2018 was a year that probably gave you glimpses of the rough side of equity and debt markets. The bad news is that you have probably not seen the end of this rough ride. But if all factors sit well, 2019 might well end as a high-adrenaline joyride, especially for equities.

Last month, we wrote a recap of the past year that included what our outlook was for 2018 and how market behaved along those lines. You can read it here.

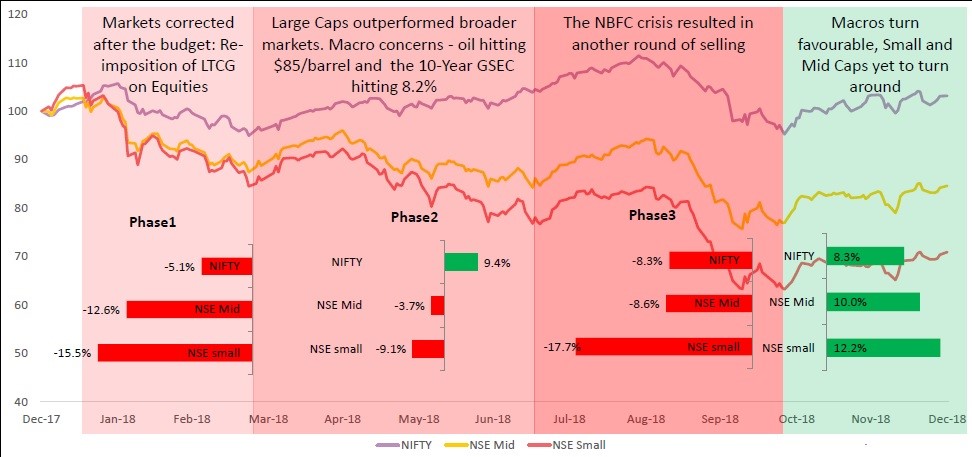

To put the outlook for this year in perspective, a quick look at the main events of 2018 is needed. Here’s a graph that captures the essence of 2018 events.

Source: IDFC MF

Equity market outlook

While crude oil, the wild swing in the 10-year gilt and the NBFC liquidity concerns were predominant reasons for the 2018 volatility, an underlying but persistent factor has been the upcoming Central Elections. A pre-election year is often marked by volatility and that has been intensified by other factors playing up in such a year.

So how do we expect this to impact 2019? For this purpose, the year would have to be split into pre-election and post-election phases.

- The pre-election phase can be expected to exhibit bouts of volatility reacting to local political sentiments leading up to elections and any global factors in the form of a rate hike in the US.

- The post-election period will once again see focus on fundamentals – earnings and macro conditions. With a prolonged period of volatility and macros continuing to improve, the second half may well see the market catch up where it left in end 2017. In simple words – subject to risks (mentioned later), equity markets, like all other election years might end up with gains that it could not manage in 2018.

Let us see what the factors you need to be aware of right away; even as the market may take cognisance only post elections.

Earnings and macro to see a shift

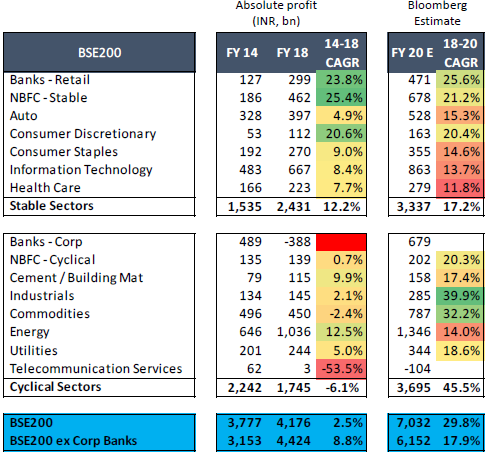

We have been writing about improvement in earnings in recent quarters but if you see the BSE 200 earnings growth, since FY-14 (from the last pre-election year) to FY-18, it was a mere 2.5% CAGR. This came on the back of cyclicals – banks, cement, industrials, energy, commodities, utilities and telecom declining in profits over these 4 years. The defensives or staples on the other hand outperformed. While cyclicals might seem quite muted at this stage, there are reasons to believe that they may see their next phase of growth.

For one, there are signs of NPAs peaking and some banks already seeing a reduction in the pace of NPA addition. Two, capacity utilisation data from RBI suggests an increase to 76.1% in the second quarter ending September 2018 from 73.1% in the first quarter. Three, one of the key high frequency indicators, eight core industries, saw a 13-month high of 6.8% growth in November (over a year ago), aided by double-digit growth in cement and steel. The Bloomberg estimate given below appears to factor many of these improvements. Even assuming much of the estimate is not achieved, a low base for cyclicals can well mean that even a small improvement can translate into good growth. And given the stock correction in these segments in 2018, valuations augur well for a rally, if supported by earnings.

