A recent article by Dhirendra Kumar of Valueresearch ‘Debt funds’ self-inflicted losses’ came as a surprise. The article surprised me for some of the assumptions it made about debt fund as a product, about what investors want and about how fund managers act.

First, the assumption that debt fund is inherently a capital preservation product is not true. It could be a capital preservation product if returns are guaranteed and capital is protected. While fund houses can do so by setting aside reserves to protect capital, no fund house with its limited profitability/reserves has guaranteed capital although they try innovative ways to make them ‘capital-protection oriented’. Debt funds are mostly market-linked products. I say mostly here, because in the case of liquid funds, theoretically the coupon is converted to returns (post expense). Other than this category of funds, debt funds, either because of the duration risk or credit risk, can never be a capital preservation product; at least not unless they are held for the time frame they are recommended for.

A fund that holds any listed bond with a medium to long-term maturity – whether government bond or corporate bond – cannot avoid losses on a day when yields move up sharply. The pain is higher when the instruments have longer residual maturity and lesser when the maturity is low. This is exactly what transpired on the day of Monetary policy as well. Please refer to our article ‘Should you worry about debt fund declines’

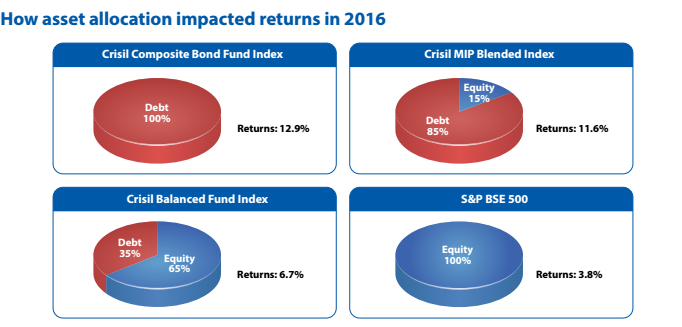

While I will certainly not say that a debt fund does all the jobs that an investor wants it to do: we know debt funds provide some hedge to an investor’s portfolio. Just to illustrate, the image below tells you in a year like 2016, debt funds helped curtail the equity falls for investors. Even a 35% debt helped ensure that you were less impacted in a volatile equity market. What they try to do is lessen the shock of equities. They do not state that they will not provide any shocks themselves.

Second, the article makes an implicit assumption that investors come to debt funds for capital preservation and that they cannot handle losses.

An investor who wants capital preservation will stay with his/her savings account or deposit or hold cash. To come into mutual funds thinking that the same preservation is possible but with higher returns is at best delusional. Here, I agree that there is poor awareness and mis-selling by some, making an investor believe that it is possible to get superior returns with no risk.

That said, the fact – as stated by thousands of our own investors – is that people come seeking FD-plus returns or savings bank plus returns when they seek debt funds. Most of them do not understand inflation-beating returns. It is not a benchmark for them to comprehend or compare. And debt funds mostly achieve that, especially on a post-tax basis.

(That debt funds, incidentally provide some hedge against the deep losses when equity markets are down, is an added benefit, that the investors understand, but only after experiencing it. That has been our experience with our customers).

The shock or pain comes to investors where they believed or were made to believe that high returns is possible from long-term debt products, without any downside risks. This typically happens when the investors picks a fund that was not meant to fulfil the job he wanted it to do. We will talk about this a little later.

In other words, the problem arises when investors choose or are made to choose the wrong category of products.

Third, in this specific instance, the article states that fund managers took bet on what the RBI Governor would do. A look at how fund managers have been managing their duration (please read our article on should you worry about debt fund declines) will tell you that directionally, they have been reducing their portfolio maturities, believing that the rate cycle was coming to an end. This is true of dynamic bond funds and long-term gilt funds. That they believed there could be some more cuts was evident because the average duration did not go very low. But that they have steadily cut it suggests that fund managers were taking no sharp bets.

Is the product doing the job it is hired to do?

So, what is the real problem? One can accuse fund houses of upping the complexity of an already complex product, in the name of innovation (read compulsion to garner AUM). But then, is it not the case with all manufacturers? Can there be any less complex products in the insurance or banking industry? Or for that matter, in equity funds – equity savings, balanced advantage, arbitrage, retirement, you name them.

The problem, as I see it, is not in innovating. A product, however well designed would not be successful if it does not do the job for which the investor sought it in the first place (do read the book ‘Competing against luck’ by Clayton Christensen. I am borrowing the learnings from this book).

The quiet burial being given to RGESS is a classic example of poorly designed product that does not really satisfy an investor’s need.

