Torrent Pharmaceuticals Ltd – Committed towards a healthier tomorrow

Incorporated in 1972 and headquartered in Ahmedabad, Torrent Pharmaceuticals Ltd. is a leading Indian pharma company with a strong presence across branded and unbranded generics, particularly in chronic and sub-chronic therapies, as well as consumer healthcare. As the flagship of the Torrent Group, the company ranks 7th in the Indian pharmaceutical market, is the leading Indian pharma player in Brazil, and is among the top five generics companies in Germany. Torrent operates across 50+ countries with major markets in India, Brazil, Germany and the US, supported by eight manufacturing facilities with several regulatory approvals and dedicated R&D and bio-evaluation centres.

Products and Services

The company operates across two business segments – branded generics and generics, with a portfolio spanning Cardiovascular, CNS, Gastro-Intestinal, Diabetology, VMN, Anti-Infective and Pain Management therapies.

Subsidiaries – As of FY25, the company has 19 subsidiaries and 1 associate company.

Investment Rationale

- Strong Chronic-Led Branded Portfolio Anchoring Growth – Torrent Pharma derives the majority of its revenue from a strong branded generics portfolio in India and Brazil, which together contribute 73% of overall revenue, with growth driven by chronic and sub-chronic therapies that form 76% of India sales. As chronic therapies are taken for long durations, often lifelong, they provide high patient stickiness, strong doctor loyalty, and sustained prescription momentum, reinforcing the company’s competitive positioning. Torrent ranks as the 6th largest player in chronic and sub-chronic segments and maintains leadership across Cardiac, Anti-Diabetic, CNS, GI and Dermatology, with an improvement in Gynaecology. Its brand strength is reflected in 21 products among the Top 500 in the Indian pharmaceutical market, including 18 mother brands (high revenue scale) with over Rs.100 crore annual sales, supported by a strong medical-rep network and ongoing expansion in core chronic areas such as diabetology.

- Diversified Portfolio with Emerging Derma Strength – The company benefits from a well-diversified portfolio across chronic, sub-chronic and select acute therapies, complemented by a steady pipeline of new launches and geographic expansion. The company is strengthening its presence in high-potential segments such as dermatology and consumer health – now supported by Shelcal and Curatio brands (dermatology-focused subsidiary) like Ahaglow and Dewsoft – at a time when consumers are increasingly willing to spend more on premium derma and cosmeceutical products. Torrent’s derma and consumer health franchise is also expanding internationally, with launches across the Philippines, Nepal and other Asian markets, while its broader global footprint is supported by a pipeline of over 60+ molecules filed with ANVISA in Brazil and multiple complex-generic filings in the US and Europe. The company is further enhancing its specialty profile through peptide-based products, including the semaglutide filing in Brazil, and has secured patents such as the Mecobalamin Nasal Spray and Tapentadol nasal composition, reinforcing its innovation capability. Alongside this, Torrent continues to strengthen core chronic areas – Cardiology, Anti-Diabetic, CNS and Gastro – through initiatives such as the acquisition of three anti-diabetes brands from Boehringer Ingelheim and the licensing of Vonoprazan from Takeda. This combination of a broad therapy portfolio, a growing consumer-care engine and expanding geographic reach positions the company for sustained and diversified growth.

- Strategic Value Creation Through JB Chemicals Acquisition – Torrent Pharma has proposed the acquisition of a controlling stake in JB Chemicals & Pharmaceuticals Ltd. and has already received CCI approval. This presents a significant long-term value catalyst, strengthening its branded-generics leadership in chronic and sub-chronic therapies. JB Chemicals brings complementary portfolios in Cardiac, Gastro and Pain management, along with strong brands such as Cilacar and Rantac, enhancing Torrent’s India scale and doctor-coverage depth. The acquisition also adds a high-quality field force, improves therapy-area concentration and expands Torrent’s presence in Tier-2/3 markets. Once completed, the merger structure is expected to unlock operating synergies across procurement, manufacturing, distribution and field-force productivity, while broadening Torrent’s revenue base with JB’s steady, brand-led India business model.

- Q2FY26 – During the quarter, the company generated revenue of Rs.3,302 crore, achieving an increase of 14% as compared to the Rs.2,889 crore of Q2FY25. The company’s chronic business grew at 13% versus the IPM (Indian Pharmaceutical Market) chronic growth of 11%, driven by outperformance in cardiac and gastro segments. EBITDA improved by 15% YoY, from Rs.939 crore to Rs.1,083 crore. Net profit stood at Rs.591 crore, a growth of 30% from Rs.453 crore of Q2FY25 despite the headwinds in Germany due to major supplier facing supply chain disruptions. For the company, the period marked a 12% growth in India, 21% in Brazil and a 5% de-growth in Germany.

