Jindal Stainless Ltd – A Legacy Synonymous with Stainless Steel

Jindal Stainless Ltd (JSL), a flagship company of the OP Jindal Group, is a leading global manufacturer of high-quality stainless steel products. Incorporated in 1980 and headquartered in New Delhi, JSL ranks among the top five stainless steel producers worldwide (excluding China). The company operates 16 manufacturing and processing facilities across India, Spain, and Indonesia (as of March 2025), with a commercial presence in over 12 countries. With the capability to produce more than 120 grades of stainless steel, JSL serves a diverse range of sectors including automotive, infrastructure, consumer durables, and industrial applications.

Products and Services

Product range includes stainless steel slabs, blooms, coils, plates, sheets, precision strips, wire rods, rebars, blade steel, and coin blanks serving core sectors such as railways, automotive, infrastructure, consumer durables, and oil & gas.

Subsidiaries: As of FY25, the company has 19 subsidiaries, 3 associates and 2 joint venture companies.

Investment Rationale

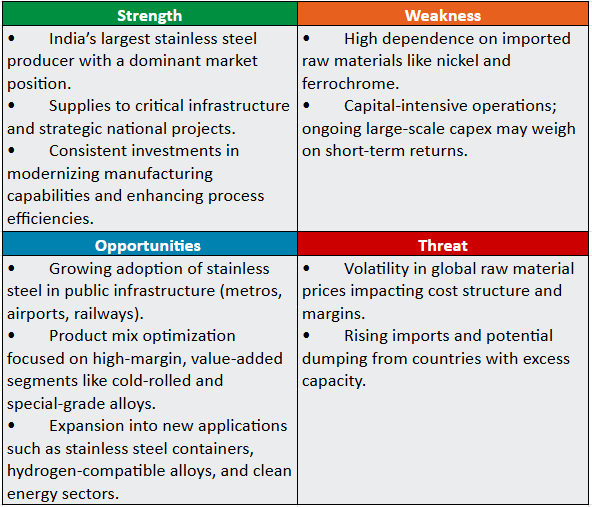

- Building Scale and Capability Through Strategic Acquisitions – JSL is pursuing strategic acquisitions to strengthen its value chain, expand product capabilities, and enhance operational efficiency. The company has acquired the remaining 46% stake in Chromeni Steels Ltd. in FY25, making it a wholly owned subsidiary. This move significantly bolstered JSL’s cold rolling (CR) capacity, improved operational integration and enhanced efficiency across the value chain. The Mundra-based facility, with a capacity of 0.6 MTPA and strategic proximity to the port, offers logistics advantages for both imports and exports. The company aims to enhance the capacity from current ~55-60% to 70-75% by Q3/Q4 FY26, a significant step in assisting the company to focus to its strategic goal of raising CR product share from ~45% to 75%. Through a JV with New Yaking Pte. Ltd., the company has commissioned a world-class Nickel Pig Iron smelter with a nameplate capacity of 200,000 MT annually (14% nickel content). This move secures critical raw material for stainless steel production, a vital step given India’s limited nickel reserves. It strengthens cost competitiveness and ensures better margin protection via backward integration.

- Capacity Expansion & Forward-Looking Growth Initiatives – JSL has outlined a robust capacity expansion and sectoral diversification strategy centered on premiumization, infrastructure readiness, and global competitiveness. The company plans to scale its capacity from 3.0 MTPA to 4.2 MTPA by FY26/27, supported by strong volume growth (8% YoY in Q1FY26) driven by demand from automotive, railways, elevators, and white goods sectors. Key growth levers include an enhanced product mix with a 35 – 40% contribution from value-added products and increased stainless steel adoption in public infrastructure projects such as metros and airports. Major investments comprise Rs.3,350 crore towards expanding downstream capacity and infrastructure at Jaipur, alongside a greenfield facility in Maharashtra targeting specialized grades for hydrogen, nuclear, defense, and clean energy applications, with phased capacity additions up to 4 MTPA. On the international front, JSL is setting up a stainless steel melt shop in Indonesia to bolster raw material security. Additionally, in FY25, JSL partnered with CJ Darcl Logistics to develop lightweight, high-strength stainless steel containers, successfully fabricating and deploying an initial batch of 50 units – signalling its foray into the growing sustainable logistics segment.

- Q1FY26 – During the quarter, the company generated revenue of Rs.10,207 crore, an increase of 8% compared to the Rs.9,430 crore of Q1FY25. EBITDA improved by 8% YoY to Rs.1,310 crore compared to Rs.1,210 crore. Net profit stood at Rs.715 crore as against the Rs.646 crore of Q1FY25, an increase of 11%.