Understanding why an investor sought a product and offering him that product which will fulfil that job for him/her is the key.

- An investor looks for a product to park his money with no time frame in his/her mind – there are liquid funds and ultra short-term funds

- An investor wants a substitute for FD in the medium to long term there are short-term debt funds and income accrual funds.

- An investor does not want to be subject to the vagaries of a changing rate cycle there are dynamic bond funds

- Large investors who want to bet/trade on the rate cycle there are gilt funds

The real problem

Of course, I am far from claiming all is well with what we do. The point I wish to drive here is that funds making losses or fund managers getting one call wrong is not the problem. Those are risks inherent to mutual funds and investors and fund managers learn.

The problem is as follows: At the AMC level, while innovation is welcome, any innovation that does not sufficiently study the problem/job that the product will solve/fulfil for a customer will be a wasted one. Whether the investor wants capital preservation or returns maximisation and what is good for him, is not for any of us – AMCs, experts or distributors – to decide by ourselves. It is for us to observe learn and respond accordingly. The same lies with the distributor. Insufficient understanding or ignoring the real reason of why the customer came to us, is the folly.

A product that does not fulfill that one real need for the customer and the distributor who fails to understand that need and place the right product is the real loser; not the customer.

Very well explained. If the fund manager or fund house misleads us, the investors, then they are the real loosers in the long run. As an investor, i put my bets on the fund manager who gives us quality returns. And i try to invest in the other funds managed by him to diversify my portfolio. Great insight into debt funds. Thanks

Dhirendar kumar is absolutely right , debt funds are for capital preservation. We chose debt funds for 2 reasons – saving tax as it has indexation benefit and fd beating returns(small percentage). Generally when you are nearing your goal (3years), one shifts his money accumulated in equity to debt mf as equity is unpredictable within 3 years. So here debt mf act as capital protection. If someone wants to stay invested for more than 5 yrs, it is better to invest in equity. Distributor like fundsindia has advised me to invest in Franklin India Income Opportunities fund in 2014 as my duration was more than 3 yrs . this fund has performed badly in terms of returns compared to Birla dynamic bond fund. It is good to invest in liquid or ultra short term funds but fund manager has to stay to its objective. There are fund managers who are over ambitious to give better returns than equity. Avoid them.

Arun, Thanks for sharing your thoughts. The problem is most debt funds are not built for capital preservation. They are not structured so. The point here is if capital preservation is the key, you should be willing to stay with the fund for the said time frame. Just as you would not sit with equities for a year and complain of losses it is the same with long-term debt funds. In the case of Franklin India Income Opportunities, as you rightly pointed out, the fund took a credit bet that went bad. It was indeed a risky move and the fund manager was punished for the same, although the fund house managed to significantly contain the loss by selling the instrument. Also, the said fund is a long-term high risk fund. But holding it for the time frame it is intended for ( I do not think the FundsIndia advisor would have given it to you as a short term fund. If he/she did please let me know), would have ensured you earned the yield in that fund. For example if one entered in 2014 it needs a 2017 time window at least. This is for the simple reason, the fund’s underlying instruments have such a maturity.

If the time frame were shorter and one does not want any fall in between, then as you said liquid and ultra short term fund would have done the job.

Also Birla Sun Life dynamic bond and Income opportunities are entirely different plays. Dynamic bond funds simply seek to ride the interest rate wave and they found a favourable year in 2016.

NO debt fund manager can even aspire to beat equities in the long term.They simply play the rate game or credit game. Only in the rate rally do they even get double digit returns and that too only for a short duration.So it is pointless for them to be chasing equity returns and they do not do that. They only try to make good when the opportunity is there. Of course, they miss it too. And that is par for the course.

If you did not go to a fund for high returns, you are right, the category of fund for you is liquid, ultra short or short-term debt. But there are others with other requirements.

Also, you are absolutely right that some funds do not stay to their true objective and keep changing their colour. They lose in the long term, trying to chase returns.

As for investors, the point is only one: when one sees high returns, it is logical to assume that it can only come with higher risks. Most investors lose sight of the second point.

thanks, Vidya

Hi Vidya

Thanks for the reply. I have no regrets investing in Franklin India Income Opportunities fund as it gave 9% + returns beating fd. I only invest in debt funds for capital preservation , fund should hold only bonds of high quality companies. I am not ready to accept 2-3 % fall in debt funds in a day ,even though I am in for 10% fall in equities. For equity funds I am ready for volatility. I can choose my own equity fund but I can’t choose my debt fund there are so complex. That’s why we need help from fundsindia to help us select a debt mutual fund which is less risky, less volatile and easily liquid(redemption in 1-2 days).it may not necessarily beat fd returns.

