Rs.208 crores in Q3FY24, a growth of 54%. Profit surged to Rs.162 crores, an increase of 113% compared to the same period in the previous year. The margins were hindered by weak performance of hi-tech segment. Order booking was $167.5 million which was about $37 million more than the same quarter last year.

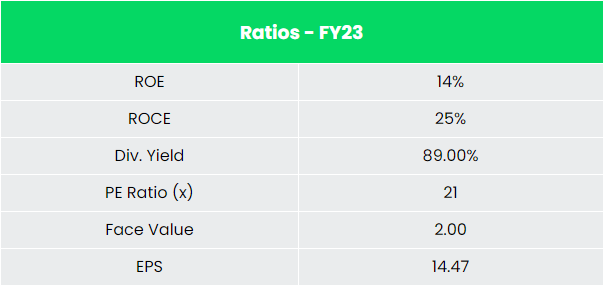

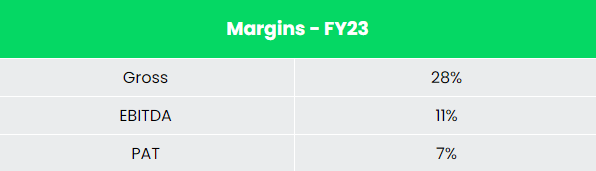

- Financial performance – The company has generated revenue and PAT CAGR of 9% and 6% over the period of 5 years (FY18-23). Average 5-year ROE & ROCE is around 14% and 19% for FY18-23 period. The company has robust capital structure with a debt-to-equity ratio of 0.07.

Industry

The IT & BPM sector has become one of the most significant growth catalysts for the Indian economy, contributing significantly to the country’s GDP and public welfare. The sector is consistently strengthening its digital capabilities by adopting deep tech technologies and focusing on deploying emerging technology solutions such as AI, Cybersecurity, and IoT. India’s IT industry is likely to hit the US$ 350 billion mark by 2026 and contribute 10% towards the country’s gross domestic product (GDP), India’s IT and business services market is projected to reach US$ 19.93 billion by 2025. The Indian software product industry is expected to reach US$ 100 billion by 2025. Data annotation market is expected to reach US$ 7 billion by 2030 due to accelerated domestic demand for AI. India is also amongst the fastest growing Fintech markets in the world. Indian FinTech industry’s market size is $50 Bn in 2021 and is estimated at ~$150 Bn by 2025.

Growth Drivers

In the Union Budget 2023-24, the allocation for IT and telecom sector stood at Rs. 97,579.05 crore (US$ 11.8 billion). Cabinet approved PLI Scheme – 2.0 for IT Hardware with a budgetary outlay of Rs. 17,000 crore (US$ 2.06 billion). Up to 100% FDI is allowed in Data processing, Software development and Computer consultancy services; Software supply services; Business and management consultancy services, Market research services, technical testing and Analysis services, under automatic route.

Competitors: Newgen Software Technologies Ltd, Cyient Ltd etc.

