How many of us know that the social security net in India is almost non-existent? And that your EPF is a very poor attempt at creating social security. NPS, a slightly improvised version, is yet to gain acceptance, thanks to its complexity and poor taxation structure. In such a scenario, it becomes imperative that we save enough for our retirement.

However, young people who join the workforce, are not geared towards financial prudence and do not start thinking about savings and investment right away. So here is a list of six mistakes one should avoid making early on in their financial life.

1. Delaying the habit of investing

Having spent our college lives on shoestring budgets, when we get that first salary credited to our bank account, we have a tendency to splurge. But hold on for a minute, this urge to spend now can get you into trouble later on.

The chapter on compound interest you had in school was not just theory. It is now time to see that into action. When you make any investment, your returns get compounded every year. The earlier you start investing, the more time your investments have to compound. The more your returns compound, the more you will accumulate.

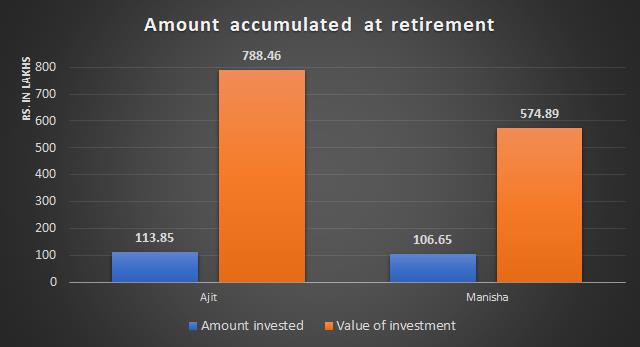

Take the case of Ajit and Manisha. Both of them started working at the age of 25. While Ajith started investing right away, Manisha waited till she turned 30. Both of them invested similar amounts, Ajit starting with Rs. 10,000 and Manisha with Rs. 15,000. They increased it by Rs. 1000 every year. However, when they turned 60, this is where they both ended up:

A delay of five years caused Manisha to fall short by over Rs. 2 crore. So start early to accumulate a sufficient amount.

2. Spending through credit card

As soon as you open a salary account, you will get a call from your bank to get a credit card. Credit card is just the thing a spendthrift needs. You spend without worrying and pile up your credit. You barely manage to pay the minimum amount every month. And very soon, you find yourself paying huge amounts of interest on the accumulated credit.

Credit cards come with very high interest rates, going as high as 42% per year. Spending money you do not have can get you into a debt trap. You will eventually find yourself spending more money paying the accumulated interest, than you spent for yourself.

3. Spending using personal loans

OK, so credit cards are expensive, but what about personal loans and EMI payments? You will be bombarded with ads offering you pre-approved personal loans at rates as low as 14%. They tempt you into buying goods you cannot afford. You may have only Rs. 30,000 in your bank account, but you take a personal loan for Rs. 40,000 to buy the latest Google Pixel phone. You will take another personal loan and go on a Europe trip with your friends.

Spending on luxuries you cannot afford will only eat into your corpus. Instead, plan for the long haul. Start with cheaper gadgets and trips closer home. This will help you save more in the initial stages of your life. As you move up in your career, you will have more opportunities to splurge.

4. Investing without understanding the product

Another mistake which people make is to not spend time understanding where they should invest their money. A young person tends to receive advice from his parents, uncles, senior colleagues, and these days, knowledge sharing social networks. None of these will understand your needs or advice you properly. Investing without understanding the product can land you into trouble, the kind which people got into last year when they invested huge amounts in Bitcoins.

You should neither rush to put your money in banks, nor rush to invest in equities. Nor should you fall into the trap of Ponzi schemes. So take a couple of weekends to think about your investments. Spend some time understanding the products available and the pros and cons of each. Then make an informed decision.

5. Trying to stay away from risks

While there are people who put their money only in banks, there will be people who swear by equities. Neither of the extremes are good. While you should not take too much risk, you should also not be too risk averse.

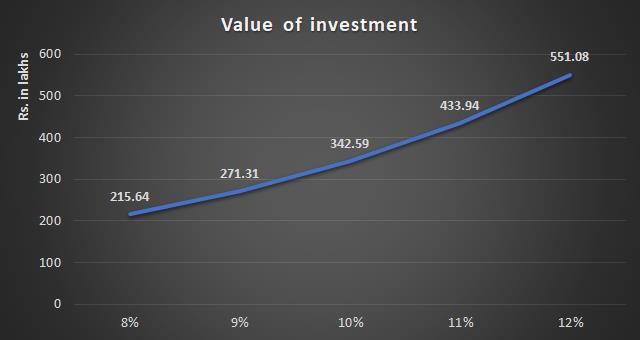

Equity and equity related products like mutual funds are risky. But they also come with risk premium. There is a reward for taking the risk and this reward is higher returns. Over a long period of time, even 1-2% return differential can create a huge difference in your corpus.

Here is a comparison of how much a monthly deposit of Rs. 10,000 grows to in 35 years, at various rates of interest:

If you stay away from risk, you risk missing out on the huge potential of equities.

6. Buying a home too early

We have a great emotional attachment to our homes. Owning a house is also associated with social status and prestige. As a result, as soon as we start earning, we want to have our own apartments. Within a few years, we find ourselves saddled with a huge home loan, zero savings, and only one illiquid asset that is the apartment. The next few years are spent paying the EMI only. By the time we can start saving, we have already missed the early bus.

Don’t be in a hurry to buy a house. Again, after having saved for a few years and after having made some progress in your career, you will be in a much better position to buy a house according to your needs. Taking a home loan early on not only gets you into a financial mess, it also restricts your career choices.