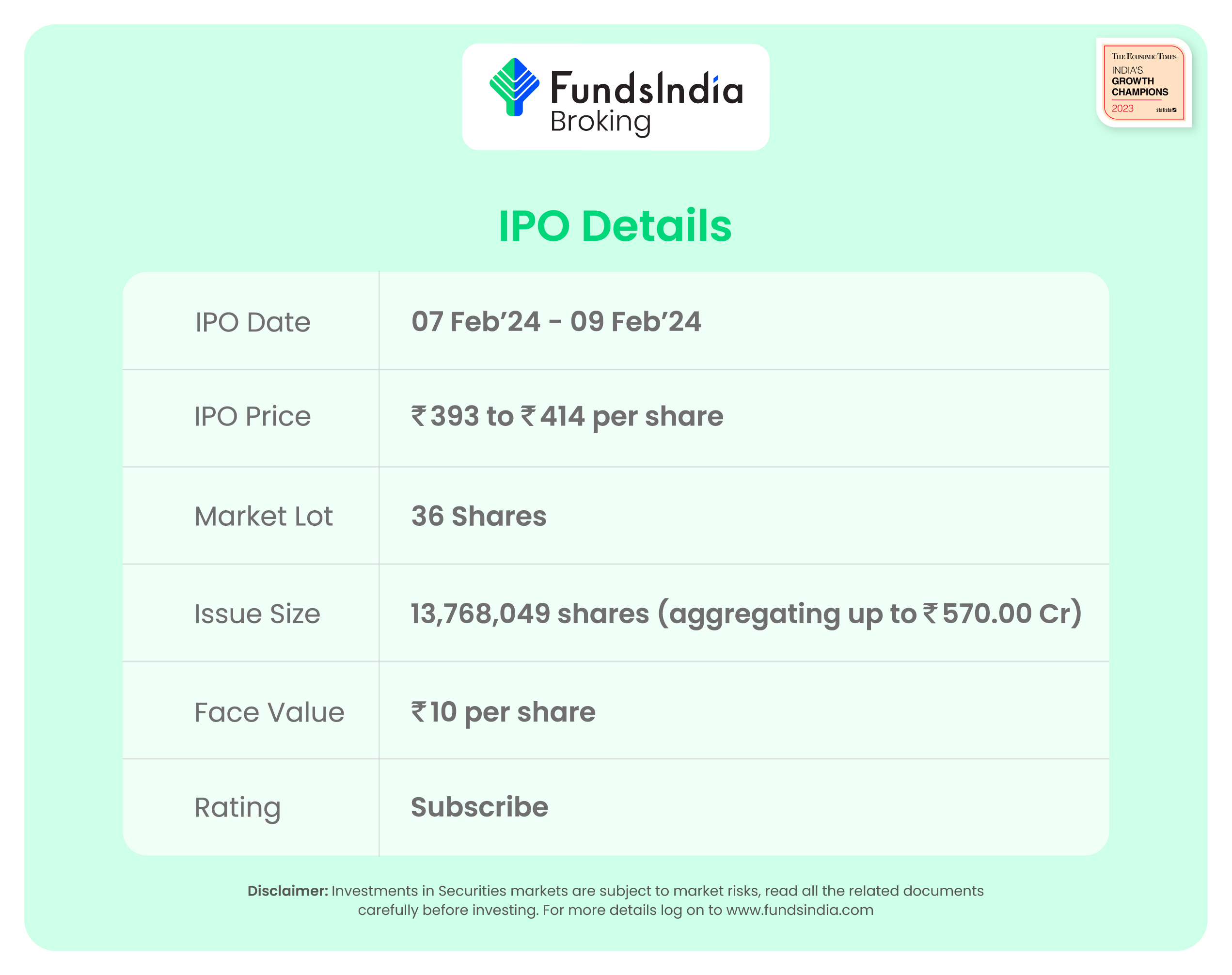

Company overview

Jana Small Finance Bank Limited is a small finance bank (SFB) with registered office in Karnataka. The bank’s primary products are deposits (demand deposits, savings deposits and term deposits) and advances. It offers secured loans, including micro loans against property, loans to micro, small and medium enterprises, affordable housing loans, term loans to non-banking finance companies, loans against fixed deposits, two-wheeler and gold loans, and unsecured loans, including individual and micro business loans, agricultural and allied loans, and loans offered to groups of women as per the joint liability group model. As of September 30, 2023, with 771 banking outlets in 22 states and two union territories the bank is the fourth largest SFB in terms of AUM and the fourth largest SFB in terms of deposit size.

