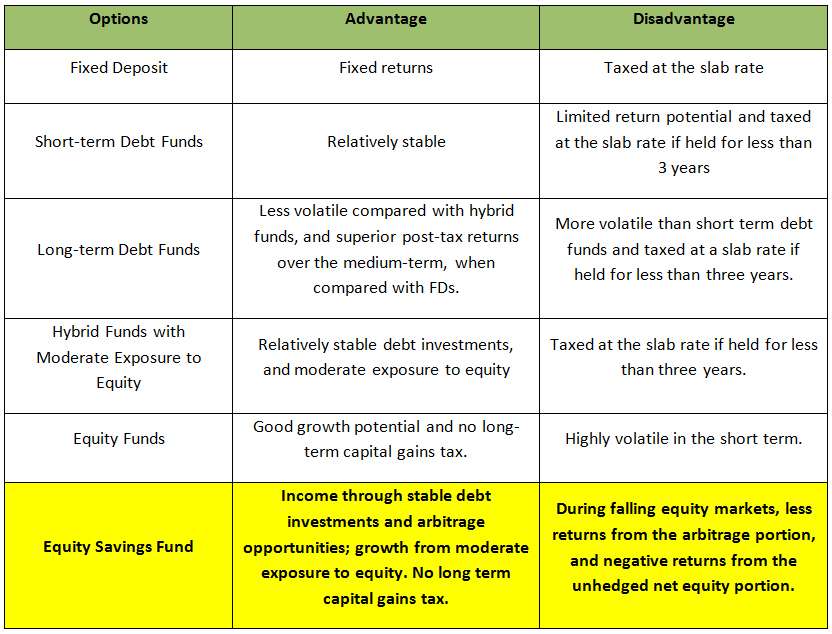

Equity savings funds are a new variant in the equity mutual fund basket. Exposure to equity, a part of which is hedged, and then some debt, and you have this new fund category. Before going into this product’s details, let’s understand the reason for this new category coming into the mutual fund universe.

In the last Budget, the government increased the holding period for debt funds to three years in order to get indexation benefits. Else, you would be taxed at your slab rate. That means debt and debt-oriented funds such as Monthly Income Plans (MIPs) would have the same tax treatment as Fixed Deposits (FDs) for holdings up to three years.

Equity savings funds, as a category, came into being to provide MIP-like returns, while trying to address the concerns of this set of investors.

The Category

Equity savings funds aim to generate returns from equities, arbitrage trades, and fixed income securities. To retain equity taxation, funds will restrict the fixed income (debt) exposure to 35 percent. Besides, to reduce volatility and hedge the portfolio, these funds actively use derivative strategies.

Still, some amount of equity is unhedged (pure equity cash market) to prop up the returns of the portfolio. The equity and the derivative exposure is considered as ‘equity’ allocation and hence, these categories of funds are treated as equity funds. The unhedged equity exposure typically ranges from 15 percent to 40 percent, and the rest of the portfolio is hedged to gain from arbitrage opportunities.

Before going into what these funds are, and when they will suit you, it is first important to know that these funds cannot build long-term wealth efficiently like pure equity funds. To this extent, one should not view these in the same light as equity for long-term portfolios. What equity savings funds offer is stability and tax efficiency; the latter when compared with debt.

These funds are suitable for those looking for some equity exposure but do not have a very long time frame. They suit those with limited risk appetite and looking for less uncertainty in returns. Many of these funds seek to provide regular dividend income although they are not mandated to do so.

They are certainly not substitutes for pure equity funds, especially for long-term portfolios, and fit those with a 2-3 year time frame who want tax benefits that are not available in debt-oriented funds for such a short time period.

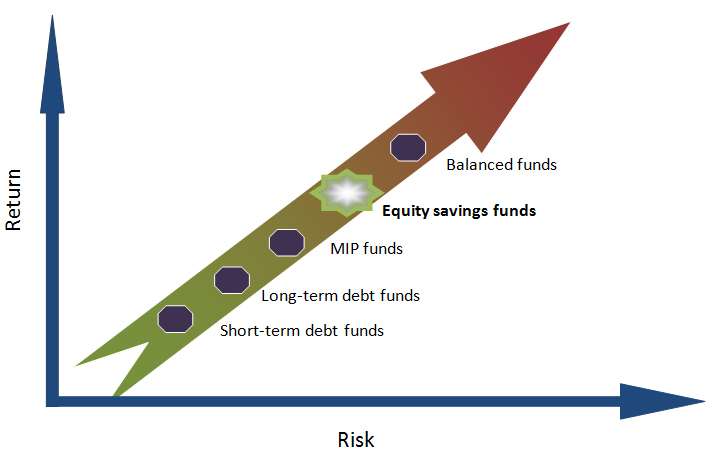

Positioning

If you plot the fund categories on a risk-return axis, equity savings funds are positioned between MIP funds and balanced funds. They stand a notch higher than MIP / debt-oriented funds, and one notch lower than balanced funds in their risk-return proposition.

