Buying a house means long-term commitment by way of EMI. The EMI amount is not small by any means, either. But that has never been a deterrent for most of us. We are willing to take a 15-year loan and pay our huge EMIs diligently, and ensure that we never miss a payment.

But this same discipline, this same giving of good sums, this same long-term horizon is not present when it comes to our mutual fund investments. Here, we hesitate to commit a fixed sum. We are under-invested, content to put in small sums of just Rs. 1,000 or Rs. 2,000 a month, even while we commit over ten times of this to our EMIs.

So, what if we compare a house investment with a mutual fund investment? If, instead of paying your EMI, you had been investing in mutual funds, what would you have ended up with?

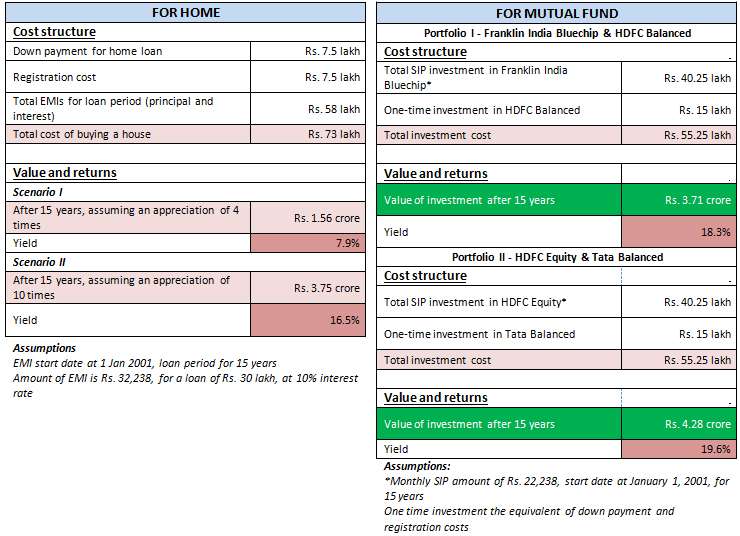

Costs of a house

Let us assume you planned to buy a house for Rs. 37.5 lakh. This is a reasonable price to assume for a middle class person to buy a house in the city. It also makes for easier calculations and presentations of down-payment and loan component.

Typically, banks ask you to put in 20 per cent of the cost as down-payment which comes from your own savings. For our house, this works out to Rs. 7.5 lakh, and the remaining Rs. 30 lakh is taken as a home loan. Assuming a reasonable interest rate of 10 per cent and a loan tenure of 15 years, the EMI for this loan works out to Rs. 32,238. Then, you have registration costs of the property, which is an average of 20 per cent, though individual states have different rates. Registration adds a further Rs. 7.5 lakh to the cost. The total of the loan payments over the 15-year period is actually Rs. 58 lakh. That brings the total cost of the house to a whopping Rs. 73 lakh (down-payment + loan + registration).

Now let’s see what happens if you commit this EMI amount to mutual funds through an SIP. You will have to pay rent as you don’t have a house. A rent of Rs. 10,000 a month is a fair assumption for a house of Rs. 37 lakh. So that gives you Rs. 22,238 to invest in a good equity fund with a long-term track record. We assume that the increase in your rent will be taken care of by salary hikes. This apart, there is also the Rs. 7.5 lakh each for the down-payment and registration cost, both of which came from your savings. Let’s say you put that into a balanced fund for proper asset allocation.

How the returns fare

Look at the table now. We have different scenarios on appreciation in property prices. We took data on mutual fund performance for the past fifteen years (assuming also that you bought the house 15 years ago).

Take the best-case scenario of your property growing 10 times in 15 years and compare it with Portfolio II. You will see that mutual funds still delivered Rs. 53 lakh more. However, the chances of a 10-fold jump in property over a 15-year period are low. In order to beat mutual funds, your house should have appreciated by at least 12 times. And if a 10 time appreciation is hard, a 12 time rise is even more remote.

So had you patiently allowed you money to grow over these 15 years, your mutual funds would have fetched you better returns.

Clearly, the SIP had delivered much higher, and that too with a lower investment amount every month (Rs. 10,000 lesser than your EMI as a result of rent).

So, what about this?

- One, if you showed the patience and ability to commit high sums for a long period of time, like you do with your EMI, you would be able to build a far superior corpus for your long-term goals.

- Two, you need not be in a hurry to take a loan and buy a house in your initial years of high saving.

Happy investing!

It’s a good analysis but I already took Home Loan and also investing sum of one thierd of my EMI in SIP.

Your intention is good but there is a basic flaw in ur assumption n argument. When u r comparing these two then u must consider that Rent over the years will grow atleast by inflation percentage i.e 6-7% and EMI will remain constant or will decrease in 15 years looking at interest rate scenario.

Basically ur left out money after paying rent will decrease over the years and this lower corpus at the end of 15 years.

Further, U have completely ignored the aspect of non monetary benefits n pleasure of owing a house.

Nontheless I completely agree with u that one should put in sizable amount in SIP simultaneously u must do proper asste allocation ….it can’t be either of!!