Objects of the offer

- To utilize the Net Proceeds from the Fresh Issue towards augmenting Bank’s Tier – 1 capital base to meet future capital requirements, to improve Tier-I capital and CRAR. Further, the proceeds from the Fresh Issue will also be used towards meeting the expenses in relation to the Offer.

- To receive the benefits of listing the Equity Shares on the Stock Exchanges.

- Carry out offer for sale of up to 2,608,629 Equity Shares by the Selling Shareholders.

Investment Rationale

- Dominant position – The bank’s gross advances has increased from Rs.118,389.82 million as at March 31, 2021 to Rs.180,007.41 million as at March 31, 2023, representing a CAGR of 23.31%, and further increased to Rs.213,471.30 million as at September 30, 2023, an increase of 18.59%. The bank is focusing on increasing secured gross advances and within unsecured advances, the focus is on agricultural and allied loans. H1FY23 to H1FY24 Assets Under Management (AUM) and gross advances improved by 35% and 42% respectively.

- Fast growing retail deposit base – The bank offers a diverse range of deposit products to appeal to different customer segments. Deposit products comprise current accounts, savings accounts, recurring deposits and term deposits. Deposits increased from Rs.123,162.58 million as at March 31, 2021 to Rs.163,340.16 million as at March 31, 2023, representing a CAGR of 15.16%, and further increased to Rs.189,367.24 million as at September 30, 2023, an increase of 15.93%. The bank has strong emphasis on increasing lower interest rate retail deposit as compared to bulk deposits.

- Financial Track Record – The company reported interest income of Rs.3,075 crores in FY23 as against Rs.2,727 crores in FY22, an increase of 13% YoY. The interest income has grown at a CAGR of 11% between FY2021-23. The EBITDA of the company in FY23 was Rs.325 crores and EBITDA margin was at 11%. The PAT of the company in FY23 is at Rs.256 crores and PAT margin is at 8%. The CAGR between FY2021-23 of EBITDA is 45% and PAT is 88%. The ROE of the company stands at 17% in FY23. GNPA improved from 6.83% in H1FY23 to 2.44% in H1FY24. NNPA improved from 4.60% for H1FY23 to 0.87% for H1FY24.

Key risks

- OFS risk – In addition to fresh issue, the IPO will see the sale of upto 906,277 shares by Client Rosehill Limited, 929,656 shares by CVCIGP II Employee Rosehill Limited, 141,285 shares by Global Impact Funds, S.C.A., SICAR, sub-fund Global Financial Inclusion Fund, 413 shares by Growth Partnership II Ajay Tandon Co-Investment Trust, 998 shares by Growth Partnership II Siva Shankar Co-Investment Trust and 630,000 shares by Hero Enterprise Partner Ventures.

- Regulatory risk – The bank is subject to inspections by various regulatory agencies such as the RBI, PFRDA, IRDA and the National Pension System Trust. Non-compliance with the observations of such regulators could adversely affect its business, financial condition, results of operations and cash flows. In addition, some of these regulatory requirements and prudential norms are more onerous for SFBs compared to other banks.

- Default risk – The risk of non-payment or default by customers may adversely affect the company’s business, results of operations and financial conditions.

Outlook

According to RHP, AU Small Finance Bank Limited, Suryoday Small Finance Bank Limited, and Credit Access Grameen Limited are few of the listed competitors for Jana Small Finance Bank Ltd. The peers are trading at an average P/E of 31.67x with the highest P/E of 30.78x and the lowest being 24.21x. At the higher price band, the listing market cap of India Shelter Finance will be around ~Rs.4330.04 crores and the company is demanding a P/E multiple of 16.92x based on post issue diluted FY23 EPS of Rs.24.47. When compared with its peers, the issue seems to be fully priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.