Key Highlights

1. Fiscal Consolidation on track

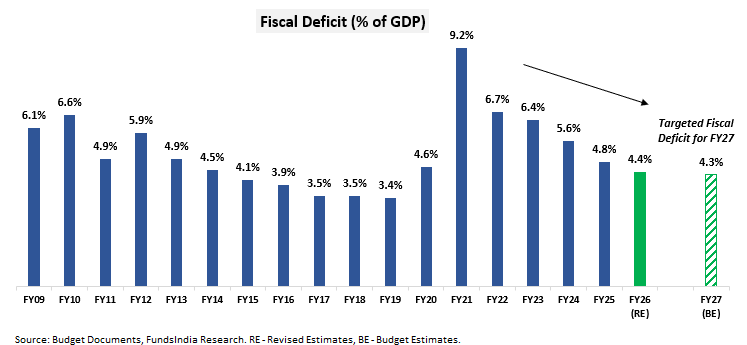

- Fiscal deficit target at 4.3% of GDP for FY 27 vs 4.4% for FY 26 – in line with the fiscal prudence path of debt consolidation.

- Debt to GDP ratio estimated at 55.6% for FY 27 vs 56.1% for FY 26 – in line with the central government target to bring down debt to 50% (+/- 1%) of GDP by 2030.

2. Capital Expenditure increased

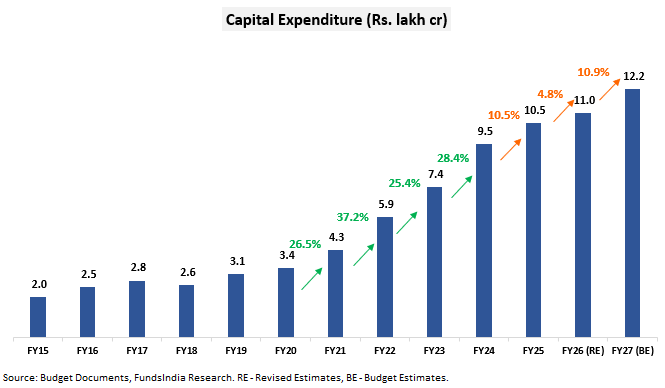

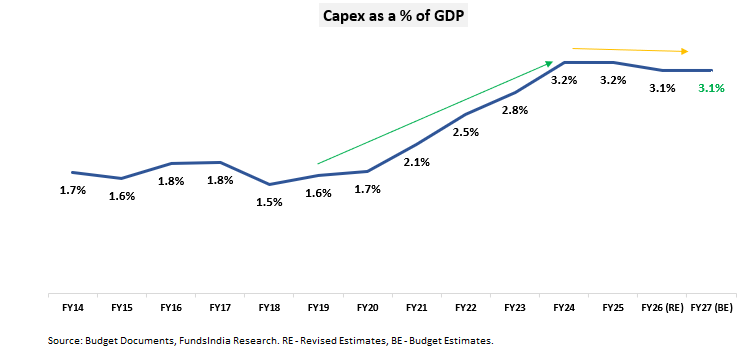

- FY27 Capex increased by ~11% to Rs 12.2 lakh cr (i.e 3.1% of GDP) vs Rs 11 lakh cr for FY 26.

3. In this Budget Government has undertaken comprehensive economic reforms towards creating employment, boosting productivity and accelerating growth.

- Manufacturing has been identified as a strategic priority, backed by new schemes to boost production, upgrade infrastructure, and provide targeted support to MSMEs.

- The services sector also receives renewed focus, with higher allocations for skilling initiatives, changes in safe harbour thresholds & margins, and plans to establish medical tourism hubs among other measures.

- Agriculture sees continued reform through increased investments in irrigation, productivity improvement, and technology adoption – measures aimed at raising rural incomes and strengthening allied sectors.

4. New Income Tax Act will come into effect from 1st April 2026 expected to improve ease of doing business, simplify taxation and streamline compliance

4. Securities Transaction Tax (STT) has been increased for Futures and Options

5. No Change in Personal Income Tax and Capital Gains Taxation for Investors

Budget in Visuals

Nominal GDP Projection for FY26 = INR 357 lakh crores (~8% growth over INR 331 lakh crores in FY25)

Nominal GDP Projection for FY27 = INR 393 lakh crores (~10% growth over INR 357 lakh crores in FY26)

