As Pramerica Mutual launches its open-ended mid-cap fund, FundsIndia.com has a Q&A with BP Singh, Executive Director & CIO-Equities, Pramerica Mutual, on how to identify a turnaround and why investors should invest in mid-caps now.

Excerpts:

Is this one of the most painful periods in the Indian economy or we have seen such prolonged cycles earlier?

We have seen such a period of slowdown from the year 1997 to the year 2002. In this span, GDP growth was sluggish and markets performed poorly in tandem. What followed was a recovery starting from the year 2003 as the preceding years of pain had resulted in low investments in new capacities tilting the balance in favour of demand against limited supply.

We are at similar point in the cycle where addition of new capacities has paused for some time now and the situation is turning in favour of the industry.

How does one identify a turnaround in economic and market cycle?

In a recovery phase, few players see improvement in margins as the industry goes through pain followed by a shake-out that results in consolidation of market share or capacities. The survivors benefit from better pricing power which drives P/E expansion.

This lasts till the prices reach a level which makes it viable for fresh investments in capacities following which we hit a peak in the cycle when these are commissioned resulting in waning of the price-making position of the industry.

Currently, we believe consolidation has begun in most of the sectors laying the foundation for the expansion of PE.

Do you believe we are about to see a turnaround, albeit at its early stages?

We do believe that we are at the cusp of a turnaround and the recent consolidation seen in cement and the shake-out seen in aviation and telecom validates our view. These events were a consequence of rising costs making inefficient capacities unviable.

Also, the high leverage that was incurred to set up these capacities drove these players to offload to stronger entities at lower valuations resulting in consolidation at lower costs and as a result, the return of pricing power to the industry. We notice similar cost pressures in most of the sectors and expect such events to lead the entire economy to recovery path.

Are macro indicators providing any signs of improvement?

The private sector capital formation as a percentage of GDP has dipped significantly over the last few years. This lack of addition in capacities is in line with our view that with no new capacity being added and the existing ones changing hands at lower costs will result in companies becoming more profitable. It may be noted that macro indicators such as GDP growth are more of lag indicators.

Do we have a 5-year story ahead after 5 years of going nowhere in the markets or the pent-up move may happen faster?

Here we would like to draw a distinction between recovery in markets and the economy. While we believe the recovery in economy with job creation, new fixed capital formation will be relatively slower, the recovery in markets has always preceded the recovery in the economy and is likely to be much faster.

Economy goes through consolidation process before it recovers and we are currently going through that process. However, market anticipates the opportunity and starts discounting that in advance. Keeping this in mind we can say that market is now anticipating consolidation in the economy and this is likely to takes us into a long term recovery may be lasting 4 to 5 years.

Why did you choose to launch a mid-cap fund now?

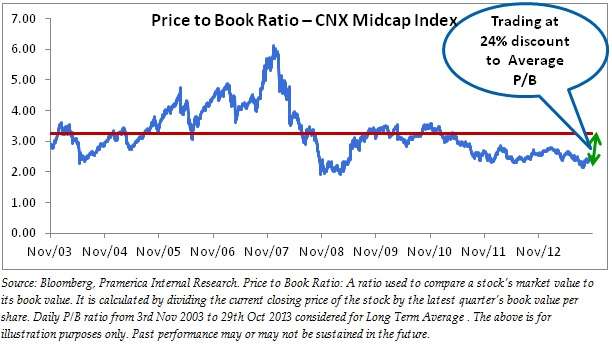

Mid-caps are trading at a discount to their historical valuations on account of the pressures seen in the economy. These have resulted in margin compression and hence a de-rating of these stocks.

However, we have observed that in the recovery mode, earnings of midcap companies pick up substantially faster driving their outperformance. Hence, given the context stated earlier, with respect to our view about the current juncture of the market/economic cycle, we are of the view that about 40% of the companies in the space will survive the current economic turmoil.

These companies will stand to benefit from gain in market share that will in turn drive earnings and multiple expansion, will be able to deliver relatively superior return. The current valuations also provide a high margin of safety to invest in this space.

The divergence in valuations between large caps and mid caps is too high. Do you think the markets have exaggerated the risks or the valuation difference is justified?

It is justified, as midcaps tend to suffer more in a downturn and see margins contract which leads to their de-rating. However, midcaps also rebound more sharply as the cycle turns around as both earnings and multiples expand. This is the opportunity we see now and hence are launching the mid cap fund.

Midcap funds have traditionally fallen out of the performance chart in phases, in the sense, there are no steady performers. How will you ensure that the fund delivers steadily?

Different industries benefit at different points of time in a cycle and mid-cap funds look to invest in those that are the stars of that cycle. Unfortunately, we have seen in the past that many of these companies raised capital aggressively and diversified into unrelated businesses leveraging on the strength of a healthy business to enter into an entirely disparate one reflecting poor capital employment decisions.

We will be cautious of such behavior and invest in businesses that look to be leaders in their niches. Our effort will be to ride a stock which is a leader in the sector which is coming out of bear phase.

Are you going to taken focused sector/stock bets or are you likely to stick around the benchmark?

We will make investments based on the underlying fundamentals of a stock looking for companies that are low on leverage and have displayed prudent capital employment in the past and hence are better placed to take advantage of consolidation in the industry.

Are you going to have a value focus in your picks in the midcap fund?

Yes, we will look to invest in stocks at attractive valuations and will take capitulations in the market as opportunities to deploy funds. To this end, we will continue to bring cost down by averaging the stock at regular interval rather than investing at once.

This is with the view that we want to capture the upside resulting from both, margin expansion-driven earnings growth and the resultant multiple rerating.

IMPORTANT DISCLOSURE:

This note is for information purpose only. This Document and the information do not constitute a distribution, an endorsement, an offer to buy or sell or the solicitation of an offer to buy or sell any securities or any other financial products / investment products of the companies or issuers (collectively “Products”) mentioned in this Document or an attempt to influence the opinion or behavior of the Investors/Recipients. This Document has been prepared on the basis of information, which may be already available in publicly accessible media or developed through internal analysis of Pramerica Asset Managers Private Limited (‘the AMC’). The views incorporated in this document are solely to enhance the transparency and should not be treated as an endorsement in any manner whatsoever. Under no circumstances should any information or any part of it be copied, reproduced or redistributed. The AMC/Pramerica Mutual Fund may or may not have a position in or with respect to the Products mentioned. Except for the historical information contained herein, statements in this publication, which contain words or phrases such as ‘will’, ‘would’, ‘may’, ‘will’ etc., and similar expressions or variations of such expressions may constitute ‘forward-looking statements’. These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the forward-looking statements. The AMC undertakes no obligation to update forward-looking statements to reflect events or circumstances after the date thereof. The above forecasts are based on our current view of the likely course of markets over the period nominated. The above forecasts are made as indications only and not as the basis for investment decisions by readers of this material. Persons wishing to make such decisions should obtain their own professional advice. The AMC, its affiliates/associates, their directors, employees, representatives or agents shall not be liable or responsible, in any manner whatsoever, to any Investor/Recipient or any other person/entity, for the performance/profitability/operations of the Products or any investments in the Products including any and all direct, special, punitive, indirect, or consequential damages (including lost profits), even if notified of the possibility of such damages.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.