Peer Analysis

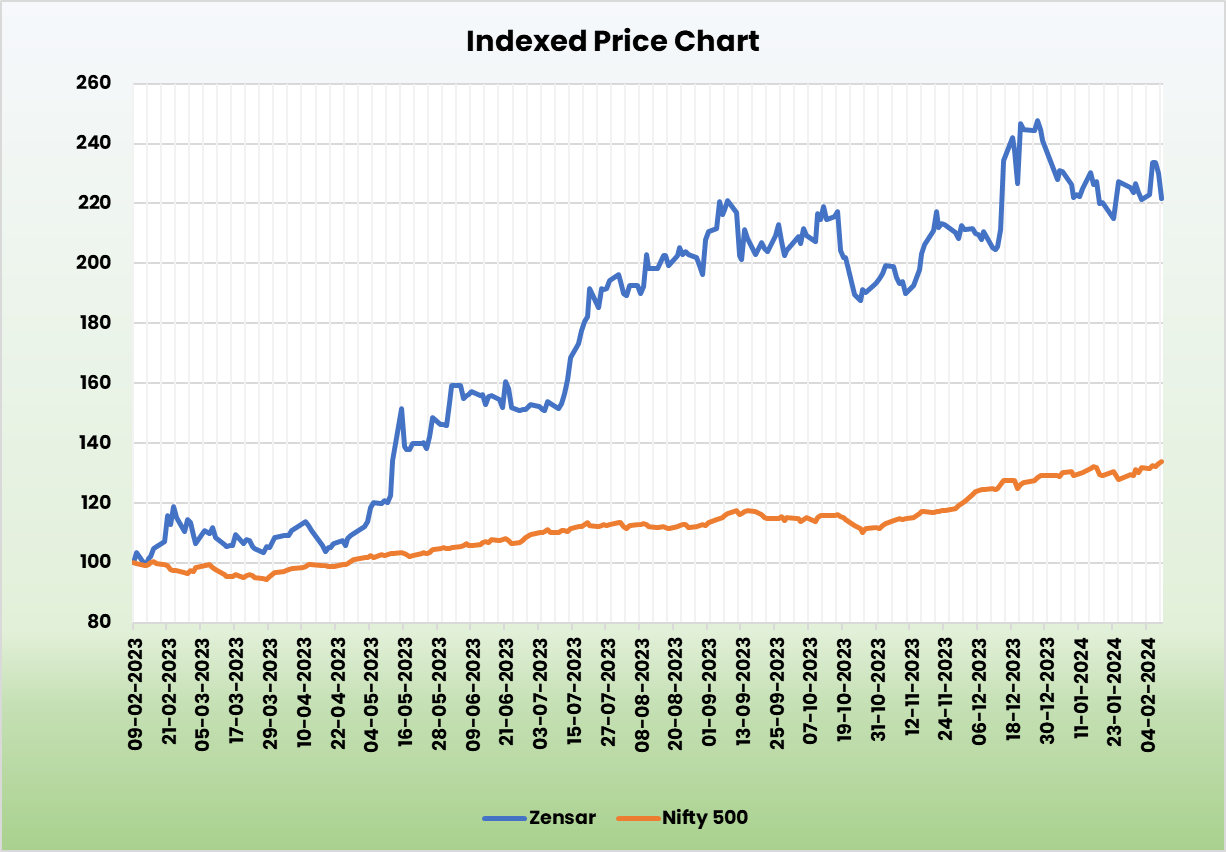

While comparing with the peers, Zensar is trading at a cheaper price to earnings ratio with an overall healthy performance metrics.

Outlook

The company’s management has expressed confidence on the growth of most of its verticals except for the hi-tech segment. The overall headwinds impacting the Hi-Tech industry and the extended furloughs impacted the performance of the company’s Hi-Tech segment as well. The company has M&A plans laid out, significantly for the Healthcare vertical. It has also started to see traction in the gen AI space as well. It has started exploring the med-tech and life science segments that have a broader scope for innovations compared to the payer segment, which is highly saturated.

Valuation

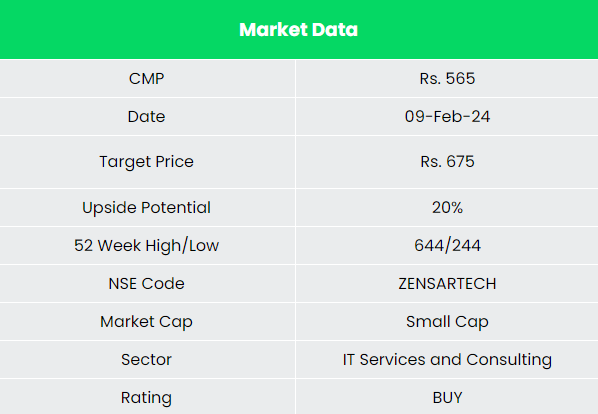

Zensar Technologies Ltd is in growth momentum in most of it’s key verticals barring hi-tech segment. We expect the impact of furloughs to reduce and hi-tech segment to recover in the mid to long term. We recommend a BUY rating in the stock with the target price (TP) of Rs. 675, 29x FY25E EPS.

Risks

- Forex Risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

- Uncertain demand environment – Due to recession threat in major economies, the global environment and economic conditions in key markets might weaken, derailing the company growth.