Priyesh, We have stated that standard rent hike in most lease agreements is 5% and we are stating that it will be taken care of by salary hikes.

We have averaged the interest rate at 10%. Since interest rate is a 7 year cycle of either upward or downward movement. Interest rates that were as high as 12% in 2001 is now available at 9%. Interest rates are not expected to be on a downward spiral all the time.

Yes you are right about the non monetary benefits of owning a house. Let us look at it in another angle – the fear and stigma of owning a housing loan is replaced with the pride of investment. Also in case of an emergency as well you can afford to stop your SIPs and further on you will have liquidity in 2 days, while that is not the same with owning a house that is purchased using a housing loan.

What abt the sleepless nights of losing to the extent of 50% of total corpus in few days when all ur money in just equity????

Lease agreement do have 5% clause but in long term u need to change ur leased house several tines n u have to bear the hike of almost 20% in 3-4 years.

When u paying emi then all ur salary hike can be used to repay ur loan faster n can thus save considerable amt of interest.A 20% hike in emi can repay ur loan 50% faster.

I would again say it can’t be either of …its alws better if u have both of the world equity n property

Priyesh, the whole point behind the article was to convey to people that SIP is a great tool to build wealth over a long period of time. And how you can get rewarded handsomely, if the patience that people display towards paying their EMIs, the same patience was displayed towards their SIPs as well.

If you notice the final yield on the SIP(18%-19%) that you see in the article is despite that the fact that the investments in SIPs have faced 2 big bear markets, 2001 (dot com bubble) and 2008 (housing bubble) when the markets have fallen between 30% and 50%. Agreed that the equity markets do not give linear returns, but this is proof enough that patience pays. Black swan events happen with all asset classes, not necessarily with equities alone.

Priyesh, while you migh be right about losing sleep over the collapse of equity market, but a collapse in housing market is even worse a fear. And house is an expenditure, not an investment better incurred without debt. Of course you won’t have the Joy of owning new house for 15 years, never the tension of EMI’s. Plenty of people in India are stuck with their bad job, bad boss, have to cancel their other plans, can’t take risks due to Home Loan EMI’s. So that mental relief shall also be priced.

Its good to see this comparison…One observation that comes to my mind is that,

Property price, interest rate, rent and registration cost is considered in todays value but then it is assumed that property was bought 15 years ago. I understand all the above values were available at lesser cost at that time (15 years back)

Comparison would be more realistic if all the historical values had been compared to mutual fund performance for same period.

Gangadhar, These values are still applicable as on 2001.That is one of the reason, why we have averaged the interest rate at 10%. Since interest rate is a 7 year cycle of either upward or downward movement. Interest rates that were as high as 12% in 2001 is now available at 9%. The interest rate even in a fixed interest housing loan is reset once in 2 years. Hence all of the values that have been taken “Property price, interest rate, rent and registration cost” are all applicable even as of 2001

It’s a good analysis but I already took Home Loan and also investing sum of one thierd of my EMI in SIP.

There is no doubt that long term systematic investment is the key to wealth creation. But, this is not the right analogy. may be true for those who invest pre dominantly in real estate.

Ramanathan, On the other hand, I think there is no better analogy than comparing SIP to EMI. Both are long-term commitments. IN the former, there is delayed gratification and in he latter, there is immediate gratification and you pay for it over the long term 🙂 It is true for those who invest even in one house in their early income/saving years and have little left to save.

EMI is negative compounding, while SIP is positive compounding…

Your intention is good but there is a basic flaw in ur assumption n argument. When u r comparing these two then u must consider that Rent over the years will grow atleast by inflation percentage i.e 6-7% and EMI will remain constant or will decrease in 15 years looking at interest rate scenario.

Basically ur left out money after paying rent will decrease over the years and this lower corpus at the end of 15 years.

Further, U have completely ignored the aspect of non monetary benefits n pleasure of owing a house.

Nontheless I completely agree with u that one should put in sizable amount in SIP simultaneously u must do proper asste allocation ….it can’t be either of!!

Priyesh, We have stated that standard rent hike in most lease agreements is 5% and we are stating that it will be taken care of by salary hikes.

We have averaged the interest rate at 10%. Since interest rate is a 7 year cycle of either upward or downward movement. Interest rates that were as high as 12% in 2001 is now available at 9%. Interest rates are not expected to be on a downward spiral all the time.

Yes you are right about the non monetary benefits of owning a house. Let us look at it in another angle – the fear and stigma of owning a housing loan is replaced with the pride of investment. Also in case of an emergency as well you can afford to stop your SIPs and further on you will have liquidity in 2 days, while that is not the same with owning a house that is purchased using a housing loan.

What abt the sleepless nights of losing to the extent of 50% of total corpus in few days when all ur money in just equity????

Lease agreement do have 5% clause but in long term u need to change ur leased house several tines n u have to bear the hike of almost 20% in 3-4 years.

When u paying emi then all ur salary hike can be used to repay ur loan faster n can thus save considerable amt of interest.A 20% hike in emi can repay ur loan 50% faster.

