Shriram Pistons & Rings Ltd – Innovating Mobility Solutions Sustainably

Founded in 1963 and based in New Delhi, Shriram Pistons & Rings Ltd. is a prominent manufacturer of automotive components, specializing in pistons, piston pins, piston rings, and engine valves. The company supplies to both domestic and international Original Equipment Manufacturers (OEMs) as well as the aftermarket segment. It holds the distinction of being the largest producer of pistons, rings, and engine valves in the country. Beyond the automotive sector, it also serves industries such as railways, gensets, industrial equipment, and defence. As of 30 June 2025, the company operates 9 manufacturing units and 5 assembly plants, exporting to over 45 countries across 5 continents.

Products and Services

The company’s core product portfolio comprises pistons and piston pins, piston rings, engine valves, electric motors and motor controllers, as well as precision injection-moulded components. It also offers a range of additional products, including cylinder liners, crankshafts, connecting rods, gaskets, and more.

Subsidiaries: As of FY25, the company has 4 subsidiaries and no other joint venture/associate company

Investment Rationale

- Performance of core business – The company’s core offering encompasses pistons, piston pins, piston rings, and engine valves tailored for the Internal Combustion Engine (ICE) segment. The company maintains a strong and resilient position in the ICE components market with longstanding relationship with major automotive players such as Maruti Suzuki, Hero MotoCorp, Bajaj Auto, Hyundai, Ashok Leyland, and more. The ICE business remains a strong cash generator, providing the financial backbone for the company’s diversification into emerging technologies and sectors. It has long-standing technical collaborations with industry leaders such as KS Kolbenschmidt (Germany) for pistons (since 1965), Riken Corporation (Japan) for rings (since 1977), Fuji Oozx (Japan) for valves (since 1990), and Honda Foundry (since 1993). Complementing these strategic moves, SPRL continues to innovate through its state-of-the-art Technology Centre, focusing on alternative fuel technologies such as CNG, LNG, hydrogen, ethanol blends, and hybrid systems, alongside EV components.

- Diversification strategies – The company has strategically diversified its business beyond the traditional ICE segment, positioning itself to tap into future mobility and multi-sector opportunities. The company has made targeted acquisitions to scale up capabilities in high-growth, future-focused areas. The acquisition of Karna Intertech Pvt. Ltd. has strengthened in-house die-casting mould capabilities, supporting the production of high-precision components and enhanced synergies within SPRL’s supply chain. Similarly, the acquisition of SPR-TGPEL Precision Engineering Ltd. has significantly expanded SPRL’s footprint in precision injection-moulded parts across automotive, electrical, consumer goods, and medical sectors – broadening its market reach and technical depth. SPRL also entered the EV component space through its acquisition of SPE EMFI in FY23, doubling revenue from the segment and investing in a new Coimbatore facility to manufacture electric motors and controllers, with production expected to commence by Q2/Q3 FY26.

- Q1FY26 – During the quarter, the company generated revenue of Rs.963 crore, an increase of 15% compared to the Rs.837 crore of Q1FY25. EBITDA improved by 16% YoY to Rs.223 crore. Net profit stood at Rs.135 crore as against the Rs.117 crore of Q1FY25, an increase of 15%.

- FY25 – The company generated revenue of Rs.3,550 crore, an increase of 15% compared to FY24 revenue. Operating profit is at Rs.836 crore, up by 15% YoY. The company posted net profit of Rs.516 crore, a jump of 18% YoY.

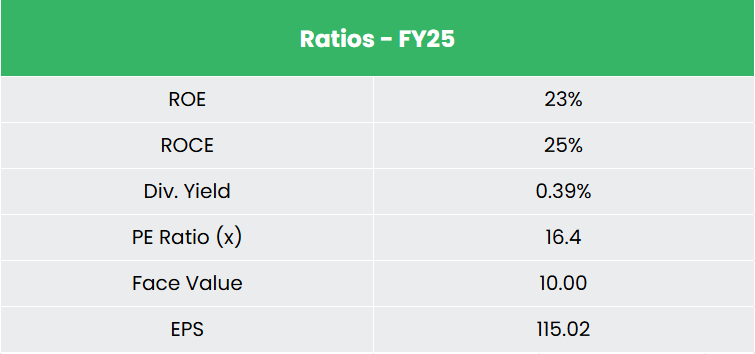

- Financial Performance – The company has generated revenue and net profit CAGR of 46% and 20% over the period of 3 years (FY23-25). Average 3-year ROE & ROCE is around 23% and 26% for FY23-25 period. The company has a robust capital structure with a debt-to-equity ratio of 0.21.

Industry

India’s auto component industry is experiencing strong momentum, driven by favourable demographics, rising incomes, and the restructuring of global supply chains. Government initiatives such as the PLI scheme, push for EV adoption, and focus on local manufacturing are further accelerating growth. As the world’s third-largest automotive market and a leader in 2W and 3W production, India is emerging as a global sourcing hub, supported by its strategic proximity to key international markets. Rising vehicle demand, especially in the two-wheeler segment, along with increased localization by global OEMs, is creating significant opportunities for domestic component manufacturers across both conventional and electric vehicle segments.