I have another query what’s your view on axis long term equity mutual fund. This fund is performing badly but this fund holds excellent companies. Many sites like mint 50 , moneycontrol have rated 2 out of 5. Mint50 has advised to exit on completion of lock in period. I am investing through sip.

Below is there analysis copied from http://www.livemint.com/Money/rmrbriDOFeIM6MioiUr15M/Schemes-that-exited-Mint50.html

“Axis Equity Fund and Axis Long Term Equity Fund: The past 2 years have been tough for equity fund management at the fund house. Poor performances and an exodus of fund managers (Pankaj Murarka, former head-equities, quit in July 2016 and another senior fund manager Sudhanshu Asthana quit thereafter) do not bode well.

Returns of Axis Equity Fund (AEF) have been disappointing and Axis Long Term Equity Fund (ALTE), too, had a bumpy ride in 2016. Given the uncertainty in the fund management team, we have decided to drop both the funds from Mint50.

AEF, a large-cap oriented equity fund, lost a little over 1% and a little under 4% in 2015 and 2016, respectively. In both these years, it finished in the bottom quintiles when compared to peers.

The scheme’s management has been aggressive on a few counts. For instance, it first invested, then exited, then re-entered some large companies such as State Bank of India and Bank of Baroda. “One lesson we have learnt is that if we hold on to companies—and the reasons why we bought them—for long, the chances of such holdings working in our favour increase. We bought shares to some of the larger names at the right time perhaps, but we may not have held them long enough,” said a senior fund official who did not wish to be named.

We suggest that you stop systematic investment plans (SIPs) in these and exit once they complete the exit load (for AEF) and lock-in period (for ALTF).”

Kiran,

Quite a few Axis funds have lagged in performance mainly because some of their stock calls went wrong and can in rather late. We are watching their performance. We are still on the watch mode for Axis LTE as some of the fund’s holdings in financials, auto and chemicals seem promising. I tried to check your time/timings of entry (with the email id provided in this blog) but could not find an account with this id. Do you have a different id? On Axis Equity, we removed it from our select list in October 2016. That means no fresh investments. Just hold and watch.

thanks

Vidya

Now I have shared the correct id while reply. I have been doing sip in Axis Long Term Equity since July 2014. That ‘s the only fund where I invested whole of my ELSS contribution. I have stopped sip from this month as i exhausted the 80c limit this year. I may not invest in ELSS in future as my 80c would be consumed by EPF and principal towards home loan from next financial year.

However I will continue investing in Parag Parikh Long Term Value fund through sip, i really liked the portfolio and diversification of this fund.

The money that is saved in Axis Long Term Equity and PPFAS long term value funds is for my retirement goal.

Could you explain how holding on to the fund for the entire duration would help, especially for long term duration funds?

Interest rates are cyclical as much as I can understand. They do not remain in one direction within a long period. They typically (in India) try to change direction every 3 – 5 years. So, if the decreasing interest rate cycle has ended, how would long duration debts provide returns? wouldnt at every interest rate rise, the value go down eroding the capital and the returns?

Wouldnt it be prudent for long duration funds to also reduce their long duration instruments in such an environment?

If investors have to do this looking at the RBI and switch funds midstream, then their tax benefits of staying invested is lost.

Hello Sir, Long-term gilt funds cannot provide high returns once the falling rate scenario is done. They cannot go for short-temr gilt as that is not their mandate. However, dynamic bond funds actively book profits and reduce the duration of the fund. That is how they manage to deliver better than long-term gilt funds in the long run. Thanks, Vidya

Thank you.

A follow up question if you dont mind. I am trying to understand the objectives of these funds better !

A disclosure that I have not made any purchases through FundsIndia yet.

So, in a scenario of likely upward interest rates, for a long term (say 3 to 5 years) investor in debt funds, apart from the dynamic funds, what other funds are likely to give a good return?

In a discussion on Debt investment with fund advisors, the first question that comes up is the term period one is looking to invest. If this is the basis, how do funds such as Income or Corporate Debt fund work? Do they also change the duration dynamically based on the interest rate situation? Or should these funds be avoided in a interest-up cycle? What should one who has already chosen an Income fund do now?

thank you

Hello Sir, sorry for the delayed response. In a rising rate scenario, accrual will yield well as it means funds will hold higher yielding papers. Accrual can be ultra short term, short term, medium term or credit opportunity. thanks, Vidya

Madam,

I would be grateful if you could suggest me whether I should stick with Birla Sunlife Dynamic Bond Fund (Growth) , ICICI Prudential Long Term (Growth) and HDFC High Interest Fund Dynamic (Growth). I have made lumpsum investments in these three funds during November, 2016 and since then all of them are giving negative returns. I am confused whether I should continue with them or switch over to some other funds. Your suggestion in this rehard will help me a lot.