I would again say it can’t be either of …its alws better if u have both of the world equity n property

Priyesh, the whole point behind the article was to convey to people that SIP is a great tool to build wealth over a long period of time. And how you can get rewarded handsomely, if the patience that people display towards paying their EMIs, the same patience was displayed towards their SIPs as well.

If you notice the final yield on the SIP(18%-19%) that you see in the article is despite that the fact that the investments in SIPs have faced 2 big bear markets, 2001 (dot com bubble) and 2008 (housing bubble) when the markets have fallen between 30% and 50%. Agreed that the equity markets do not give linear returns, but this is proof enough that patience pays. Black swan events happen with all asset classes, not necessarily with equities alone.

Priyesh, while you migh be right about losing sleep over the collapse of equity market, but a collapse in housing market is even worse a fear. And house is an expenditure, not an investment better incurred without debt. Of course you won’t have the Joy of owning new house for 15 years, never the tension of EMI’s. Plenty of people in India are stuck with their bad job, bad boss, have to cancel their other plans, can’t take risks due to Home Loan EMI’s. So that mental relief shall also be priced.

I fully agree with this.

Paying the same amount in SIP will certainly fetch more returns as compared to paying the same amount as EMI.

Most people in India dont understand the SIP route and therefore they end up missing on the benefits of investing in SIP

Its good to see this comparison…One observation that comes to my mind is that,

Property price, interest rate, rent and registration cost is considered in todays value but then it is assumed that property was bought 15 years ago. I understand all the above values were available at lesser cost at that time (15 years back)

Comparison would be more realistic if all the historical values had been compared to mutual fund performance for same period.

Gangadhar, These values are still applicable as on 2001.That is one of the reason, why we have averaged the interest rate at 10%. Since interest rate is a 7 year cycle of either upward or downward movement. Interest rates that were as high as 12% in 2001 is now available at 9%. The interest rate even in a fixed interest housing loan is reset once in 2 years. Hence all of the values that have been taken “Property price, interest rate, rent and registration cost” are all applicable even as of 2001

Great post. I am loving it !!!

Much awaited article…thanks FundsIndia

Very Nice

In SIP market risk is there, there is no guarantee of returns and it is purely based on market growth, if we purchas land or building home that will be permanent asset and growth will be sure, then how SIP is better than making home.

Hello Sir, if you see the National Housing Bank’s (subsidiary of RBI) index for property called Residex, it shows that property market does indeed fall. No guarantee of growth. Between 2007 and 2015 for instance, Mumbai market grew just 11% annually, Delhi, even worse at 8%. HYderabad – -0.38% annually – that is it fell.

Also in 15-20 years, while property will grow, equity too has 0% chance of falling and mutual funds have proved to beat all other asset classes. If you talk of 3 years in equity market, then a 3-year in property market too would have given you flat returns in many cities. Just that most people are not aware of property price movement (as there is little information) and are all aware of day-to-day market returns. I think this perception that property delivers more is a myth, arising from lack of sufficient info and nothing else. thanks, Vidya

Hello Sir, without sounding to be abrupt here, i would say this is a common misconception among people in India and rest of the world. The idea that property prices can never fall is one of the reason why the US Economy Collapsed in 2008. While ours is little different, but the way world is interlinked, India is forming a property bubble with unsold real estate inventory in all major cities. If we realistically go with Supply vs. Demand idea, the property prices should have fallen steeply, but they have not, there is minor drop. Reason? Reason is hoarding, builders are not willing to sell on lesser prices but they’re happy to hold it back. But this cannot be done for a long time.

Another difference between real estate market and stock market is that stock markets have shorters. There are a set of people who think the orices for an equity have gone way higher than where it should be and they bet against it, correcting the prices. But there are no such shorters in the Real Estate market, the prices can go over the roof and continue soaring, and when it falls, it will come spinning down.

Last aspect is liquidity. You have a 3BHK flat worth 50 Lacs, you need 10 Lacs for some emergency, you can’t sell of 1 bedroom and keep other 2. Even selling off the whole flat is a painful affair, and don’t forget the long term capital gain tax that you’ll have to pay. Whereas in case of equities, well tax free in long term and you have your money in 2 days, and don’t need to hustle around looking for buyers.

The issue with Indian mentality is that we feel proud to own a house rather having good portfolio. That one of the reason we usually go for high EMI rather then investing more in SIP

not Real Estate fan & believes that one should not own more than one house.

but I guess you should have made realistic assumptions for EMI.

In 2001, cost of 2BHK in my city (Pune) was around : 6 Lakh.

In 2001, For 6 lakhs loan My EMI with 11% should be around : 6800. for 15 years.

today cost of this 2 bhk is: 70 lakh.

As it is now old, so consider discounted price as : 60 Lakh.

So with monthly payment of Rs.6800 and current value of Rs. 60 Lakh my returns comes around 19%…here I save my rent as well.

But we should agree that there is need of realistic expectations from real estate or equity as well in future.

Thank you.