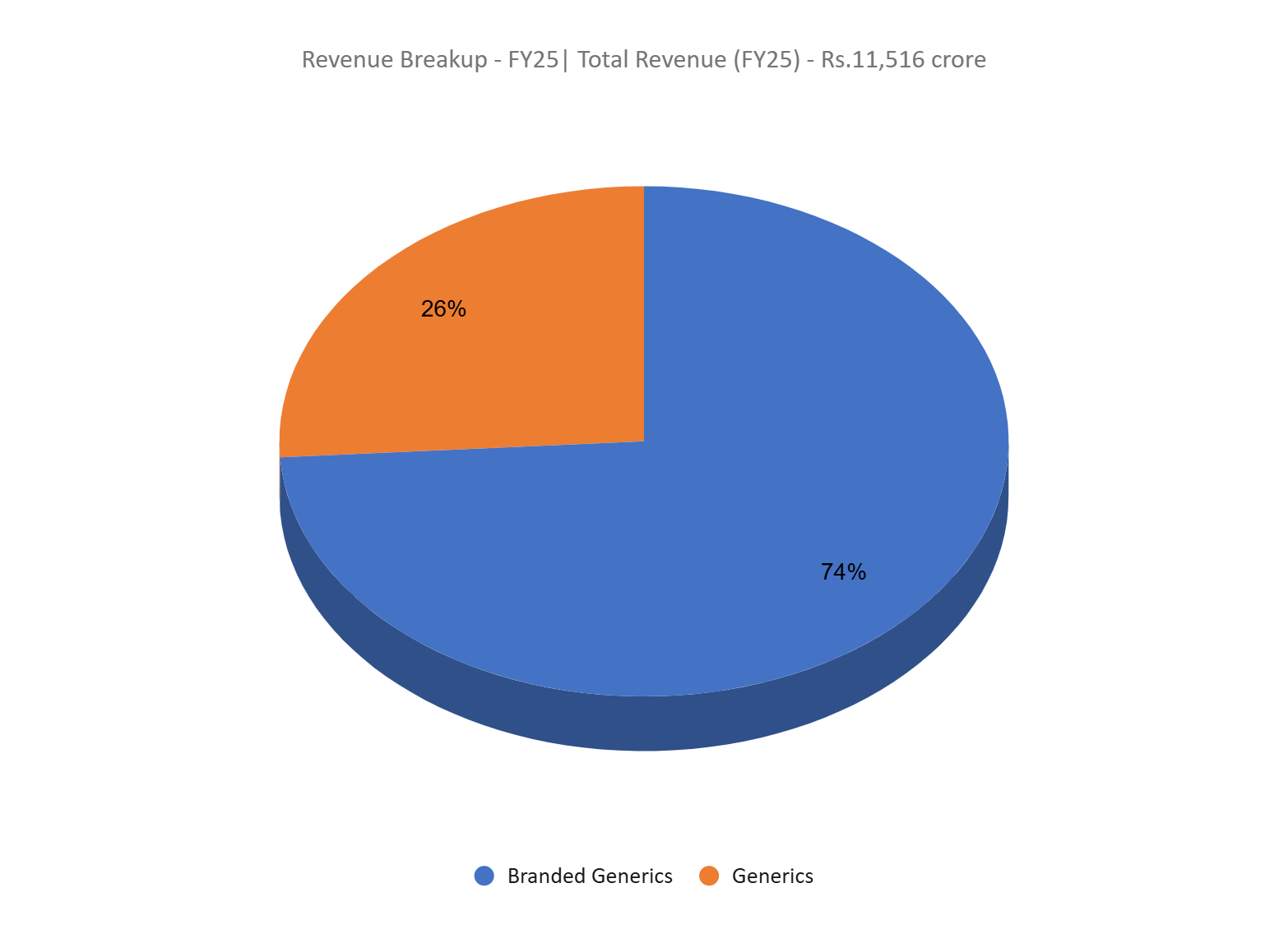

- FY25 – The company generated revenue of Rs.11,516 crore during FY25, an increase of 7% compared to the FY24 revenue. EBITDA was at Rs.3,721 crore, up by 10% YoY. The company reported net profit of Rs.1,911 crore, an increase of 15% YoY.