Regards,

Sujoy

Kolkata

Hello Sir,

Sorry for the delayed response. Please stick to debt funds for the time frame your originally intended and do not get swayed by market volatility in debt. To review specific funds, please get in touch with us through your FundsIndia account. thanks, Vidya

Madam,

I would be grateful if you could suggest me whether I should stick with Birla Sunlife Dynamic Bond Fund (Growth) , ICICI Prudential Long Term (Growth) and HDFC High Interest Fund Dynamic (Growth). I have made lumpsum investments in these three funds during November, 2016 and since then all of them are giving negative returns. I am confused whether I should continue with them or switch over to some other funds. Your suggestion in this rehard will help me a lot.

Regards,

Sujoy

Kolkata

Hello Sir,

Sorry for the delayed response. Please stick to debt funds for the time frame your originally intended and do not get swayed by market volatility in debt. To review specific funds, please get in touch with us through your FundsIndia account. thanks, Vidya

Dhirendar kumar is absolutely right , debt funds are for capital preservation. We chose debt funds for 2 reasons – saving tax as it has indexation benefit and fd beating returns(small percentage). Generally when you are nearing your goal (3years), one shifts his money accumulated in equity to debt mf as equity is unpredictable within 3 years. So here debt mf act as capital protection. If someone wants to stay invested for more than 5 yrs, it is better to invest in equity. Distributor like fundsindia has advised me to invest in Franklin India Income Opportunities fund in 2014 as my duration was more than 3 yrs . this fund has performed badly in terms of returns compared to Birla dynamic bond fund. It is good to invest in liquid or ultra short term funds but fund manager has to stay to its objective. There are fund managers who are over ambitious to give better returns than equity. Avoid them.

Arun, Thanks for sharing your thoughts. The problem is most debt funds are not built for capital preservation. They are not structured so. The point here is if capital preservation is the key, you should be willing to stay with the fund for the said time frame. Just as you would not sit with equities for a year and complain of losses it is the same with long-term debt funds. In the case of Franklin India Income Opportunities, as you rightly pointed out, the fund took a credit bet that went bad. It was indeed a risky move and the fund manager was punished for the same, although the fund house managed to significantly contain the loss by selling the instrument. Also, the said fund is a long-term high risk fund. But holding it for the time frame it is intended for ( I do not think the FundsIndia advisor would have given it to you as a short term fund. If he/she did please let me know), would have ensured you earned the yield in that fund. For example if one entered in 2014 it needs a 2017 time window at least. This is for the simple reason, the fund’s underlying instruments have such a maturity.

If the time frame were shorter and one does not want any fall in between, then as you said liquid and ultra short term fund would have done the job.

Also Birla Sun Life dynamic bond and Income opportunities are entirely different plays. Dynamic bond funds simply seek to ride the interest rate wave and they found a favourable year in 2016.

NO debt fund manager can even aspire to beat equities in the long term.They simply play the rate game or credit game. Only in the rate rally do they even get double digit returns and that too only for a short duration.So it is pointless for them to be chasing equity returns and they do not do that. They only try to make good when the opportunity is there. Of course, they miss it too. And that is par for the course.

If you did not go to a fund for high returns, you are right, the category of fund for you is liquid, ultra short or short-term debt. But there are others with other requirements.

Also, you are absolutely right that some funds do not stay to their true objective and keep changing their colour. They lose in the long term, trying to chase returns.

As for investors, the point is only one: when one sees high returns, it is logical to assume that it can only come with higher risks. Most investors lose sight of the second point.

thanks, Vidya

Hi Vidya

Thanks for the reply. I have no regrets investing in Franklin India Income Opportunities fund as it gave 9% + returns beating fd. I only invest in debt funds for capital preservation , fund should hold only bonds of high quality companies. I am not ready to accept 2-3 % fall in debt funds in a day ,even though I am in for 10% fall in equities. For equity funds I am ready for volatility. I can choose my own equity fund but I can’t choose my debt fund there are so complex. That’s why we need help from fundsindia to help us select a debt mutual fund which is less risky, less volatile and easily liquid(redemption in 1-2 days).it may not necessarily beat fd returns.