Hi Paresh,. the emphasis here is towards returns and building wealth over a period of time using SIP and how the same can be used to buy a house. The value of the house and the EMI amount can all be adjusted accordingly based on an individual capacity and capability. A house was still available in 2001 for Rs 37 lakhs. So these are not unrealistic assumptions.

This article is extremely path breaking and eye opening though we need not take it implicitly.

Calculations are well done with rigor. This leads me to believe, being Indian, a hybrid approach will

be the best bet. That is, buying a Home plus doing SIP simultaneously getting the best of both Worlds,

of course choosing property builders and location with great care and thought.

Most definitely the edge with SIP is that nowadays we have a lot of study on Mutual Funds and we

easily can pick the best yielding ones.

Can’t thank enough for this wonderful article very timely, though I wish it came years ago.

Very Nice

U hv ignored I.Tax Benefits in both d cases.

The comparison is inproper without d Tax Benefit.

Secondly I can rent this house n earn rent income,which is an add-on income to my Kitti.

Nitin, A very valid point, but the tax saving that you gain because of both the principle repayment and interest payment is a very minuscule part considering the scale of the numbers(We would be putting the supporting working for this shortly). Also one can do an SIP in an ELSS fund, which would more or less work out to give the same level of tax benefits as that of paying your EMI.

Our main objective behind this article is to convey to people that there is an also an alternate way of buying a home or building wealth . And here our assumption is that the house bought is self occupied.

Couple of points:

1) FundsIndia does not sell property or provide broking. But does sell MF. Isn’t there a built in bias?

2) No amount of bank balance can match the happiness that a nice-comfortable reasonably priced home can provide. A home we can modify or enhance at will without seeking permission from landlord. A property that when we pass on to our heirs will make them rich (20-25 years later, in their prime youth)

3) I think it is wrong advice to discourage buying first and only home and encourage people to live in rented premises. I think lenders view home-owners favourably and life-long renters not so favourably (atleast outside India, eg: US)

4) Whereas “investing” in second property? Buying a property (to live) that is beyond our budget? Your advice could apply and does make sense 100%

Anand,The point of this analysis though was to tell how one can build wealth using SIP to create an asset base. To prove that SIP is one of the most superior route to creating wealth, it had to be compared to something which people use in a similar manner but to make EMIs (payments) and hence the comparison to housing. We have given another means of buying a home be it the first or be it the 10th. We totally agree on your second point, but let us look at it from another angle as well – maintaining the house it your responsibility, paying property taxes and various taxes associated with it is all a hassle.

My point is Anand, all asset classes come with their pros and cons and we can go on discussing countless points in favor and against each of them and each will have his or her own perspective to it.

As I said, by this analysis we are merely trying to give an alternative to approach to buying a home or build wealth over a period of time.

What all risks are involved in investing in mutual funds??

Hi Nupur,

Various categories of mutual funds carry different types of risks. Volatility is the major risk with respect to equity funds while debt carry credit risk and interest rate risk. But the biggest risk with respect to investing in mutual funds is the risk of capital loss. Having said that, mutual funds are the best investment avenues to generate real returns over a long period of time. And this can be done by having an asset allocated approach to investing with the help of your advisor.

@Lakshmeenarasimhan S

brilliant piece of information.

many experts consider 12 per return you considered yield of 19 per. is that possible if my horizon is 20 years.

is there a blog post on when to buy a house or measures to check or what cost checks to be done.

thanks

Rajni, that would depend on host of factors. But given the growth outlook for our economy, its is not impractical.

Good and encouraging maths, but where is the house I wanted at the end of the 15 yr term? Now what I would want to buy within my reach will be in the outskirts of the city. And do not forget the hassles of changing the house and dealing with the landlords, brokers etc etc. Last but not the least…..suppose one dies, then…..

Manish, please read this part of the article “Take the best-case scenario of your property growing 10 times in 15 years and compare it with Portfolio II. You will see that mutual funds still delivered Rs. 53 lakh more. However, the chances of a 10-fold jump in property over a 15-year period are low. In order to beat mutual funds, your house should have appreciated by at least 12 times. And if a 10 time appreciation is hard, a 12 time rise is even more remote” The whole point that we are trying to make is the kind of wealth you can build using SIP and how there is an actual possibility of that growing by 10 times in 15 years time provided you display the same level of patience.

Let us look at it form another angle.. Owning a house still comes with the hassle of maintaining it, paying property tax and various taxes associated with it. And yes suppose one dies then ….you need to have insurance.. either with the insurance amount that is equal to or greater than that of your loan, it can be used to prepay the loan

Now incase of SIP.. the wealth built can be liquidated in t+2 days time with a simple redemption request and this along with the insurance amount can be use to purchase a house.

Two questions

1. is doing SIP in shares a good idea

2. If I want to spread my saving to commodity – can I choose to buy silver every month or some other better mechanism of investing in silver with a horizon of 5 – 10 years.

