Caplin Point Laboratories Ltd – Be Unique. Go Big.

Caplin Point Laboratories Ltd. is a fast growing fully integrated pharmaceutical company with a dominant position in emerging markets of Latin America (LATAM), Francophone Africa and a growing presence in the regulated markets such as USA & EU. Established in 1990 to manufacture a range of ointments, creams and other external applications, currently the company has its presence across all critical and value driven spots on the pharmaceutical value chain right from APIs to Finished Formulations; Research & Development; Clinical Research; Contract Research Organization (CRO); Marketing & Distribution; Online Platform for Pharmacy Automation, etc.

Products and Services

Caplin’s product list comprises of tablets, capsules, injections (liquid & lyophilized, pre-filled syringes), softgel capsules, liquid orals, ointments, cream and gels, powder for injections, suppositories and ovules, pre-mix bags and inhalers, sprays, etc.

Subsidiaries: As of FY24, the company has 13 subsidiaries and 1 associate company.

Investment Rationale

- Performance in emerging markets – The company continues to strengthen its footprint across emerging markets, with a strategic focus on LATAM. It is in the process of finalising new partnerships and filing additional dossiers in Mexico and Chile. It has also expanded its infrastructure in the region, establishing new manufacturing facilities and warehouses. In the first phase, it plans to manufacture oral liquids and dermatology range of products. In Mexico, over 35 product dossiers have been filed, with 17 approvals already secured. An additional pipeline of 80+ products is expected to be filed over the next 12 months. The company has secured government tenders worth approximately US$7.6 million in a key Central American market, with supplies scheduled for Q2 and Q3 of FY26. The company’s General API facility in Vizag has been completed and is currently undergoing GMP certification. This will enable backward integration for select Injectable and Oral Solid Dosage (OSD) products targeted at the LATAM region. Additionally, the company has recently acquired 100% stake in Neoethicals Chile SpA in Chile and Triwin Pharma in Mexico, further strengthening its marketing and distribution channels.

- Performance in regulated markets – The company expanded into the U.S. regulated market with the incorporation of Caplin Steriles USA Inc. in FY24. The subsidiary turned profitable within the first few quarters, driven by launches in injectables, emulsions, and ophthalmic products. 21 products have been launched to date, with 15 more in the pipeline. During Q1FY26, the company secured key USFDA approvals include generics of COMBIGAN (ophthalmic), Vitamin K1 injection, and HALDOL (long-acting injectable), validating the company’s sterile manufacturing and regulatory strengths. This early traction in a high-margin market supports robust earnings visibility and positions Caplin as an emerging player in the U.S. generics space. The company is also increasing its filings and approvals in markets such as Canada, Mexico, Saudi Arabia, UAE, and South Africa, which are expected to positively impact its financial performance in the near future.

- Q1FY26 – During the quarter, the company generated revenue of Rs.510 crore, achieving an increase of 11% as compared to the Rs.459 crore of Q1FY25. EBITDA improved by 18% YoY, from Rs.170 crore to Rs.201 crore. Net profit stood at Rs.151 crore, a growth of 21% from Rs.125 crore of Q1FY25.

