Anoop Bhaskar CIO, UTI Mutual is candid not only in his opinion of the equity market but also when it comes to the market opportunities that he may have overlooked. In this interview with FundsIndia.com, Anoop provides his perspective on where we are today in terms of valuations and also the strategy for their premium fund UTI Opportunities.

Anoop Bhaskar CIO, UTI Mutual is candid not only in his opinion of the equity market but also when it comes to the market opportunities that he may have overlooked. In this interview with FundsIndia.com, Anoop provides his perspective on where we are today in terms of valuations and also the strategy for their premium fund UTI Opportunities.

Excerpts:

With the market looking for growth in the last 18 months, growth stories are now at a premium. Is that premium justified?

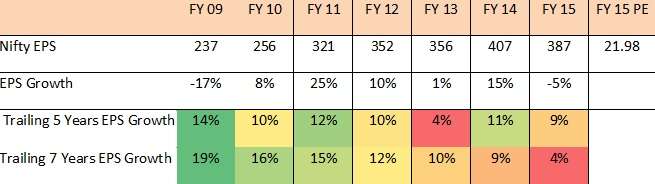

Nifty earnings growth for FY 14 and FY-15 have been way below its 10 and 15 year averages. As a result, investors continue to repose faith in companies reporting growth rates higher than the market, even though the trajectory of their growth appears to have flattened. Valuations, as we have seen before, by themselves will not lead to a correction.

When will such premium appear to be untenable? While it is difficult to pin point a time period when the high growth stocks correct, the advent of sustained economic recovery should lead to earnings growth getting more uniformly distributed.

Such a scenario should herald a correction for high growth stocks. Whether this correction is time or price led, would be interesting to observe in the future.

When do you believe that the broad market will catch up with the earnings growth of the companies that command a premium today?

Over the last three quarters, growth has continued to elude, despite optimistic pronouncement. Given that economic growth peaked in CY-11, it would be four years since the peak levels. During the 1990s, growth peaked in CY-1997 and recovered from CY-2002. Hence, based on past experience, an economic recovery should be around the corner.

Will valuations become more realistic then?

Valuations could become reasonable, either through a price correction or an earnings recovery. Most investors would prefer the second! There are a few examples of companies, where growth issues have led to a sharp de-rating – Sun Pharmaceuticals and Lupin. The impact of a poor quarterly earnings has been reflected in the sharp price movements in both these companies. Thus, the belief that a portfolio of high quality companies would be the insuranceagainst high valuations, may need to be revisited.

How different is UTI Opportunities’ strategy in the ‘search for growth’ story? Has that meant consciously losing on some seemingly good/short-term opportunities?

Our focus has been to identify companies with strong medium-term prospects of 2-4 years on the one hand, and valuations on the other. We have been willing to overlook near term hiccups in quarterly earnings, with the objective of generating longer term outperformance. This mind set has resulted in us overlooking some of the stocks which were and have remained expensive relative to their peers.

Unfortunately, such stocks have been amongst the better performing stocks over the last eighteen months.

UTI Opportunities has been large cap focused for several years now. In the minimal midcaps that you do take exposure to, what is your strategy?

Our approach to stock selection, irrespective of the market cap or size remains consistent. We would like to identify companies which have reasonably consistent track record over the last five years, should be able to generate operating cash flow, reduce debt from internal accruals rather than through frequent equity issuances coupled with moderate valuation mutiples.

Within this sub set of companies, we would prefer those, where our analysts are confident that earnings growth could be stronger than the consensus. We are willing to overlook a couple of quarterly earnings which may be below par, if valuations have come down from the past peak levels.

When do you expect a clear momentum in earnings and how is UTI Opportunities positioned in this regard?

Our belief has been that consumption will be the driver of revival in economic growth over the next few quarters. Automobiles, as a representative of the same, are best placed to benefit from lower raw material costs as well as an improvement in volume growth. Not surprisingly, this sector has the largest overweight to its benchmark weight in our portfolio. Also given the tepid global situation, unlike 2003-08 period when global growth was booming, economic recovery in India could be more gradual than what the expectations were earlier, especially during May 2014 post the election result results.