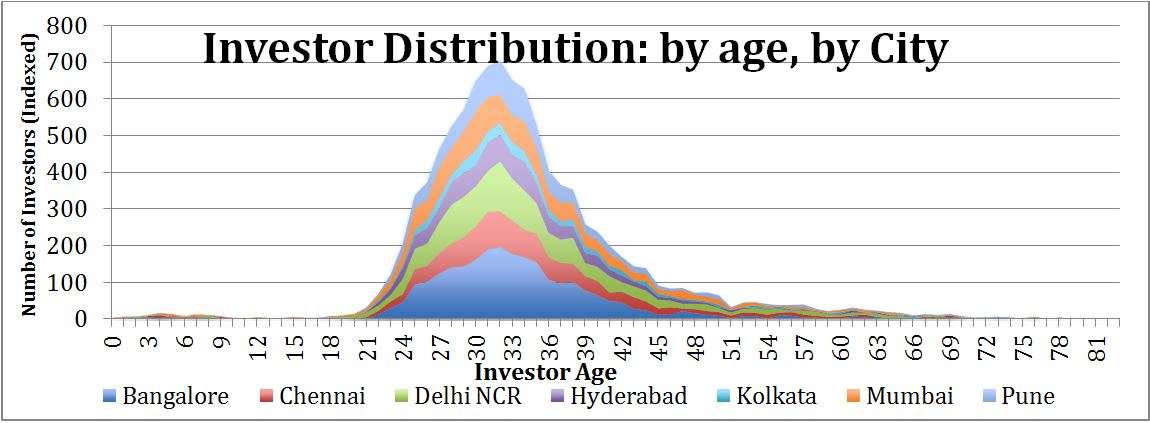

FundsIndia investor distribution, much like most things related to the Internet in India, is skewed towards young working age men. As a result our investors when measured across age for 6 of the biggest cities in India are distributed thus.

Our typical investor, as it can be seen, is between the ages 24 and 44. How does this age group compare with others in terms of investment behavior? Do older investors have differing investing patterns? Do their returns vary significantly? And how have they accumulated wealth?

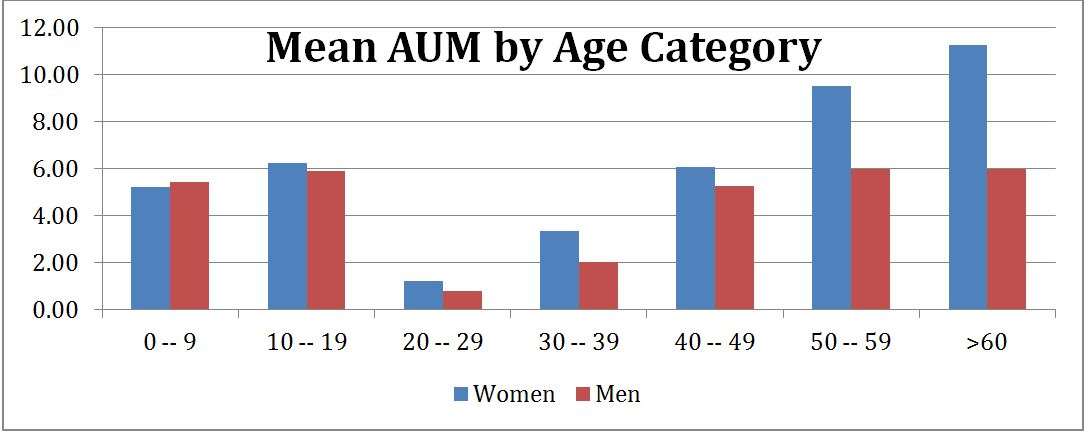

To start with, let’s divide our investor base into buckets of 10-year age intervals. How does their relative wealth compare? What’s our expectation though? Possibly, for someone who hasn’t looked at the data, it’s to expect a linearly increasing wealth with age. We expect the power compounding and time of accumulation to work thus, don’t we? Let’s now look at the data though,

[AUM has been indexed to a base and is representative]

[AUM has been indexed to a base and is representative]

Our general hypothesis that wealth increases with age seems to hold for adults. The age group of 20-29 seems to have the least wealth as they’ve only just started investing. It then progresses as a monotonically increasing function for that range across the older age groups. An interesting divergence is that older men seem to plateau in terms of their wealth while women continue to grow their wealth with age. Men seem to have higher redemptions with more advanced age. This can have several social reasons which we don’t want to get into now.

Another curious factor is that children and teens seem to have a mean wealth of a 40-year-old person in the overall investor population. The overall number of children as we saw previously, is very low. However, they seem to have a lot wealth. This simply point to a self selecting sample where only the more wealthy parents start investments for their children early.

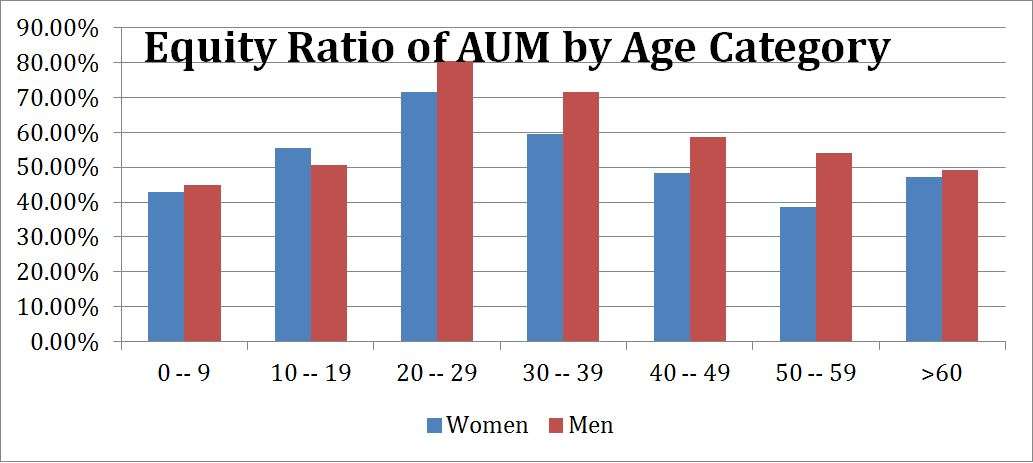

Another way of looking at investors is what portion of their overall investment is in equity funds. This gives us a good idea of whether investors understand risk and the power of compounding. We’d expect the youngest to be invested in equity the maximum; and we’d think that tapers off with age. The data again suggests that broadly but with interesting divergences.

Children whom we’d expect to be invested in equity almost entirely, seem to have a very low proportion of their wealth invested thus. Men seem to have more money in equities compared to women across all adult age groups. The slight bump in women’s equity participation in the last age bucket points again to social reasons we alluded to above.

An interesting on-going project will be to track how people who’re currently in their 20s and 30s rebalance their portfolios as they get older. Will they do it such that the overall spread remains as the current snapshot captures it? Or will they retain their behavior?