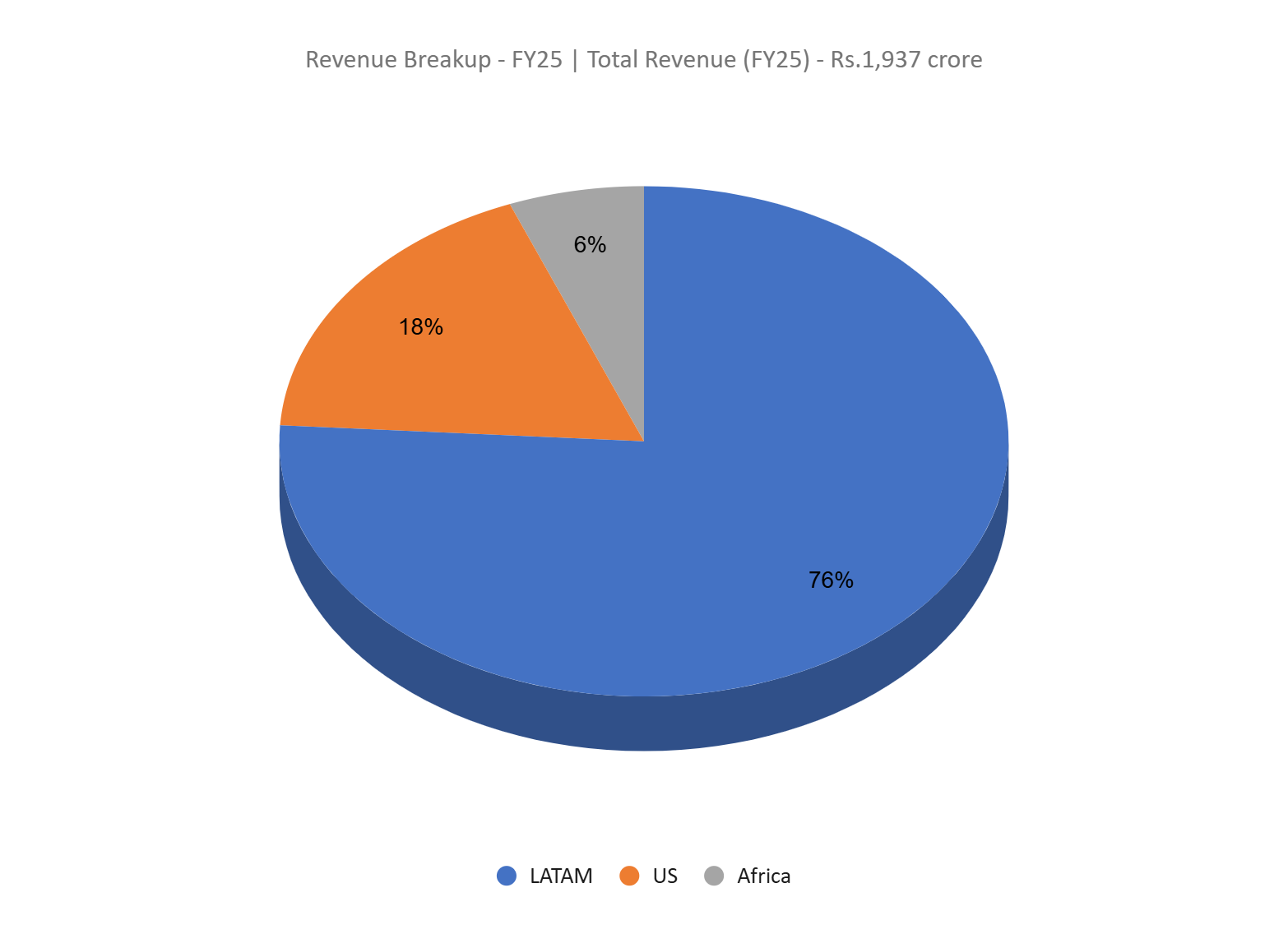

- FY25 – The company generated revenue of Rs.1,937 crore during FY25, an increase of 14% compared to the FY24 revenue. EBITDA was at Rs.743 crore, up by 20% YoY. The company reported net profit of Rs.541 crore, an increase of 17% YoY.

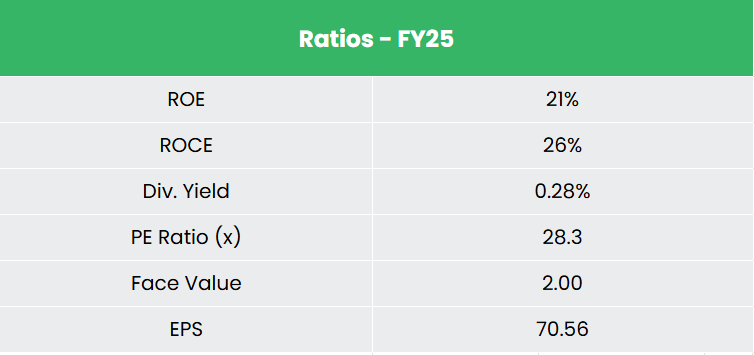

- Financial Performance – The revenue and PAT CAGR of the company for the past 3 years is around 15% and 21% between FY23-FY25. The 3-year average ROE and ROCE for the company is around 24% and 26% for the past 3 years. The company has a balance sheet without any debt in its capital structure.