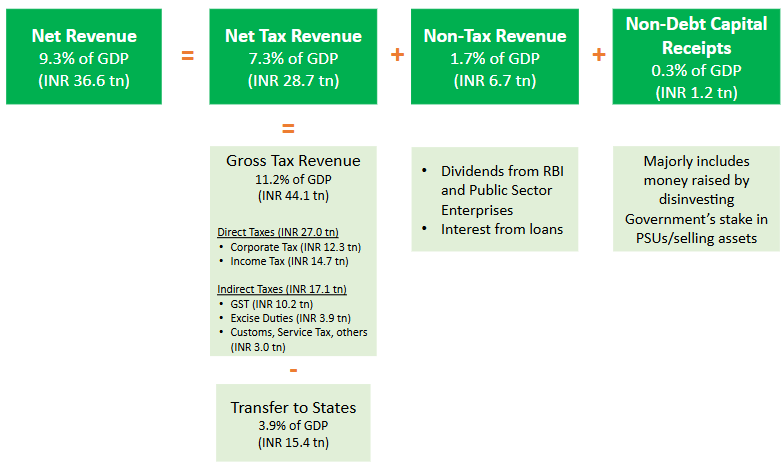

Where does the money come from?

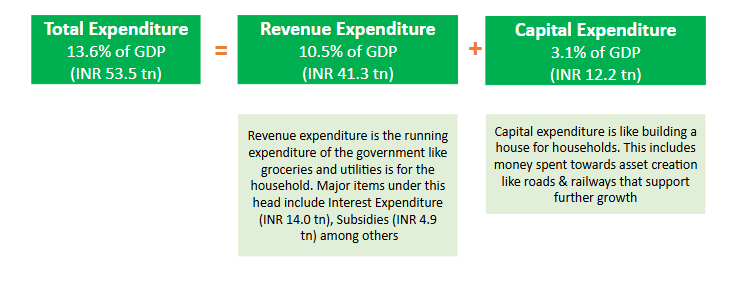

Where does the money get spent?

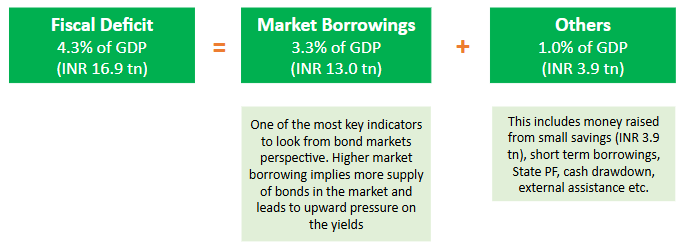

How much is the deficit between spending and earning?

How is the deficit financed?

Fiscal Consolidation On Track..

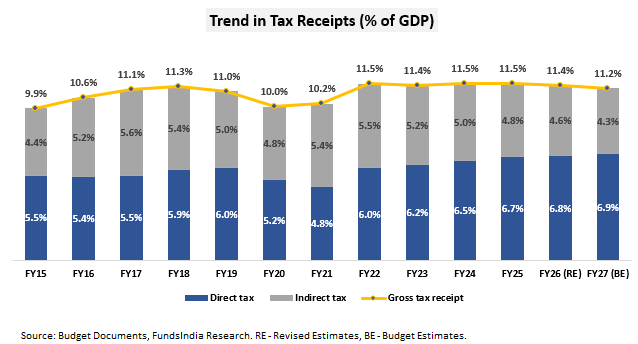

Tax Receipts as a % of GDP remains stable..

Capex increased but growth has moderated..

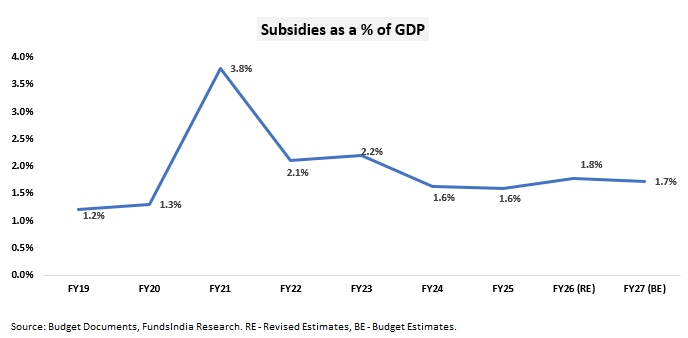

No dilution in quality of spending -> Subsidies remain low

What’s in it for you?

1. Securities Transaction Tax (STT) increased for Futures and Options Trading

STT on Futures has been increased from 0.02% to 0.05%, on option premium from 0.10% to 0.15% and on the exercise of options from 0.125% to 0.15%.

2. No Change in Personal & Capital Gains Taxation

3. What gets Cheap and Costly

- Cheap – Foreign travel, Certain Imported goods for personal use, Cancer treatment medicines, Mobile phones & tablets, EV batteries & solar panels.

