We covered taxation on mutual funds in detail last month, over two different posts. This week, we will go a bit more into detail, especially as many of you had questions regarding capital gains.

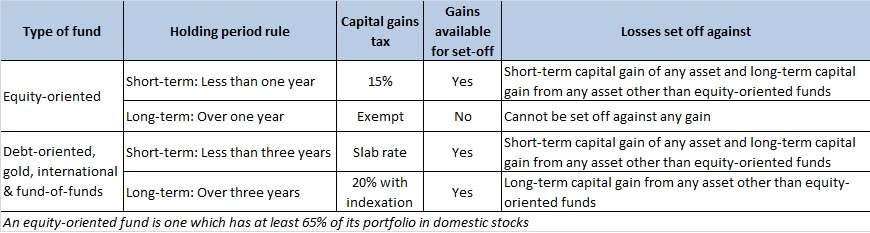

First, a brief recap. Long-term capital gains on equity-oriented funds (including equity balanced funds) are tax-exempt on holding for over twelve months. Short-term gains on equity-oriented funds are taxed at a flat 15 per cent, no matter your tax bracket.

On all funds other than equity-oriented funds, short-term gains are taxed at your tax slab rate. For such funds, short-term is defined as a holding period of less than 3 years. Long-term gains (holding period of over 3 years) are taxed at 20 per cent with indexation benefit. We’ve also explained how to use indexation.

Setting off

It is all very neatly laid out if you make capital gains. You pay taxes, where applicable, on the gains.

What happens in the case of losses? You set it off against the capital gains you made – that is, you reduce your capital gains by the amount of losses. As your gains reduce, your taxes also drop. If your capital gains aren’t enough to fully cover the losses, the unabsorbed loss can be carried forward into the next year, and set off against the capital gains made. Such carry forward can be done for eight years.

Since you have both long-term and short-term gains, and, depending on the type of fund the taxation differs, there are rules to such setting off.

– Long-term capital gains on equity-oriented funds, because they are tax-exempt, cannot be used to set off any loss whatsoever.

– For this same reason, long-term capital loss on equity-oriented funds cannot be set off against any capital gain.

– Short-term capital losses from all funds (equity-oriented and others), can be set off against both long-term and short-term capital gains.

– Long-term capital losses on all funds other than equity-oriented funds can be set off against long-term capital gains only.

Therefore, always remember to omit long-term capital gains on equity-oriented funds while arriving at the capital gains available for set off.

Understanding all this is easier with examples. Say you made short-term capital gains of Rs 50,000 on an equity fund. You also made a short-term capital loss of Rs 30,000 on a debt fund in the same year. You can set off this Rs 30,000 loss against the short-term gain. You now pay the tax only on Rs 20,000. If you had a long-term capital loss on the debt fund instead of the short-term, you cannot do such a set-off, and you pay tax on the entire Rs 50,000.

Understanding all this is easier with examples. Say you made short-term capital gains of Rs 50,000 on an equity fund. You also made a short-term capital loss of Rs 30,000 on a debt fund in the same year. You can set off this Rs 30,000 loss against the short-term gain. You now pay the tax only on Rs 20,000. If you had a long-term capital loss on the debt fund instead of the short-term, you cannot do such a set-off, and you pay tax on the entire Rs 50,000.

Take another example. You made long-term capital gain of Rs 50,000 on an equity fund. You had a short-term capital loss of Rs 30,000 on a debt fund. There is no set-off that you can do. Take a third example. You made a short-term loss on a debt fund for Rs 30,000. You made a long-term gain on a gold fund for Rs 50,000. You can set the loss off against the gain and pay 20% tax with indexation on the remaining Rs 20,000. If you had instead made a long-term loss on the debt fund, you can still set it off against the gain from the gold fund.

Set off against other assets

Now, it is important to remember that you can set off the long-term and short-term capital gains in other assets (where tax is not exempt) such as property or gold against your mutual fund loss. If you have a short-term capital loss in mutual funds, you can set it off against short-term or long-term capital gain in any other asset as well. If you have a long-term capital loss in your non-equity fund, you can set it off against only a long-term capital gain in any other asset.

Showing capital gains

Mutual fund houses don’t deduct taxes when you redeem the fund, unless you’re an NRI in which case TDS will apply. Calculating capital gains and paying the taxes due on them is your exercise. Capital gains are a separate source of income, under the Income Tax Act. Therefore, you need to list it separately as a different income head at the time you file your returns.