Growth Drivers

- 100% FDI is allowed under the automatic route for auto components sector.

- The reduction in the tax burden in the 2025-26 Union Budget is expected to boost spending among the expanding middle class population.

- Growing working population and expanding middle class.

Peer Analysis

Competitors: Sona BLW Precision Forgings Ltd, Bharat Forge Ltd, etc.

Compared to its listed peers, the company demonstrates steady revenue growth, superior return ratios, and strong earnings potential, reflecting its financial stability and ability to generate income and returns from invested capital efficiently.

Outlook

SPRL offers a compelling investment proposition rooted in its dual strength: steadfast leadership in the ICE components market and a multifaceted diversification strategy for future mobility. The management has given a guidance of 15% growth in the future years. SPRL’s ICE components segment remains a strong pillar – characterized by market leadership, consistent growth, margin resilience, and strong profitability. The segment’s financial robustness and operational integrity provide the strategic flexibility necessary to expand into emerging mobility technologies and diversify the company’s growth trajectory.

Valuation

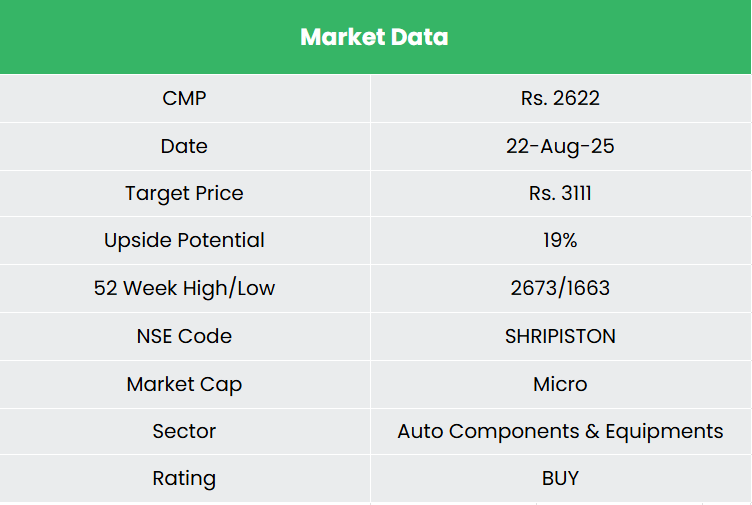

We believe the company is well positioned to sustain its growth momentum over the medium to long term, supported by robust expansion plans and strong brand recall among major OEMs. We recommend a BUY rating in the stock with the target price (TP) of Rs.3,111, 22x FY27E EPS.

Note: We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

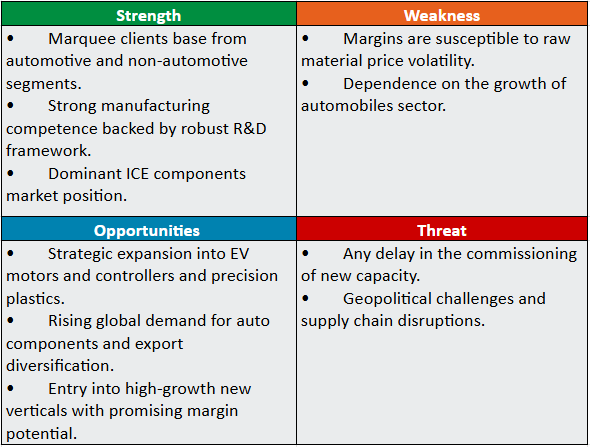

SWOT Analysis

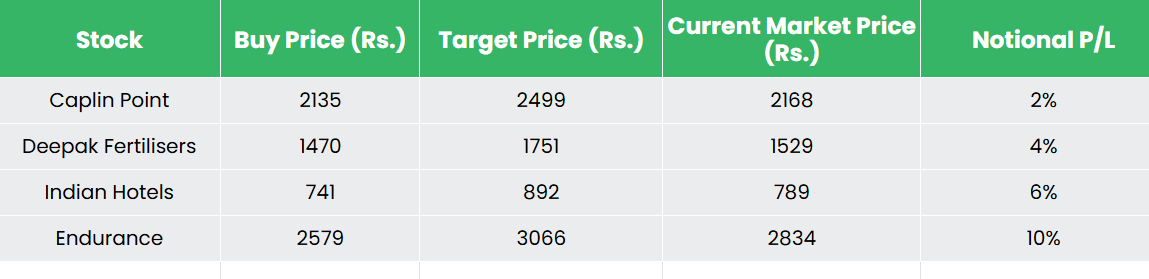

Recap of our previous recommendations (As on 22 August 2025)

Deepak Fertilisers & Petrochemicals Corp Ltd

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.