Valuations off highs

The Nifty 50 price earnings ratio is off its year-ago levels and importantly the price to book is now marginally below long-term averages. Besides, the market cap to GDP ratio is at 71% from 93% a year ago. This basically means the correction has removed some froth, even as the healthy GDP growth has ensured there is more left on the table for the equity market.

Support from domestic inflow

A year like 2018, when foreign investors were net sellers, could have been worse but for support from domestic investors. However, this too has been flagging in recent months. While it is not easy to guess what foreign investors will do, domestic retail investors (as indicated by MF equity inflows) have traditionally pumped in more money post elections, compared with 6 months preceding the election period. This, irrespective of what the election mandate was. Essentially, it appears to suggest they just like certainty before deploying their money. Hence, some renewed support on this front, post-election, could provide some fillip as well.

Risks to equity outlook

The last few years’ global growth has been fuelled by the US. But recent forecasts by analysts, including World Bank’s, suggest a global slowdown (including in US), citing multiple factors from trade tensions to financial market instability to currency challenges in emerging markets. While this need not necessarily impact local fundamentals, it can certainly trigger risk sentiments. Crude too, remains a game changer.

The outcome of the elections will also influence Indian markets. While a new government might see markets reacting a bit but settling down, the worst scenario would be that of a lack of clear mandate. In such a scenario, a full-fledged correction cannot be ruled out. But then, remember, that would mean bargain buying in the market as fundamentals don’t change overnight even if seats are traded!

Your Equity investing strategy

- While largecaps look better from the perspective of stability, we think multitap funds make more sense from the current market perspective. Given the correction in mid and smallcap stocks, these funds provide the needed entry points into this space without having to experience too much volatility.

- If you hold mid and small cap funds and they account for less than 20% of your portfolio, this could be a good time to add. While we advocated caution in this segment last year, we believe this is the year to accumulate. You can consider lumpsum investments now and follow it up with SIPs for both the multicap funds and mid and small-cap funds.

- If the cyclical shift in sectors is to play out this year, then it will be cyclicals all the way for the next few years. Mixing it with our defensive strategy (to reduce the present volatility and risk of election outcome) using our election portfolio can yield results for those looking for superior returns to diversified funds. Investments in these can be lumpsum.

- For those of you still wanting to be cautious on equity and not wanting to allocate unless supported by fundamentals, our new SmartSIP portfolio will provide you the right dynamic allocation in the present volatility.

Debt outlook

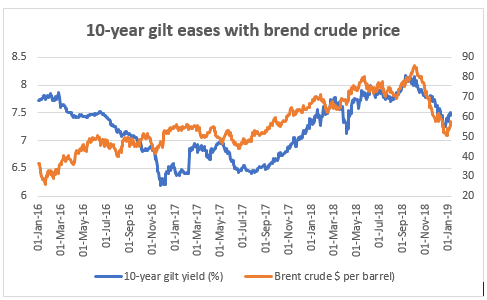

The later part of 2017 to September 2018 saw the worst kind of volatility in the 10-year gilt (government security). Thanks to rising crude and depreciating rupee, gilt yields crossed the 8% mark in September 2018, denting debt fund returns. But with the easing of crude price to less than $60 a barrel now, things seem less painful.

Our outlook for debt in 2019 is as follows:

- Inflation signals remaining the same, we may enter a rate pause scenario now.

- A possible rate cut in the later part of the year cannot be ruled out if global cues are not negative and inflation remains benign.

- The abnormally high rates in short term debt may ease.

- Credit risks may remain even as liquidity-related issues reduce. It will be a good while before NBFCs regain charm.

- While the quick easing of gilts post September may provide signals to play the duration, external factors (global rates, crude oil) and internal factors (like fiscal deficit) suggest it may be prudent to stay away as there are adequate returns to be made in accrual.

Risks to a neutral or rate cut stance

- At 15.1%, bank credit growth for December 2018 (over a year) far outpaced the deposit growth of 9.4%. With NBFCs ceding more ground to banks, the latter’s ability to lend will come only from higher deposit rates. And that builds an obstruction for a rate cut.

- Rate hike by the US Federal Reserve, besides fiscal slippages locally will make it harder to continue a neutral rate stance. Crude oil remains yet another constant source of risk.

Your 2019 debt strategy

- If a combination of liquid and ultra short-term/low duration funds yields the best returns in 2018, this may be a year to shift to short-term and medium duration high quality accrual funds, especially in place of 2-3-year bank FDs.

- The average yield to maturity for short duration funds, at 8.8%, and for medium duration and corporate bond funds, at 9.35%, would make early 2019 among the best periods to enter debt funds.

- For those who held dynamic bond funds and took a hit, wait till you complete at least 3 years. The current easing may help recover much of the returns you lost.