Industry

India’s pharmaceutical industry, backed by strong innovation, cost-effective manufacturing, and government support, is poised for significant growth – projected to expand at a CAGR of over 10% to reach USD 130 billion by 2030 and USD 450 billion by 2047. Globally recognized as the “Pharmacy of the World,” India is the largest supplier of generic medicines and fulfills over 50% of global vaccine demand, exporting to more than 200 countries. The country ranks third worldwide in pharmaceutical production by volume and plays a vital role in ensuring affordable healthcare access across the globe. Additionally, India’s medical technology sector is gaining traction, with exports expected to reach USD 20 billion by FY2030. This dynamic and expanding industry continues to offer attractive opportunities for investors and stakeholders alike.

Growth Drivers

- Up to 100% Foreign Direct Investment (FDI) is permitted in the pharmaceutical sector, with greenfield projects allowed under the automatic route, while brownfield projects allow up to 74% under the automatic route and any investment beyond that requires government approval.

- Allocation of Rs. 5,268.72 crore (US$ 602.90 million) in the Union Budget 2025-26 towards Department of Pharmaceuticals (DoP).

- Well-suited infrastructure for clinical trials, combined with a large pool of skilled professionals.

Peer Analysis

Competitors: Zydus Lifesciences Ltd & ERIS Lifesciences Ltd, etc.

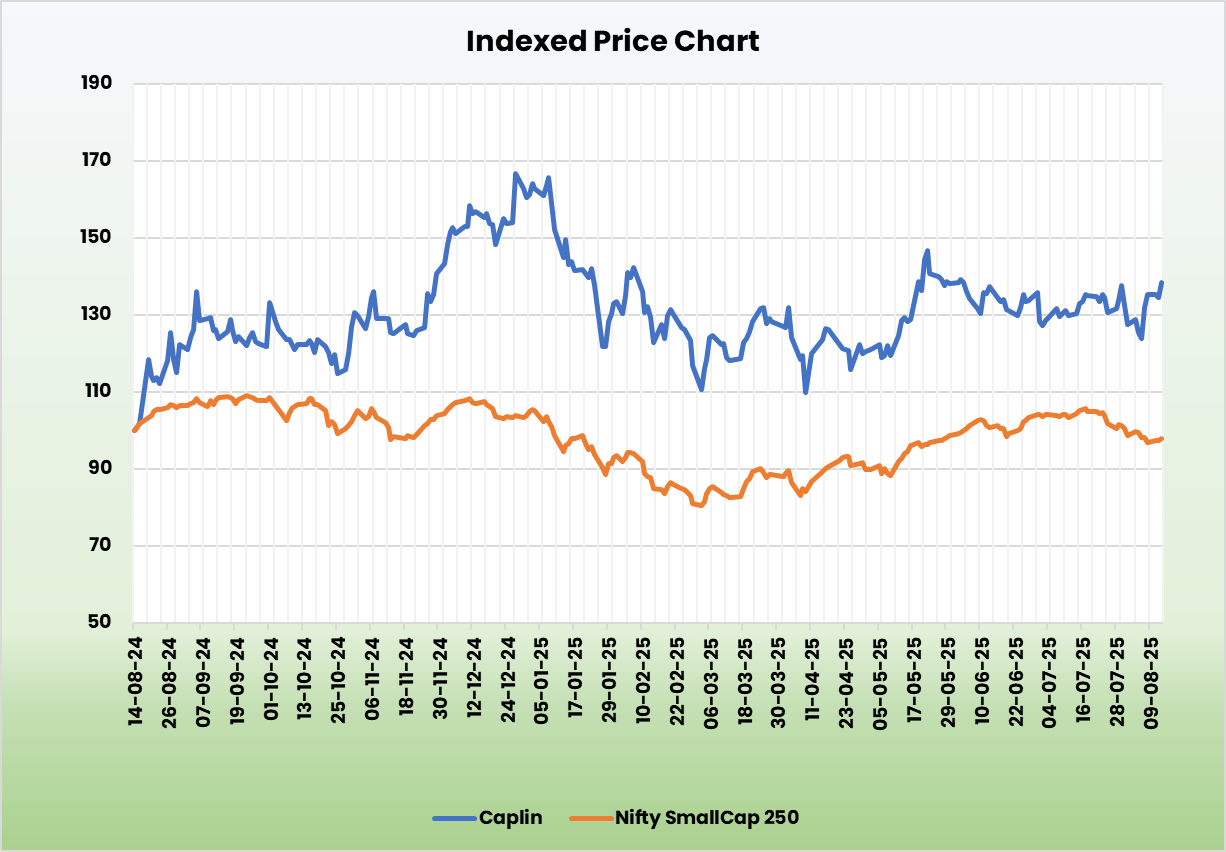

Among its peers, Caplin has demonstrated steady revenue growth along with superior capital returns and strong earnings potential, reflecting its financial stability and efficient capital allocation.