There is a big difference with respect to SIP in a stock and a mutual fund. Firstly you need to know the company very well. One can average a stock, but if the price of the stock is falling because of fundamental reasons, there is no point in holding the stock, leave alone averaging. But with respect to a mutual fund, it is a basket of stocks which is picked after a lot of research and the fund manager is well equipped to take decision on a stock, whether to average it or to exit it completely. Hence it would generally be better option to do SIP in a mutual fund compared to a stock

No comments on commodities Rajni.

While I try to be optimistic about SIP returns, posts like this will make me think twice. What is you folks take on this?

http://capitalmind.in/2016/04/six-years-of-nothingness-the-nifty-or-gold-adjusted-for-inflation-have-been-lousy-investments/

Hello Pradeep,

Thanks for sharing this link. Unfortunately, while this is all analysed data, it is still point to point and it is the index not fund. So here’s my personal view on the article:

First on inflation: The inflation base changed at least 3 times (2001 under old CPI base, 2010 and then 2012 under new CPI) and the methodology once in 2010 (major change). So I wonder what he took unless he took the capital gains inflation index which grew 8.5% annually in 6 years. If so, yes between 2010 (which was any way a high year whether inflation adjusted or not..hence it becomes a case of taking a high point to see the returns; basically timing the market in a high) and now I think Nifty delivered only 6.5% point to point. But point to point is the whole problem, is it not? It means timing the market.

The fact is:

Nifty’s significant underperformance in this period was due to 2 reasons: it is commodity heavy and took a deep hit. It is bank heavy and took a more recent hit. But as a mutual fund investor you are not really investing in the Nifty.

I ran a check for funds in these 6 years. With point to point returns, if you had chosen equity funds (other than sector), the average returns is about 10.1%, about 1.5 percentage points higher than inflation. If you take funds with 3 rating and above it is 11.5%. And with 4&% ratings 13.6% annually.

With SIPs it was far better. Over these 6 years, even a middle order fund in the point to point list delivered 15-16% IRR. Hence as you will see, it is all about interpreting the right data. While the article’s point to point return data is right, it does not tell the full picture about how other products like MFs delivered. And the fact remains mutual funds and investments through SIPs (to be specific) performed well.

thanks,

Vidya

While I try to be optimistic about SIP returns, posts like this will make me think twice. What is you folks take on this?

http://capitalmind.in/2016/04/six-years-of-nothingness-the-nifty-or-gold-adjusted-for-inflation-have-been-lousy-investments/

Hello Pradeep,

Thanks for sharing this link. Unfortunately, while this is all analysed data, it is still point to point and it is the index not fund. So here’s my personal view on the article:

First on inflation: The inflation base changed at least 3 times (2001 under old CPI base, 2010 and then 2012 under new CPI) and the methodology once in 2010 (major change). So I wonder what he took unless he took the capital gains inflation index which grew 8.5% annually in 6 years. If so, yes between 2010 (which was any way a high year whether inflation adjusted or not..hence it becomes a case of taking a high point to see the returns; basically timing the market in a high) and now I think Nifty delivered only 6.5% point to point. But point to point is the whole problem, is it not? It means timing the market.

The fact is:

Nifty’s significant underperformance in this period was due to 2 reasons: it is commodity heavy and took a deep hit. It is bank heavy and took a more recent hit. But as a mutual fund investor you are not really investing in the Nifty.

I ran a check for funds in these 6 years. With point to point returns, if you had chosen equity funds (other than sector), the average returns is about 10.1%, about 1.5 percentage points higher than inflation. If you take funds with 3 rating and above it is 11.5%. And with 4&% ratings 13.6% annually.

With SIPs it was far better. Over these 6 years, even a middle order fund in the point to point list delivered 15-16% IRR. Hence as you will see, it is all about interpreting the right data. While the article’s point to point return data is right, it does not tell the full picture about how other products like MFs delivered. And the fact remains mutual funds and investments through SIPs (to be specific) performed well.

thanks,

Vidya

Very Nice

Why there is no mention of rental income on home?

Amar, the assumption here is, the house being bought is for personal stay rather than renting it out. The purpose of this article was mainly to emphasise how patiently investing in SIP in good funds will help build a good asset base.

Good article. Every investment has to be invested with purpose.

Everyone needs a home for good living, because no one cannot live or search for a rental home after 55 years of age.

We can choose mutual fund investments for our goals such as retirement corpus money, child college education fees, child marriage expenses which will require investment for a period of 15 years.

If I’m buying a house as an investment and not for residence, how would that compare to investment in SIP if the following two things are also considered:

1) Income tax rebate on the interest paid on housing loan (given that the housing loan interest is around 10% and the income tax is between 20% and 30%)

2) Rental income from the house

Srinivas,

The main objective of the article was to highlight the importance of SIP and how to use it to build wealth consistently and patiently over a long term.

Even if you buy a house for investment purposes you can notice it from the article while the probability of your money growing by 10 times is greater with equities compared to real estate over a 15 year period.

One of the reason we did not consider tax is because it becomes a very minuscule aspect considering the magnitude of the numbers.