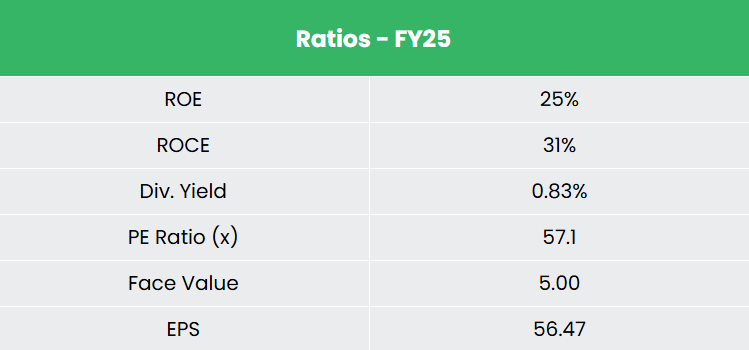

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 11% and 21% between FY23-FY25. The 3-year average ROE and ROCE for the company is around 24% and 21% for the past 3 years. The company has a robust capital structure with a debt-to-equity ratio of 0.33.

Industry

The Indian pharmaceutical industry is a global leader in generic medicines and low-cost vaccines, ranking as the world’s 3rd largest market by volume and 14th by value. Sector growth is being driven by rising healthcare demand, increasing chronic disease incidence, and India’s expanding role as a reliable supplier of affordable medicines. According to Bain & Co., the Indian pharmaceutical market was valued at Rs.4,71,295 crore (US$ 55 billion) in 2025 and is projected to reach Rs.10,28,280–11,13,970 crore (US$ 120–130 billion) by 2030. India contributes 20% of global generic exports by volume and supplies 60% of global vaccine demand, underscoring its manufacturing depth and cost advantages. Government initiatives aimed at self-reliance, domestic API manufacturing, and enhanced R&D capabilities are further strengthening India’s position in global pharmaceutical supply chains. Rising income levels, broader health insurance coverage, and a structural shift toward chronic therapy consumption continue to support sustained industry growth.

Growth Drivers

- 100% FDI is permitted under the automatic route for greenfield pharmaceutical projects, with 74% permitted for brownfield investments.

- India’s growing middle class, expanding healthcare access, and increasing prevalence of chronic illnesses such as diabetes, cardiovascular disorders, and CNS conditions continue to drive long-term demand.

- Allocation of Rs.5,268.72 crore (US$ 602.90 million) in the Union Budget 2025-26 towards Department of Pharmaceuticals (DoP).

Peer Analysis

Competitors – Cipla Ltd, Dr Reddys Laboratories Ltd, etc.

