MF Monthly Dividend Plans are sometimes sold to investors on the pitch that they will offer almost 1% ‘return’ in the form of dividend payouts every month. That is, a ‘return’ of around 10-12% for the year.

Sounds attractive right?

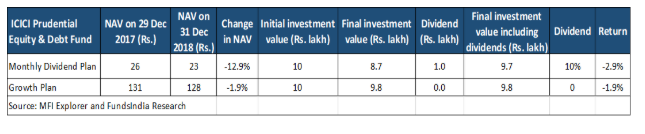

Let’s check what really happens, by taking the example of ICICI Prudential Equity & Debt Fund’s Monthly Dividend Plan.

For the year 2018, the scheme gave investors, dividend every month which added up to around 10% dividend for the entire year. That is, if you had invested Rs.10 lakh at the start of the year, you would have received around Rs.1 lakh by way of dividends by the end of it.

So, does that mean the scheme return was 10% in 2018?

Well, your answer would be a ‘yes’ if by the end of the period your original investment value had remained unchanged. That is, you end the year with the same Rs.10 lakh that you started with and also make an extra Rs.1 lakh.

That would seem like a good deal.

Hang on. Let’s now check what actually happened to the Rs.10 lakh that you invested on 29 Dec 2017.

You’ll find that your original investment value fell to Rs. 8.7 lakh by 31 Dec 2018.

Oops!

Assuming you simply put 10 lakhs in your locker, and took out some money every month adding to Rs 1 lakh over the year, still you should have ended up with Rs 9 lakhs right.

Since the remaining amount is Rs 8.7 lakhs, this simply means your fund value must have fallen (as is to be normally expected a lot of times in the short term for any equity-oriented product).

Your return, as calculated by the change in the NAV and as reflected in the fall in your investment value is therefore minus 2.9%. This also takes into account the dividends received.

See the table below.

Dividends don’t equal returns

What’s happening here?

The dividend that was pitched to you as ‘return’ is not the actual return but simply the amount extracted from the fund by selling off your investments (securities) worth around 1% of the corpus every month.

This happens irrespective of whether the fund has made a positive or negative return on the investments sold. This is certainly not in the best interest of investors.

The scheme NAV falls once dividends are paid. The NAV also falls if the market value of the securities held under the scheme falls. The decline on account of dividend payment is additional.

This becomes clear when we compare the change in NAV for the two schemes (table above). The sharper fall in the Dividend Plan NAV (-12.9%) compared to that in the Growth Plan NAV (-1.9%) reflects a large extent the impact of the dividend pay-out.

And hence, dividends (10%) do not equal returns (-2.9%)

Every dividend payment eats away into the scheme corpus. Assuming the number of outstanding units held by the fund remains the same, the smaller corpus then translates into a smaller NAV.

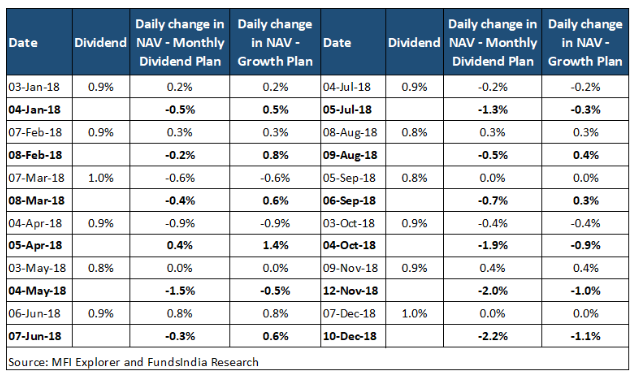

You can see the impact on the NAV on the next trading day (highlighted in bold) in the table below.

For instance, on 3 Jan, NAVs under both the plans increased by the same 0.2% compared to the previous day. It was, however, very different on 4 Jan, a day after dividends were paid. While the Growth Plan NAV rose by 0.5%, the Dividend Plan NAV fell by 0.5%.

Let’s pick one more day. On 5 April, while the Growth Plan NAV rose by 1.4%, the Dividend Plan NAV rose by only 0.4%.

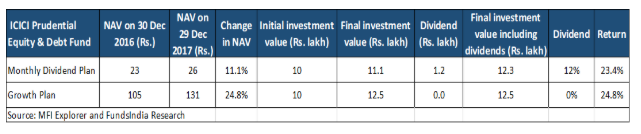

Monthly dividend plans gained popularity when NAVs were rising

As seen earlier, dividend payments come at the cost of a decline in your original investment value. This fall in investment value is fairly obvious during a down-market year when the scheme NAV is anyways falling irrespective of the dividend payments.

This may however not be so obvious in the up-market years when the NAV is rising. Then, even as dividends are paid, the NAV may still not fall as the market value of the scheme’s securities is going up.

And, dividend schemes have been marketed to investors during such times.

You can, however, see the impact of dividends on the Dividend Plan NAV by comparing it with the Growth Plan NAV.

See the table below.

While the returns under the Growth Plan benefit from a compounding impact too, the 24.8% rise in the NAV (instead of only 11.1%) also reflects the absence of the erosive effect of dividend payouts.

Our recommendation

We believe dividend-paying options don’t make sense in case of long-term investment products such as equity oriented mutual funds where the equity exposure is 60% or higher.

For such products, investors should opt for the growth option and reap the benefit of their money compounding over the long run.

Further, the Budget has abolished the dividend distribution tax (DDT) and instead made dividends taxable in the hands of investors at their applicable income tax slab rate. Currently, a fund distributes dividends after deducting a DDT of 11.648% on an equity scheme. Investors do not pay any tax on the dividends received.

From 1 April 2020, those in the 5% and 10% tax brackets (under the new tax regime) will face a lower dividend tax burden than before. For others, the dividend tax burden will be higher (15% to 30%).

Investors in the higher tax brackets have therefore, yet another reason to give dividend plans a miss.

If you require regular pay-outs, you can go for an SWP on a debt product (debt funds, fixed deposits). This will be efficient from a tax perspective too.