Outlook

We believe the company is poised for sustained growth, backed by a strong focus on emerging markets, a robust R&D pipeline, and ongoing capacity expansion. Key projects include an oncology API facility in Thervoy and a dual-chamber syringe line in Puducherry for the LATAM market – both targeting high-margin, low-competition segments. The company’s integrated approach – spanning backward integration, onshore manufacturing, and owned distribution – enhances supply chain efficiency and margins. With all expansions funded through internal accruals, Caplin remains committed to a debt-free, asset-light model, ensuring financial strength and long-term value creation.

Valuation

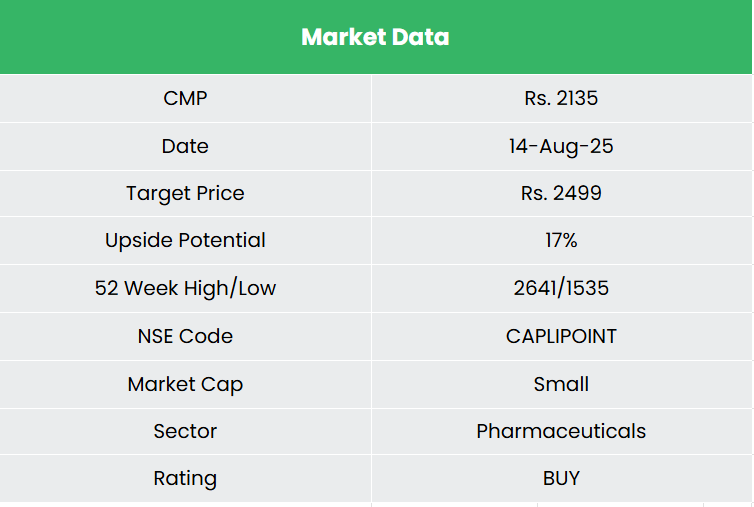

The company’s focus on underserved markets with strong demand potential positions it well for sustainable mid- to long-term growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,499, 26x FY27E EPS.

Note: We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

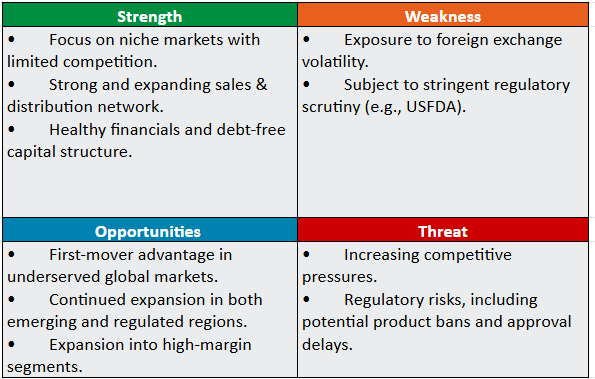

SWOT Analysis

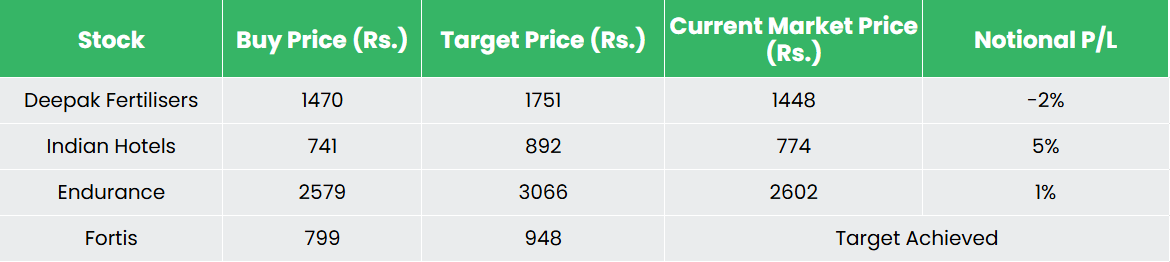

Recap of our previous recommendations (As on 14 August 2025)

Deepak Fertilisers & Petrochemicals Corp Ltd

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.