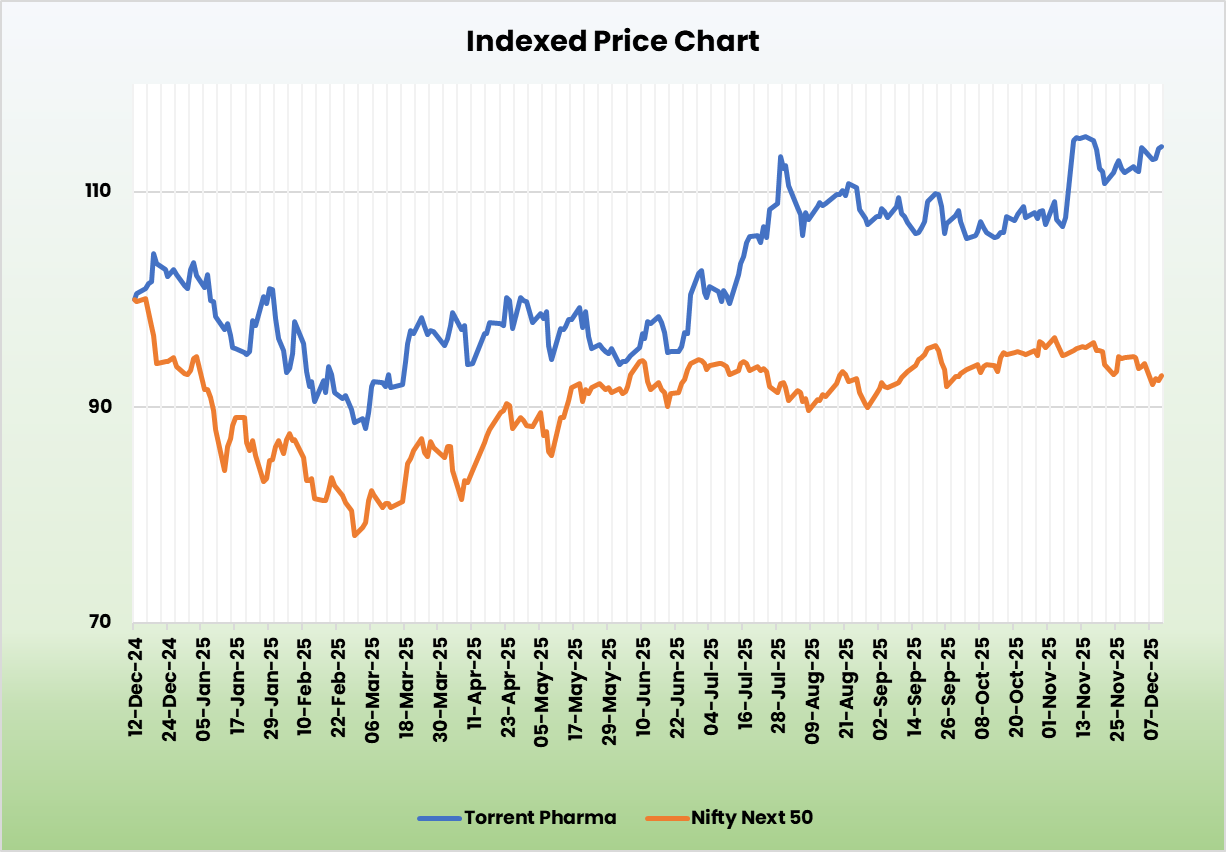

Compared to its peers, the company demonstrates disciplined capital allocation and strong overall financial performance.

Outlook

Torrent Pharma’s outlook remains strong, supported by high prescription stickiness in chronic therapies and sustained doctor pull. The company is simultaneously widening its international footprint across the Philippines, Nepal and Latin America, while building future growth engines through complex generics, peptides and a robust pipeline of filings in regulated markets. Management remains upbeat on accelerating growth for the Curatio portfolio in FY26, supported by an expanding field force of 7,000 MRs, including 600 additions during the year. The company expects 8 – 10 launches in Brazil and around 10 launches in the US in FY26, alongside 4 – 5 new products already introduced in Q1, including the key launch of Esomeprazole. This blend of therapy diversification, consumer-health momentum and expanding geographic scale positions Torrent for sustained medium-term growth.

Valuations

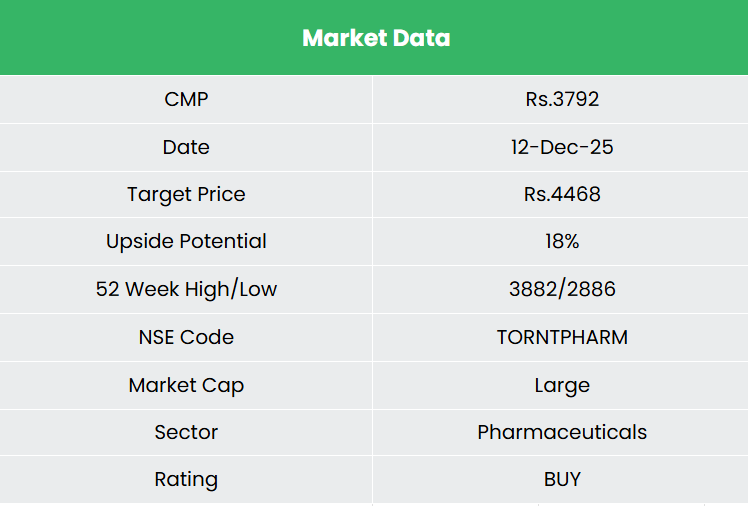

A robust chronic-led portfolio, scale-up in key markets and synergy gains from upcoming integrations position Torrent for sustained earnings growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.4,468, 40x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

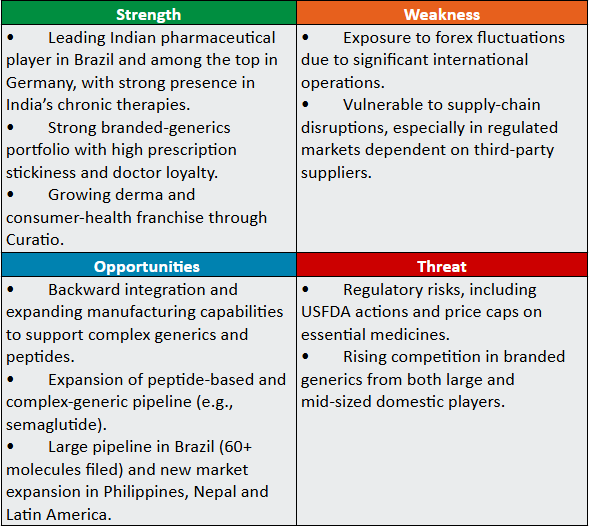

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.