Now, what happens if your income outside of capital gains is less than the basic exemption limit? For individuals below 60 years of age, the basic exemption is Rs 2.5 lakh, for those between 60 and 80, it is Rs 3 lakh and for those above 80 years, the exemption limit is Rs 5 lakh.

Income tax rules allow you to reduce your long-term capital gains and short-term gains from equity to the extent your income falls short of the basic exemption limit. This rule applies only if you are a resident individual (or HUF) and not if you are an NRI investor.

For example, s say you’re 25 years old. Your taxable income is Rs 200,000 excluding capital gains. After completing all the available set-off, you have Rs 300,000 of long-term capital gains from your debt mutual fund, on which you need to pay tax. Now, the basic exemption slab that applies to you is Rs 250,000. So the difference between this limit and your income is Rs 50,000. You can use this Rs 50,000 to reduce your taxable capital gains. Therefore, you will pay 20% tax (with indexation) on Rs 250,000. Similarly, if you instead had Rs 300,000 worth of short-term capital gains from an equity fund, you will have to pay tax of 15% on Rs 250,000. But if the short-term capital gains came from a debt-oriented fund, then your taxable income jumps to Rs 500,000 (Rs 200,000 + Rs 300,000). This is because the gains are added to your income and taxed at your slab rate.

Shall be glad if you could guide me on the following:-

I have a lumpsum investment in a liquid fund with weekly dividend payout option. From this, fortnightly STP is being done to an equity fund. At the end of the financial year the liquid fund shows a capital loss (Short Term) as per statement obtained from CAMS. Can I use this loss as MF debt loss ot set off etc this loss while filing returns? Also how do I ensure that I do not violate IT act sec 94(7) regarding Dividend stripping.

Hello,

Really sorry about for the late reply. Unfortunately, you would have to consult a tax expert for your doubt. Dividend stripping provisions (where you can’t claim capital gains loss to the extent of dividend) apply when there is an investment made 3 months prior to a dividend being declared and the same is sold within nine months after the dividend declaration. Theoretically, there is a possibility that the provision can apply. It depends on when your first investment was in the liquid fund and when you started your STP. Capital gains calculation is on first-in-first-out basis.

Thanks,

Bhavana

Hi, it would be a great help if you can clarify the ambiguity in the article on “the capital gain taxes & set-off”

In the note it has been stated as follows but in the example it seems contradicting; i.e; short term capital gain from equity can be set off against short term capital loss from Debt.

Short-term capital losses from all funds (equity-oriented and others), can be set off against both long-term and short-term capital gains.

– Long-term capital losses on all funds other than equity-oriented funds can be set off against long-term capital gains only.

Example

“Understanding all this is easier with examples. Say you made short-term capital gains of Rs 50,000 on an equity fund. You also made a short-term capital loss of Rs 30,000 on a debt fund in the same year. You can set off this Rs 30,000 loss against the short-term gain. You now pay the tax only on Rs 20,000. If you had a long-term capital loss on the debt fund instead of the short-term, you cannot do such a set-off, and you pay tax on the entire Rs 50,000.”

Hi,

Short-term capital losses on any fund can be set off against both long-term and short-term capital gains, as long as the long-term capital gain does not come from an equity investment. This means that a short-term capital gain on equity can be used to set off a loss. In the example, the short-term loss was on the debt fund for Rs 30,000. The short-term gain was on the equity fund for Rs 50,000. Now, this equity gain can be set off against the debt loss. So the gain after setting off comes down to Rs 20,000 (50,000 gain less the 30,000 loss). The second part of the example explains what happens if this loss on the debt fund was not short-term in nature but long-term. In that case, it cannot be set off against the gain on the equity fund, since the gain is short term. So the taxable gain on the equity is the whole Rs 50,000. Hope it is clear; there is no ambiguity on this.

Thanks,

Bhavana

Thanks FundsIndia. This info is very useful.

Shall be glad if you could guide me on the following:-

I have a lumpsum investment in a liquid fund with weekly dividend payout option. From this, fortnightly STP is being done to an equity fund. At the end of the financial year the liquid fund shows a capital loss (Short Term) as per statement obtained from CAMS. Can I use this loss as MF debt loss ot set off etc this loss while filing returns? Also how do I ensure that I do not violate IT act sec 94(7) regarding Dividend stripping.

Hello,

Really sorry about for the late reply. Unfortunately, you would have to consult a tax expert for your doubt. Dividend stripping provisions (where you can’t claim capital gains loss to the extent of dividend) apply when there is an investment made 3 months prior to a dividend being declared and the same is sold within nine months after the dividend declaration. Theoretically, there is a possibility that the provision can apply. It depends on when your first investment was in the liquid fund and when you started your STP. Capital gains calculation is on first-in-first-out basis.