What about IT exemption on Interest for salaried

Past evidence that we have worked on suggests that the returns will adequately compensate for the exemption in tax we get from paying the interest. It is also to be notes that the exemption in tax we get from the interest we pay would actually be a minuscule part in the whole scheme of things.Also the interest that you pay on your EMI reduces as you advance in the tenure of your loan and subsequently the tax advantage you get keeps reducing. Further more, assuming that the property is let out for rent, once the rent received is greater than the interest paid, you will have to pay capital gains tax for the amount over and above the interest paid.

Superb analysis Team Funds India.

Way to go Mr Srikanth and team. The only reason one may still feel tempted to invest in Real estate is to feed ones emotional self. Practically speaking SIPs best every asset class in the long run. Plus post 15yrs one can still buy a similar house.. Which will be debt free, brand new.. And have surplus money to take care of the monthly outflows.

Superb analysis Team Funds India.

Way to go Mr Srikanth and team. The only reason one may still feel tempted to invest in Real estate is to feed ones emotional self. Practically speaking SIPs best every asset class in the long run. Plus post 15yrs one can still buy a similar house.. Which will be debt free, brand new.. And have surplus money to take care of the monthly outflows.

Thanks for the analysis….

May I please know….. if I prepay 1 Lakh loan I save 3.78 L of interest payment and taking 14 yrs to repay full loan. If I invest 1L in MF and wait for 14 yrs will I get return of 3.78L (1L principal and 3.78L return) post tax deduction ???? I assume i do not want to switch or churn my MF portfolio but simply wait n watch for 14 yrs.

Considering 10% inflation, no tax cut on prepayment but tax cut on MF return…. no rent payment as i have purchase house for self and no plans of selling it off even if there s appreciation in housing rates

Hi Apoorva,

Going by your calculations, it translates into 11.9% annualised return which when we look at, the mutual funds have scored over very easily. The average performance of large-cap funds over the last 14 years(as of 30 Jun 2017) is 19% annualised. For this return the Rs one lakh will have become Rs 11 lakhs(If you had invested in a top performing large-cap fund, this amount will be even greater). The same Rs 1 lakh would have become Rs 22 lakh had it been invested in mid-caps. Average performance of mid-cap funds between 30 Jun 2003 and 30 Jun 2017 is 24% annualised. And all this is post tax since for equity funds, the long-term capital gains (units of an equity fund held for greater than a year) is zero. And yes this is taking into consideration a buy and hold approach.

Buying House is always a emotional decision.Still SIP are much more return than the home loan.In my view salary hikes are there to meet the monthly emi.for first couple of years its difficult to meet the need.But for long run own house has eyewitnesses different set of things like child growth,marriages etc,there is no fear of home changing.

like SIP if in metros home rates growing upto 13-15% ,so we can also get return after 15 years like balanced MF .So one can put some EMI in home loan and some money towards SIP

I fully agree with this.

Paying the same amount in SIP will certainly fetch more returns as compared to paying the same amount as EMI.

Most people in India dont understand the SIP route and therefore they end up missing on the benefits of investing in SIP

There is no doubt that long term systematic investment is the key to wealth creation. But, this is not the right analogy. may be true for those who invest pre dominantly in real estate.

Ramanathan, On the other hand, I think there is no better analogy than comparing SIP to EMI. Both are long-term commitments. IN the former, there is delayed gratification and in he latter, there is immediate gratification and you pay for it over the long term 🙂 It is true for those who invest even in one house in their early income/saving years and have little left to save.

EMI is negative compounding, while SIP is positive compounding…

Very Nice

Great post. I am loving it !!!

Very Nice

not Real Estate fan & believes that one should not own more than one house.

but I guess you should have made realistic assumptions for EMI.

In 2001, cost of 2BHK in my city (Pune) was around : 6 Lakh.

In 2001, For 6 lakhs loan My EMI with 11% should be around : 6800. for 15 years.

today cost of this 2 bhk is: 70 lakh.

As it is now old, so consider discounted price as : 60 Lakh.

So with monthly payment of Rs.6800 and current value of Rs. 60 Lakh my returns comes around 19%…here I save my rent as well.

But we should agree that there is need of realistic expectations from real estate or equity as well in future.

Thank you.

Hi Paresh,. the emphasis here is towards returns and building wealth over a period of time using SIP and how the same can be used to buy a house. The value of the house and the EMI amount can all be adjusted accordingly based on an individual capacity and capability. A house was still available in 2001 for Rs 37 lakhs. So these are not unrealistic assumptions.

Couple of points:

1) FundsIndia does not sell property or provide broking. But does sell MF. Isn’t there a built in bias?