- Costly – Luxury goods, Cigarettes & tobacco, Imported cameras & equipment.

Other Important Announcements

- Share Buyback taxation – Buyback to be taxed as Capital Gains instead of dividend income for all types of shareholders

- Changes in Tax Collected at Source limits – TCS has been reduced to 2% on foreign tour packages, for pursuing overseas education and medical purposes under the Liberalized Remittance Scheme (LRS).

- TDS compliance eased – TDS on the sale of immovable property by a non-resident to be deducted and deposited through resident buyer’s PAN instead of TAN thereby reducing the compliance burden.

- New Income Tax Act 2026 – The new act will come into effect from 1st April 2026 and is expected to simplify tax rules and compliances.

- Increase Investment Limits for Individual persons resident outside India (PROIs) – limit to be increased for investments made through the Portfolio Investment Scheme.

- Rationalizing tax disputes – several changes made for immunity from penalty and prosecution in cases of misreporting income, non-disclosure of non-immovable foreign assets below a certain value and settling tax disputes.

FundsIndia Equity View:

This budget has continued the focus on fiscal consolidation, increased the capital expenditure with focus on infrastructure (mainly road and railways) and introduced several changes for ease of doing business and tax compliance. The increase in government capital expenditure is expected to drive investment momentum along with private sector capex.

Overall, we maintain our POSITIVE outlook on Equities over a 5-7 year horizon, anticipating reasonable earnings growth in the coming years. We believe we are currently in the mid stage of a multi-year bull market. Our Equity view is derived based on our 3 signal framework driven by

- Earnings Cycle

- Valuation

- Sentiment

As per our current evaluation we are at MID PHASE OF EARNINGS CYCLE + NEUTRAL VALUATIONS + MIXED SENTIMENTS

- MID PHASE OF EARNINGS CYCLE

We expect a reasonable earnings growth environment over the next 3-5 years. This expectation is led by Manufacturing Revival, Banks – Better asset quality & pickup in loan growth, Revival in Real Estate, Early signs of Corporate Capex, Structural Demand for Tech services, Government’s focus on Consumption boost, Structural Domestic Consumption Story, Consolidation of Market Share for Market Leaders, Strong Corporate Balance Sheets (led by Deleveraging) and Govt Reforms (Lower corporate tax, Labour Reforms, PLI) etc. - NEUTRAL VALUATIONS

FundsIndia Valuemeter based on MCAP/GDP, Price to Earnings Ratio, Price To Book ratio and Bond Yield to Earnings Yield is at 56 (as on 31-Jan-2026) – valuation remains in the ‘Neutral’ Zone i.e not expensive or cheap. - BALANCED SENTIMENTS

Market sentiment is currently Balanced, not overly optimistic or pessimistic. Domestic investors (DIIs) continue to invest steadily. Over the past year, money coming from Indian investors has remained strong due to:

- A shift in savings from physical assets (like gold and real estate) to financial assets

- The growing habit of investing through monthly SIPs

- Equity investments by institutions like EPFO

FII Flows continue to remain weak. FII Flows have been muted for the last 3+ years -> since Oct-21 at negative Rs. ~1.4 lakh Crs vs DII Flows at Rs. ~17.9 lakh Crs. This is also reflected in the FII ownership of NSE Listed Universe which is currently at its 14 year low of 17.5% (peak ownership at ~22.1%). This indicates significant scope for recovery in FII inflows. IPOs Sentiments has slowly started to revive with many IPOs coming into the market. Despite recent volatility, market returns have been reasonable with the past 5Y Annual Return at 13.6% (Sensex TRI) lagging underlying earnings growth at 16.2% and nowhere close to what investors experienced in the 2003-07 bull market (45% CAGR). Overall the sentiments are Balanced and we see no signs of ‘Euphoria’.

FundsIndia Fixed Income View:

The Fiscal Deficit for FY27 at 4.3% of GDP adheres to the fiscal glide path. New Fiscal Consolidation roadmap to bring down debt to 50% (+/- 1%) of GDP by Mar-2030 from an estimated 56.1% by FY26 and 55.7% by FY27. Bond Markets will like the deficit number and medium term investors will appreciate the debt / GDP framework. However market borrowing is higher than expectation which could keep bond yields elevated – Net Market Borrowing in FY27 at INR 11.7 lakh crores (vs 11.3 lakh crores in FY26) and Gross Market Borrowing in FY27 at INR 17.2 lakh crores (vs 14.6 lakh crores in FY26).