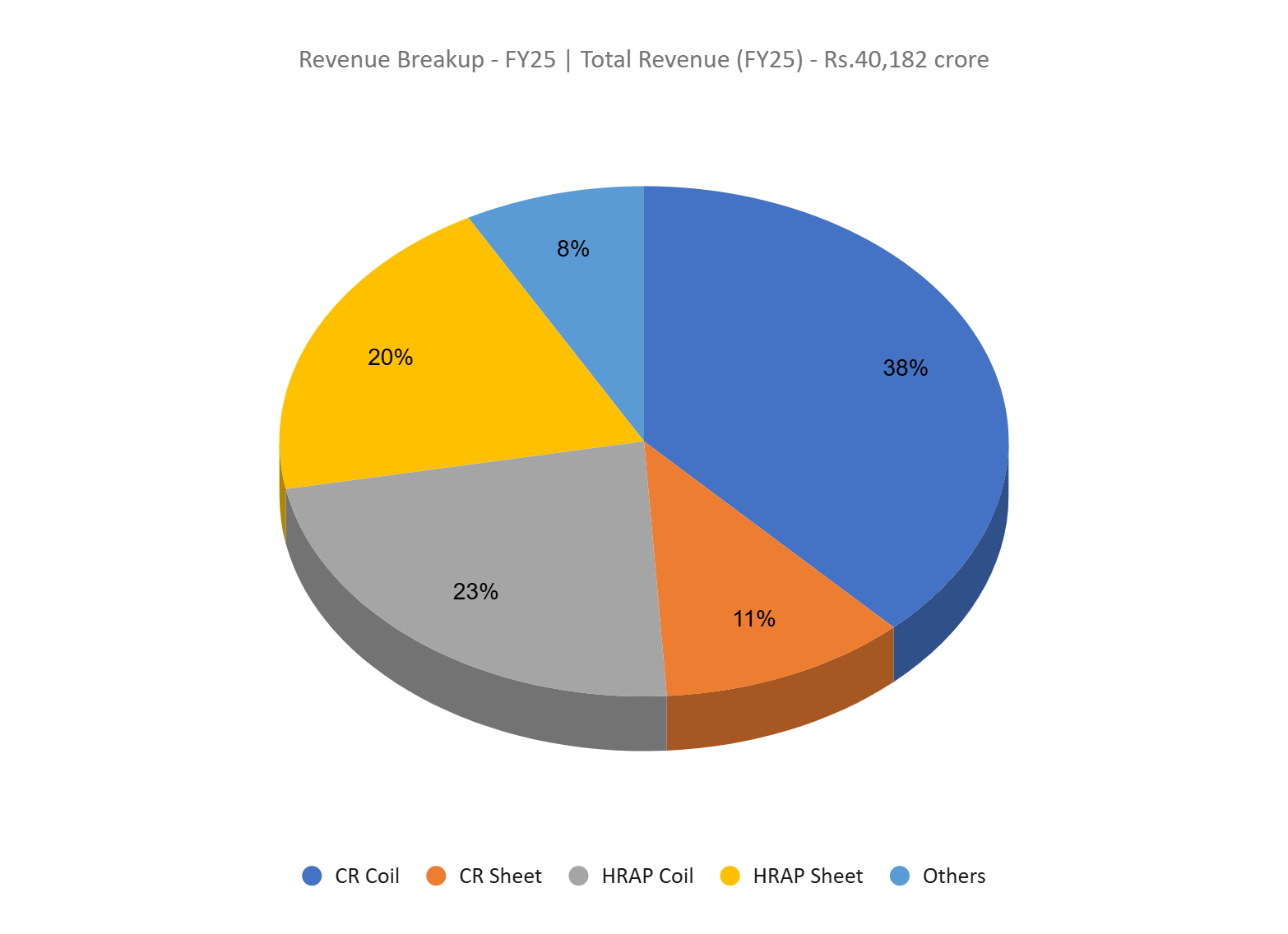

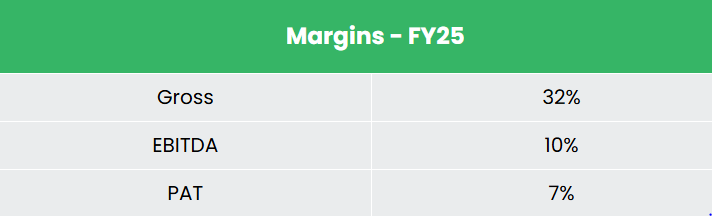

- FY25 – The company generated revenue of Rs.40,182 crore, an increase of 5% compared to FY24 revenue. Volume increased by 9% YoY, with strong demand from railway, automotive, infra, oil & gas and pipes and tubes segment. However, operating profit declined by 3% to Rs.3,905 crore, primarily due to pricing pressure and adverse inventory valuation, impacted by challenging global economic conditions. The company posted net profit of Rs.2,711 crore, a jump of 7% YoY.

