The single-day fall in medium and long-term debt funds ranging from 0.1% to 2.2% on February 8, 2017, following the Monetary Policy, might look alarming. There were also sections of the media blaming fund managers for betting on the Monetary Policy and losing money for investors. Is this really the case? Why did we have that kind of fall and what should you be doing when your debt fund falls? We’ll try to discuss these as many of you have asked us what you should do with your funds.

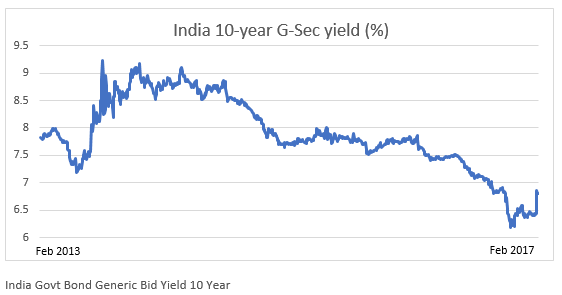

First, the sharp rise in 10-year government yields by as much as 32 basis points or 4.9% on policy day caused gilt prices to fall by about 2% on a single day. The chart below shows the extent of spike on budget day. However, as can be observed, it is nowhere near what we faced in July 2013, when yields moved by as much as 6.7% on a single day and between 4-5% on subsequent days in August, same year.

Now, the 2013 fall was triggered by many events, including the crash of the rupee and steep rate hikes. So, what could be the trigger this time around as nothing dire happened other than the RBI not announcing a rate cut? Let’s take a step back to answer this.

We believe the debt market equation has significantly changed with the increased participation of FPIs (foreign portfolio investors) in the debt markets. Let us consider these facts:

- The net inflow into debt by FPIs was about Rs. 35,000 crore in 2012 (calendar year). Fast forward 2 years. – 2014 – the net inflows into debt by FPIs was a whopping Rs. 1,59,000 crore or a 4.5 times surge. Since then, there have been months of huge inflows as well as outflows.

- Just to put the nature of outflows into perspective: in one of the worst periods for debt – July 2013, FPIs pulled out a net Rs. 12,000 crore. Now in the month of November 2016, FPIs pulled out a net Rs. 21,151 crore and followed it with another Rs. 18,935 crore in December 2016. And yet, the pressure on yields was not as significant, since these outflows were accompanied by substantial inflows as well.

- Now on February 8, 2017, FPIs pulled out a net Rs. 862 crore and yet February still has net inflows of Rs. 4,450 crore.

- The yield curve itself shows that we have been in a period of prolonged gentle decline in yields beginning 2014, lasting for 3 years now, with temporary up moves. That means, we were headed towards the end of a rate cycle, prompting many large investors to exit; but for the correction that happened on February 8. That there were net outflows in November and December 2016 suggests that profit booking started a few months ago.

Why did we talk about FPI inflows and outflows? The point here is simple: Higher participation by institutional investors, specifically FPIs has led to higher volatility in the gilt market. And long-term gilt being the most traded instrument, it is subject to maximum volatility. Of course, this together with the continuous liquidity measures by RBI has made the debt market far more active than it was earlier.

While the extent of fall is not like equity markets, you need to note that higher liquidity and participation means higher volatility and that is what this segment is going through. For new investors in debt, the recent fall will be a hard lesson but well learnt.

Fund performance

Now coming to the fall in fund returns, logically, funds with higher maturity and those with higher traded securities (top-rated corporate bonds) would be the ones to fall the most and this theory has played out. The accompanying table shows that while long-term gilt funds fell the most on February 8, income accrual/short-term and ultra short-term funds fell the least and liquid funds were unhurt.

| Category | Avg. Returns (%) for 1 day* |

|---|---|

| Long-Term Gilt | -1.8% |

| Dynamic Bond | -1.3% |

| Income accrual | -0.8% |

| Credit Opportunity | -0.5% |

| Short-term debt | -0.5% |

| Ultra short-term debt | -0.16% |

| Liquid | 0.02% |

| *Returns as of Feb 8. Category returns for FundsIndia categories. | |

Now, you might wonder if the fund managers took bets on further rate cuts and therefore took a hit when the rate cut did not happen. Take a look at the average maturity of debt funds and you will see that fund managers have been slowly reducing the duration of their funds suggesting that they did not anticipate any opportunity in keeping the duration very high.