Thanks,

Bhavana

Hi, it would be a great help if you can clarify the ambiguity in the article on “the capital gain taxes & set-off”

In the note it has been stated as follows but in the example it seems contradicting; i.e; short term capital gain from equity can be set off against short term capital loss from Debt.

Short-term capital losses from all funds (equity-oriented and others), can be set off against both long-term and short-term capital gains.

– Long-term capital losses on all funds other than equity-oriented funds can be set off against long-term capital gains only.

Example

“Understanding all this is easier with examples. Say you made short-term capital gains of Rs 50,000 on an equity fund. You also made a short-term capital loss of Rs 30,000 on a debt fund in the same year. You can set off this Rs 30,000 loss against the short-term gain. You now pay the tax only on Rs 20,000. If you had a long-term capital loss on the debt fund instead of the short-term, you cannot do such a set-off, and you pay tax on the entire Rs 50,000.”

Hi,

Short-term capital losses on any fund can be set off against both long-term and short-term capital gains, as long as the long-term capital gain does not come from an equity investment. This means that a short-term capital gain on equity can be used to set off a loss. In the example, the short-term loss was on the debt fund for Rs 30,000. The short-term gain was on the equity fund for Rs 50,000. Now, this equity gain can be set off against the debt loss. So the gain after setting off comes down to Rs 20,000 (50,000 gain less the 30,000 loss). The second part of the example explains what happens if this loss on the debt fund was not short-term in nature but long-term. In that case, it cannot be set off against the gain on the equity fund, since the gain is short term. So the taxable gain on the equity is the whole Rs 50,000. Hope it is clear; there is no ambiguity on this.

Thanks,

Bhavana

Thanks FundsIndia. This info is very useful.

if fund house doesn’t deduct the tax so who deduct the mutual fund capital gains tax?

Hi Pankaj,

As we’ve mentioned in the article, it is the responsibility of every individual to calculate their capital gains, after completing available set-off. It isn’t possible for the AMC to know your total capital gains or loss across your investments. Once you calculate your gain and whether it is short-term or long-term, you will have to pay the applicable tax to the authorities. Hope its clear now.

Thanks,

Bhavana

if fund house doesn’t deduct the tax so who deduct the mutual fund capital gains tax?

Hi Pankaj,

As we’ve mentioned in the article, it is the responsibility of every individual to calculate their capital gains, after completing available set-off. It isn’t possible for the AMC to know your total capital gains or loss across your investments. Once you calculate your gain and whether it is short-term or long-term, you will have to pay the applicable tax to the authorities. Hope its clear now.

Thanks,

Bhavana

Very good informative article. Are you planning an article on carry forward rules as well ?

Could you please clarify whether long term capital loss on equity mutual funds cannot be carried forward also, not just it cannot be set off ? (Is it why such a loss is called “dead-loss” ?) I saw differing opinions about this on various websites.

A table which combines both set off and carry forward information will be helpful to FundsIndia users during tax returns. Such table is also hard to find for current FY and definitely a value add. 🙂

Hi,

Carry forward of losses is done when, in a year, you don’t have enough gains to set the losses off. As we’ve explained in the article, carry forward can be done for eight years. The rules for set-off remain the same when you when you’re carrying forward the loss. On long-term loss on equity, since you can’t set it off against any gain, there is no question of carrying it forward at all.

Thanks,

Bhavana

Thanks,

Bhavana

Very good informative article. Are you planning an article on carry forward rules as well ?

Could you please clarify whether long term capital loss on equity mutual funds cannot be carried forward also, not just it cannot be set off ? (Is it why such a loss is called “dead-loss” ?) I saw differing opinions about this on various websites.

A table which combines both set off and carry forward information will be helpful to FundsIndia users during tax returns. Such table is also hard to find for current FY and definitely a value add. 🙂

Hi,

Carry forward of losses is done when, in a year, you don’t have enough gains to set the losses off. As we’ve explained in the article, carry forward can be done for eight years. The rules for set-off remain the same when you when you’re carrying forward the loss. On long-term loss on equity, since you can’t set it off against any gain, there is no question of carrying it forward at all.

Thanks,

Bhavana

Thanks,

Bhavana

Question: If I made a gain after selling equity mutual fund (i had it for 5 years, hence no long term tax to be paid), should I need to report it in tax form indicating date bought / date sold, or I do not need to indicate in tax form since it is obvious.

Please let me know your views

Thanks

Report it under exempt income in the appropriate row after adding up other equity exempt income ( from selling of shares etc).