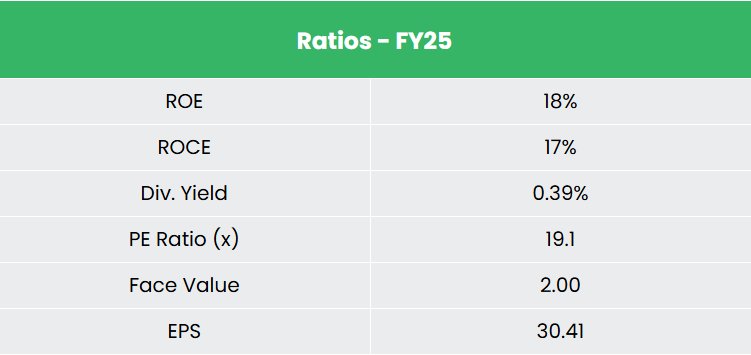

- Financial Performance – Average 3-year ROE & ROCE is around 18% and 20% for FY23-25 period. The company has a robust capital structure with a debt-to-equity ratio of 0.38.

Industry

Stainless steel, known for its corrosion resistance, durability, and smooth finish, has become a critical material across industries such as construction, automotive, infrastructure, and energy. Globally, the stainless steel market has grown at a steady rate, outpacing other metals like carbon steel, aluminium, and copper, driven by urbanization, infrastructure expansion, and demand from sectors like automotive, LNG, and renewables. In India, the market is witnessing strong growth supported by rising applications in railways, transport, manufacturing, and emerging sectors such as green hydrogen, nuclear energy, and defence. India is now the second-largest consumer and third-largest producer of stainless steel, playing a key role in the country’s push towards becoming a global manufacturing hub, with demand expected to rise steadily on the back of economic growth, infrastructure development, and favourable policy support.

Growth Drivers

- Increased government spending in sectors like railways, construction, automobiles, consumer goods, and process industries is expected to boost stainless steel consumption.

- The Government of India aims to reduce steel imports by 50% by FY26 and position the country as a net exporter in the near future.

- 100% Foreign Direct Investment (FDI) is permitted under the automatic route in the steel sector.

Peer Analysis

Competitors: JSW Steel Ltd, Tata Steel Ltd, etc.

Among its peers, the company stands out with strong revenue growth and superior performance ratios, reflecting its financial stability and operational efficiency in generating returns on invested capital.

Outlook

JSL is poised for robust growth in FY26, backed by a committed capex plan of Rs.2,700 – Rs.2,800 crore and an ambitious volume growth target of 9 – 10%. The company anticipates an EBITDA per tonne range of Rs.19,000 – Rs.21,000, underpinned by improving operational efficiencies and a favourable product mix. Export volumes are expected to surge by 25%, reflecting the company’s expanding global footprint. Strategic acquisitions and focused R&D initiatives have significantly enhanced the product portfolio, increasing the share of cold-rolled and value-added products to 60% of wider coils – aligning JSL with global industry benchmarks. With cold-rolled products commanding superior demand and margins, the company’s pivot towards premiumization is clear. Additionally, JSL’s entry into the stainless-steel container segment further diversifies its value-added offerings, reinforcing its growth and margin expansion trajectory.

Valuation

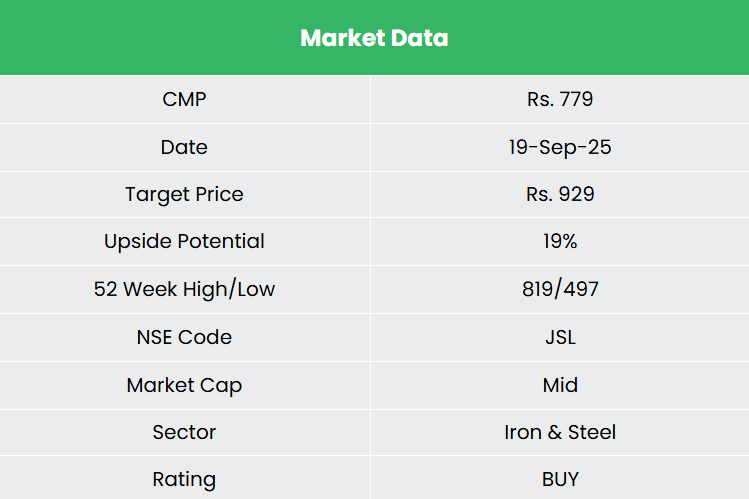

We believe the JSL’s focused expansion strategy, ongoing product mix enhancement, and cost optimisation efforts position the company well to sustain its growth trajectory and strengthen its competitive edge in the evolving stainless steel landscape. We recommend a BUY rating in the stock with the target price (TP) of Rs.929, 28x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.