We took just those categories which play on duration. Needless to say, long-term gilt funds cannot reduce their duration much as their mandate is to hold long bonds. But dynamic bond funds have been actively reducing. However, that they expected more rate cuts to happen is obvious from their average maturity being higher than what would be necessary if we are at the end of a rate cycle.

While one can debate whether fund managers should have reduced their maturities further, the fact remains that fund houses did not take any big bets on rate cuts. Rather, they were preserving the profits by gradually moving to lower maturity securities.

| Month | Avg. maturity of gilt funds (years) | Avg. maturity of dynamic bond funds (years) |

|---|---|---|

| July 2016 | 13.7 | 10.5 |

| August 2016 | 12.3 | 10.0 |

| September 2016 | 12.3 | 10.2 |

| October 2016 | 10.5 | 9.6 |

| November 2016 | 13.4 | 11.6 |

| December 2016 | 11.0 | 9.25 |

| January 2017 | 10.1 | 7.8 |

| As of January 2017, based on available data | ||

What now

What surprised the debt market was the ‘neutral’ stance taken by the RBI from an ‘accommodative’ stance so far. And that has indeed pushed yields up. A neutral stance, in simple terms, suggests that unless there is sound reason (backed by inflation), there is no reason to accommodate further rate cuts.

We believe we were nearing the end of a rate cycle but for the correction that has taken the yields back to October 2016 levels. That means there does remain room for yields to ease, although it is unlikely that it will happen any time soon. In fact, don’t be surprised if you see the current yield up move continuing for some time. That means more correction but also entry opportunities for those who want to invest.

Before we move on to what you should be doing, here are a few points you need to keep in mind about debt funds:

- Debt funds can be volatile; especially those that take active interest rate calls. And interest rate calls can go wrong, just as equity calls do

- Choose the right category of debt funds based on your time frame and stick to it. This is important if you do not want to suffer losses

- Do not expect debt funds to never fall. If you enjoyed those 12-15% returns in one year, be prepared for falls as well

- Stick to short-term debt/income funds (based on your time frame) instead of dynamic bond funds if you do not like volatility

As for what you should do now:

- Continue to hold the category of funds (other than long-term gilt funds) you have, for the time frame you originally intended.

- Fresh investments can be in a combination of dynamic bond funds and income funds with a bias for the latter. We have been suggesting this for the past few months. However, many investors, attracted by the high returns in long duration funds (gilts especially), have entered them just before correction. With yields moving up, income funds will have options to pick instruments with higher coupon rate and will hence benefit more than they did few months ago

- For those wanting to play the interest rate game, dynamic bond funds are a less painful way to participate than gilt funds. Use the SIP route to deploy funds in this category now. But do note that their returns won’t be as attractive as they looked in the past year; And over a 3-5-year period, dynamic bond fund returns will likely be closer to income funds.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Thank you. Very well explained. Great service.

Thank you. Very well explained. Great service.

Birla sunlife dynamic bond fund- Is it a bond fund or income fund ?

It is a dynamic bond fund by nature but when interest rates decline, it will reduce its maturity and at such times it will seem like an income fund.

Great piece, thanks!

Is it right time to invest in debt funds, if yes please suggest some good debt funds for a holding period of 3-5 years.

also let me know if i should take SIP route or Lump sum amount..

Naveen, You can invest in debt funds anytime. What category to choose will depend on your time frame and requirement. Please get in touch with us through your FundsIndia account for any specific suggestions from us. thanks, Vidya

hi,

I have invested in ICICI Prudential Long Term Plan, now it is 2% down. should I wait for year to turn positive or I should do SIP from this fund to another

Please stay invested for the time frame you intended to. There is nothing wrong with the fund. It is about yields moving up. thanks, Vidya

hi,

I have invested in ICICI Prudential Long Term Plan, now it is 2% down. should I wait for year to turn positive or I should do SIP from this fund to another

Please stay invested for the time frame you intended to. There is nothing wrong with the fund. It is about yields moving up. thanks, Vidya

Is it right time to invest in debt funds, if yes please suggest some good debt funds for a holding period of 3-5 years.

also let me know if i should take SIP route or Lump sum amount..

Naveen, You can invest in debt funds anytime. What category to choose will depend on your time frame and requirement. Please get in touch with us through your FundsIndia account for any specific suggestions from us. thanks, Vidya

Birla sunlife dynamic bond fund- Is it a bond fund or income fund ?

It is a dynamic bond fund by nature but when interest rates decline, it will reduce its maturity and at such times it will seem like an income fund.

Great piece, thanks!