2) No amount of bank balance can match the happiness that a nice-comfortable reasonably priced home can provide. A home we can modify or enhance at will without seeking permission from landlord. A property that when we pass on to our heirs will make them rich (20-25 years later, in their prime youth)

3) I think it is wrong advice to discourage buying first and only home and encourage people to live in rented premises. I think lenders view home-owners favourably and life-long renters not so favourably (atleast outside India, eg: US)

4) Whereas “investing” in second property? Buying a property (to live) that is beyond our budget? Your advice could apply and does make sense 100%

Anand,The point of this analysis though was to tell how one can build wealth using SIP to create an asset base. To prove that SIP is one of the most superior route to creating wealth, it had to be compared to something which people use in a similar manner but to make EMIs (payments) and hence the comparison to housing. We have given another means of buying a home be it the first or be it the 10th. We totally agree on your second point, but let us look at it from another angle as well – maintaining the house it your responsibility, paying property taxes and various taxes associated with it is all a hassle.

My point is Anand, all asset classes come with their pros and cons and we can go on discussing countless points in favor and against each of them and each will have his or her own perspective to it.

As I said, by this analysis we are merely trying to give an alternative to approach to buying a home or build wealth over a period of time.

What all risks are involved in investing in mutual funds??

Hi Nupur,

Various categories of mutual funds carry different types of risks. Volatility is the major risk with respect to equity funds while debt carry credit risk and interest rate risk. But the biggest risk with respect to investing in mutual funds is the risk of capital loss. Having said that, mutual funds are the best investment avenues to generate real returns over a long period of time. And this can be done by having an asset allocated approach to investing with the help of your advisor.

In SIP market risk is there, there is no guarantee of returns and it is purely based on market growth, if we purchas land or building home that will be permanent asset and growth will be sure, then how SIP is better than making home.

Hello Sir, without sounding to be abrupt here, i would say this is a common misconception among people in India and rest of the world. The idea that property prices can never fall is one of the reason why the US Economy Collapsed in 2008. While ours is little different, but the way world is interlinked, India is forming a property bubble with unsold real estate inventory in all major cities. If we realistically go with Supply vs. Demand idea, the property prices should have fallen steeply, but they have not, there is minor drop. Reason? Reason is hoarding, builders are not willing to sell on lesser prices but they’re happy to hold it back. But this cannot be done for a long time.

Another difference between real estate market and stock market is that stock markets have shorters. There are a set of people who think the orices for an equity have gone way higher than where it should be and they bet against it, correcting the prices. But there are no such shorters in the Real Estate market, the prices can go over the roof and continue soaring, and when it falls, it will come spinning down.

Last aspect is liquidity. You have a 3BHK flat worth 50 Lacs, you need 10 Lacs for some emergency, you can’t sell of 1 bedroom and keep other 2. Even selling off the whole flat is a painful affair, and don’t forget the long term capital gain tax that you’ll have to pay. Whereas in case of equities, well tax free in long term and you have your money in 2 days, and don’t need to hustle around looking for buyers.

Hello Sir, if you see the National Housing Bank’s (subsidiary of RBI) index for property called Residex, it shows that property market does indeed fall. No guarantee of growth. Between 2007 and 2015 for instance, Mumbai market grew just 11% annually, Delhi, even worse at 8%. HYderabad – -0.38% annually – that is it fell.

Also in 15-20 years, while property will grow, equity too has 0% chance of falling and mutual funds have proved to beat all other asset classes. If you talk of 3 years in equity market, then a 3-year in property market too would have given you flat returns in many cities. Just that most people are not aware of property price movement (as there is little information) and are all aware of day-to-day market returns. I think this perception that property delivers more is a myth, arising from lack of sufficient info and nothing else. thanks, Vidya

This article is extremely path breaking and eye opening though we need not take it implicitly.

Calculations are well done with rigor. This leads me to believe, being Indian, a hybrid approach will

be the best bet. That is, buying a Home plus doing SIP simultaneously getting the best of both Worlds,

of course choosing property builders and location with great care and thought.

Most definitely the edge with SIP is that nowadays we have a lot of study on Mutual Funds and we

easily can pick the best yielding ones.

Can’t thank enough for this wonderful article very timely, though I wish it came years ago.

The issue with Indian mentality is that we feel proud to own a house rather having good portfolio. That one of the reason we usually go for high EMI rather then investing more in SIP

U hv ignored I.Tax Benefits in both d cases.

The comparison is inproper without d Tax Benefit.

Secondly I can rent this house n earn rent income,which is an add-on income to my Kitti.

Nitin, A very valid point, but the tax saving that you gain because of both the principle repayment and interest payment is a very minuscule part considering the scale of the numbers(We would be putting the supporting working for this shortly). Also one can do an SIP in an ELSS fund, which would more or less work out to give the same level of tax benefits as that of paying your EMI.

Our main objective behind this article is to convey to people that there is an also an alternate way of buying a home or building wealth . And here our assumption is that the house bought is self occupied.

@Lakshmeenarasimhan S

brilliant piece of information.

many experts consider 12 per return you considered yield of 19 per. is that possible if my horizon is 20 years.

is there a blog post on when to buy a house or measures to check or what cost checks to be done.

thanks

Rajni, that would depend on host of factors. But given the growth outlook for our economy, its is not impractical.

Good and encouraging maths, but where is the house I wanted at the end of the 15 yr term? Now what I would want to buy within my reach will be in the outskirts of the city. And do not forget the hassles of changing the house and dealing with the landlords, brokers etc etc. Last but not the least…..suppose one dies, then…..