I have another query what’s your view on axis long term equity mutual fund. This fund is performing badly but this fund holds excellent companies. Many sites like mint 50 , moneycontrol have rated 2 out of 5. Mint50 has advised to exit on completion of lock in period. I am investing through sip.

Below is there analysis copied from http://www.livemint.com/Money/rmrbriDOFeIM6MioiUr15M/Schemes-that-exited-Mint50.html

“Axis Equity Fund and Axis Long Term Equity Fund: The past 2 years have been tough for equity fund management at the fund house. Poor performances and an exodus of fund managers (Pankaj Murarka, former head-equities, quit in July 2016 and another senior fund manager Sudhanshu Asthana quit thereafter) do not bode well.

Returns of Axis Equity Fund (AEF) have been disappointing and Axis Long Term Equity Fund (ALTE), too, had a bumpy ride in 2016. Given the uncertainty in the fund management team, we have decided to drop both the funds from Mint50.

AEF, a large-cap oriented equity fund, lost a little over 1% and a little under 4% in 2015 and 2016, respectively. In both these years, it finished in the bottom quintiles when compared to peers.

The scheme’s management has been aggressive on a few counts. For instance, it first invested, then exited, then re-entered some large companies such as State Bank of India and Bank of Baroda. “One lesson we have learnt is that if we hold on to companies—and the reasons why we bought them—for long, the chances of such holdings working in our favour increase. We bought shares to some of the larger names at the right time perhaps, but we may not have held them long enough,” said a senior fund official who did not wish to be named.

We suggest that you stop systematic investment plans (SIPs) in these and exit once they complete the exit load (for AEF) and lock-in period (for ALTF).”

Kiran,

Quite a few Axis funds have lagged in performance mainly because some of their stock calls went wrong and can in rather late. We are watching their performance. We are still on the watch mode for Axis LTE as some of the fund’s holdings in financials, auto and chemicals seem promising. I tried to check your time/timings of entry (with the email id provided in this blog) but could not find an account with this id. Do you have a different id? On Axis Equity, we removed it from our select list in October 2016. That means no fresh investments. Just hold and watch.

thanks

Vidya

Now I have shared the correct id while reply. I have been doing sip in Axis Long Term Equity since July 2014. That ‘s the only fund where I invested whole of my ELSS contribution. I have stopped sip from this month as i exhausted the 80c limit this year. I may not invest in ELSS in future as my 80c would be consumed by EPF and principal towards home loan from next financial year.

However I will continue investing in Parag Parikh Long Term Value fund through sip, i really liked the portfolio and diversification of this fund.

The money that is saved in Axis Long Term Equity and PPFAS long term value funds is for my retirement goal.

Could you explain how holding on to the fund for the entire duration would help, especially for long term duration funds?

Interest rates are cyclical as much as I can understand. They do not remain in one direction within a long period. They typically (in India) try to change direction every 3 – 5 years. So, if the decreasing interest rate cycle has ended, how would long duration debts provide returns? wouldnt at every interest rate rise, the value go down eroding the capital and the returns?

Wouldnt it be prudent for long duration funds to also reduce their long duration instruments in such an environment?

If investors have to do this looking at the RBI and switch funds midstream, then their tax benefits of staying invested is lost.

Hello Sir, Long-term gilt funds cannot provide high returns once the falling rate scenario is done. They cannot go for short-temr gilt as that is not their mandate. However, dynamic bond funds actively book profits and reduce the duration of the fund. That is how they manage to deliver better than long-term gilt funds in the long run. Thanks, Vidya

Thank you.

A follow up question if you dont mind. I am trying to understand the objectives of these funds better !

A disclosure that I have not made any purchases through FundsIndia yet.

So, in a scenario of likely upward interest rates, for a long term (say 3 to 5 years) investor in debt funds, apart from the dynamic funds, what other funds are likely to give a good return?

In a discussion on Debt investment with fund advisors, the first question that comes up is the term period one is looking to invest. If this is the basis, how do funds such as Income or Corporate Debt fund work? Do they also change the duration dynamically based on the interest rate situation? Or should these funds be avoided in a interest-up cycle? What should one who has already chosen an Income fund do now?

thank you

Hello Sir, sorry for the delayed response. In a rising rate scenario, accrual will yield well as it means funds will hold higher yielding papers. Accrual can be ultra short term, short term, medium term or credit opportunity. thanks, Vidya

Very well explained. If the fund manager or fund house misleads us, the investors, then they are the real loosers in the long run. As an investor, i put my bets on the fund manager who gives us quality returns. And i try to invest in the other funds managed by him to diversify my portfolio. Great insight into debt funds. Thanks