Be sure to preserve the Account statements for purchase and redemption you have received / downloaded from mutual fund house for at least 8 years in case there is enquiry / clarification demanded from Income Tax officer. Better preserve bank statements showing amount being transferred for purchase / after redemption.

Sorry for the delayed response. Technically, it has to be reported under exempt income. Vidya

Question: If I made a gain after selling equity mutual fund (i had it for 5 years, hence no long term tax to be paid), should I need to report it in tax form indicating date bought / date sold, or I do not need to indicate in tax form since it is obvious.

Please let me know your views

Thanks

Sorry for the delayed response. Technically, it has to be reported under exempt income. Vidya

Report it under exempt income in the appropriate row after adding up other equity exempt income ( from selling of shares etc).

Be sure to preserve the Account statements for purchase and redemption you have received / downloaded from mutual fund house for at least 8 years in case there is enquiry / clarification demanded from Income Tax officer. Better preserve bank statements showing amount being transferred for purchase / after redemption.

Hi,

I was wondering what is the taxation rule for capital gain/loss arising due to sale of restricted stock units listed on Nasdaq for Indian Residents?

And is it possible to set off capital gain/loss on sale of RSUs (listed on US stock exchange) against capital loss/gain on sale of debt oriented mutual funds?

Thanks,

Bhaskar

Hi Bhaskar,

RSU gains have tax implications in both countries. Please check with an auditor to understand the taxability in your case.

Thanks,

Bhavana

Could you throw light on LTCG applicable on a debt fund that has dividend payout and has been invested for more than 3 years?

When I redeem the invested units, can I use indexation to determine the Capital Gains? Should the dividend paid in the year be added, and if so for what period?, or since dividends have already suffered dividend distribution tax, can they be excluded?

thank you

You can claim indexation on your LTCG on your debt fund, irrespective of whether you had the dividend or growth option. Either way, you have made capital gains on the units you sold. Dividend is a separate income altogether. You don’t need to add it to your capital gains to determine your capital gain taxes. Its already got the applicable tax deducted, as you’ve noted.

Thanks,

Bhavana

thank you. Most often since the gains are given away as dividend what is left is just a little more than the principal so with indexation, I have found them to be a net loss

Could you throw light on LTCG applicable on a debt fund that has dividend payout and has been invested for more than 3 years?

When I redeem the invested units, can I use indexation to determine the Capital Gains? Should the dividend paid in the year be added, and if so for what period?, or since dividends have already suffered dividend distribution tax, can they be excluded?

thank you

You can claim indexation on your LTCG on your debt fund, irrespective of whether you had the dividend or growth option. Either way, you have made capital gains on the units you sold. Dividend is a separate income altogether. You don’t need to add it to your capital gains to determine your capital gain taxes. Its already got the applicable tax deducted, as you’ve noted.

Thanks,

Bhavana

thank you. Most often since the gains are given away as dividend what is left is just a little more than the principal so with indexation, I have found them to be a net loss

Hello,

I had a long term capital gain of 1 Cr. I had bought a plot of 80Lacs the previous year, which I used to set off against the gains. The balance 20 lacs was put in a FD in a nationalised bank towards construction of house.

Now three years later the FD is getting matured, but the plot has still not been given to possession by the builder. What can I do?

Will I have to pay tax on the entire 1 Cr gains?

Or will I have to pay tax only on the 20 lacs balance?

Hello,

Please seek the advice of your auditor, since property and the taxes and options involved are not in our ambit.

Thanks,

Bhavana

Hi,

I was wondering what is the taxation rule for capital gain/loss arising due to sale of restricted stock units listed on Nasdaq for Indian Residents?

And is it possible to set off capital gain/loss on sale of RSUs (listed on US stock exchange) against capital loss/gain on sale of debt oriented mutual funds?

Thanks,

Bhaskar

Hi Bhaskar,

RSU gains have tax implications in both countries. Please check with an auditor to understand the taxability in your case.

Thanks,

Bhavana

Hello,

I had a long term capital gain of 1 Cr. I had bought a plot of 80Lacs the previous year, which I used to set off against the gains. The balance 20 lacs was put in a FD in a nationalised bank towards construction of house.

Now three years later the FD is getting matured, but the plot has still not been given to possession by the builder. What can I do?

Will I have to pay tax on the entire 1 Cr gains?

Or will I have to pay tax only on the 20 lacs balance?

Hello,

Please seek the advice of your auditor, since property and the taxes and options involved are not in our ambit.

Thanks,

Bhavana