Manish, please read this part of the article “Take the best-case scenario of your property growing 10 times in 15 years and compare it with Portfolio II. You will see that mutual funds still delivered Rs. 53 lakh more. However, the chances of a 10-fold jump in property over a 15-year period are low. In order to beat mutual funds, your house should have appreciated by at least 12 times. And if a 10 time appreciation is hard, a 12 time rise is even more remote” The whole point that we are trying to make is the kind of wealth you can build using SIP and how there is an actual possibility of that growing by 10 times in 15 years time provided you display the same level of patience.

Let us look at it form another angle.. Owning a house still comes with the hassle of maintaining it, paying property tax and various taxes associated with it. And yes suppose one dies then ….you need to have insurance.. either with the insurance amount that is equal to or greater than that of your loan, it can be used to prepay the loan

Now incase of SIP.. the wealth built can be liquidated in t+2 days time with a simple redemption request and this along with the insurance amount can be use to purchase a house.

Two questions

1. is doing SIP in shares a good idea

2. If I want to spread my saving to commodity – can I choose to buy silver every month or some other better mechanism of investing in silver with a horizon of 5 – 10 years.

There is a big difference with respect to SIP in a stock and a mutual fund. Firstly you need to know the company very well. One can average a stock, but if the price of the stock is falling because of fundamental reasons, there is no point in holding the stock, leave alone averaging. But with respect to a mutual fund, it is a basket of stocks which is picked after a lot of research and the fund manager is well equipped to take decision on a stock, whether to average it or to exit it completely. Hence it would generally be better option to do SIP in a mutual fund compared to a stock

No comments on commodities Rajni.

Much awaited article…thanks FundsIndia

Good article. Every investment has to be invested with purpose.

Everyone needs a home for good living, because no one cannot live or search for a rental home after 55 years of age.

We can choose mutual fund investments for our goals such as retirement corpus money, child college education fees, child marriage expenses which will require investment for a period of 15 years.

Very Nice

Why there is no mention of rental income on home?

Amar, the assumption here is, the house being bought is for personal stay rather than renting it out. The purpose of this article was mainly to emphasise how patiently investing in SIP in good funds will help build a good asset base.

If I’m buying a house as an investment and not for residence, how would that compare to investment in SIP if the following two things are also considered:

1) Income tax rebate on the interest paid on housing loan (given that the housing loan interest is around 10% and the income tax is between 20% and 30%)

2) Rental income from the house

Srinivas,

The main objective of the article was to highlight the importance of SIP and how to use it to build wealth consistently and patiently over a long term.

Even if you buy a house for investment purposes you can notice it from the article while the probability of your money growing by 10 times is greater with equities compared to real estate over a 15 year period.

One of the reason we did not consider tax is because it becomes a very minuscule aspect considering the magnitude of the numbers.

Buying House is always a emotional decision.Still SIP are much more return than the home loan.In my view salary hikes are there to meet the monthly emi.for first couple of years its difficult to meet the need.But for long run own house has eyewitnesses different set of things like child growth,marriages etc,there is no fear of home changing.

like SIP if in metros home rates growing upto 13-15% ,so we can also get return after 15 years like balanced MF .So one can put some EMI in home loan and some money towards SIP

Thanks for the analysis….

May I please know….. if I prepay 1 Lakh loan I save 3.78 L of interest payment and taking 14 yrs to repay full loan. If I invest 1L in MF and wait for 14 yrs will I get return of 3.78L (1L principal and 3.78L return) post tax deduction ???? I assume i do not want to switch or churn my MF portfolio but simply wait n watch for 14 yrs.

Considering 10% inflation, no tax cut on prepayment but tax cut on MF return…. no rent payment as i have purchase house for self and no plans of selling it off even if there s appreciation in housing rates

Hi Apoorva,

Going by your calculations, it translates into 11.9% annualised return which when we look at, the mutual funds have scored over very easily. The average performance of large-cap funds over the last 14 years(as of 30 Jun 2017) is 19% annualised. For this return the Rs one lakh will have become Rs 11 lakhs(If you had invested in a top performing large-cap fund, this amount will be even greater). The same Rs 1 lakh would have become Rs 22 lakh had it been invested in mid-caps. Average performance of mid-cap funds between 30 Jun 2003 and 30 Jun 2017 is 24% annualised. And all this is post tax since for equity funds, the long-term capital gains (units of an equity fund held for greater than a year) is zero. And yes this is taking into consideration a buy and hold approach.

What about IT exemption on Interest for salaried

Past evidence that we have worked on suggests that the returns will adequately compensate for the exemption in tax we get from paying the interest. It is also to be notes that the exemption in tax we get from the interest we pay would actually be a minuscule part in the whole scheme of things.Also the interest that you pay on your EMI reduces as you advance in the tenure of your loan and subsequently the tax advantage you get keeps reducing. Further more, assuming that the property is let out for rent, once the rent received is greater than the interest paid, you will have to pay capital gains tax for the amount over and above the interest paid.