How does arbitrage generate returns?

Arbitrage funds look to exploit arbitrage opportunities (the price difference in securities) in different segments of markets. Fund managers opine that there are significantly higher arbitrage opportunities in a bull market, but lesser during falling or flat markets.

Let us assume that ABC Ltd. trades in the National Stock Exchange (NSE) cash market for Rs. 100, and Rs. 101 (same month futures price) in the futures market. By the end of the month, the future price converges with the cash price. Buying in the cash market and selling in the futures market will entitle a gain of 1 percent. If we assume a 0.2 percent brokerage for these transactions, then the net gain is 0.8 percent, or an annualised return of 9.6 percent.

Pure arbitrage funds hedge their cash positions entirely and hence, the return from a market movement (from unhedged equity) is ruled out. In equity savings funds, there is a good chunk of unhedged equity that can generate returns higher than arbitrage funds. To this extent, equity savings funds carry far higher risk and higher return potential than arbitrage funds.

Category Performance

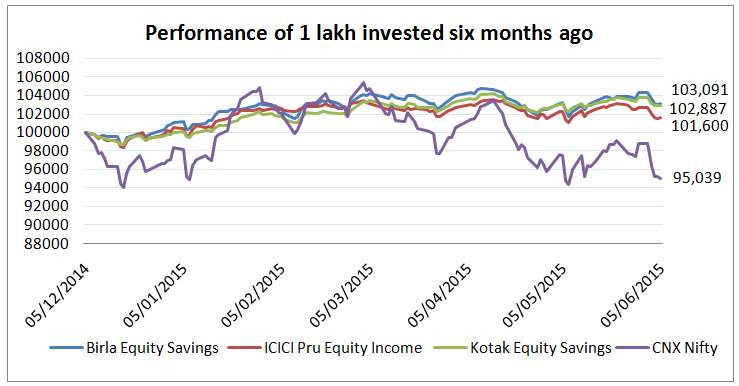

Given that many of the funds in this category are of recent origin, they do not have much of a track record. But when reviewing their performance thus far, it appears that they have performed well in relation to the CNX Nifty. In the below chart, the Nifty has fallen by around 5 percent, while equity savings funds delivered positive returns that range from 1.6 percent to 3 percent in the last six months. Their arbitrage component and debt allocation clearly help these funds in down markets.

The unhedged equity portion differs from fund to fund, and also varies in different time periods. Higher the unhedged portion (net equity exposure), higher the volatility. Hence, you need to check this information before investing in these schemes. For instance, Edelweiss Absolute Returns also follows a similar strategy, but can take a much higher unhedged equity exposure (we have therefore, not brought the fund under this category).

| Scheme | Unhedged portion |

| Birla Sun Life Equity Savings Fund – Reg. – Growth | 20% – 45% |

| ICICI Prudential Equity Income Fund – Reg. – Growth | 20% – 40% |

| Kotak Equity Savings Fund – Reg. – Growth | 15% – 25% |

Equity savings funds – How they stack up

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Can these funds be used to save emergency funds?

Hi Arun,

These funds are not suitable for keeping the emergency funds. Keep the funds in Liquid and Ultra short term funds.

Thanks

Sathya

Who should consider investing in this class of funds?

Moderate risk profile investors with an investment horizon of 2-3 years. And also who looks for moderate returns with equity taxation.

Thanks

Sathya

can i park my retirement savings in these funds and do swp for monthly income. Will it give higher return and capital safety?

pl reply

Joseph

joesouza14@gmail.com

Hi Joseph, Sorry about the delayed reply. Can there be capital safety and high return? 🙂 The returns will be middle order and will be lower risk than equity but not nil risk.

thanks

Vidya

Hi Vidya,

Can I suggest me one small and mid cap fund and one multicap fund for long term investment.

Hi Krishna,

Fund suggestions would depend on the other funds you hold and your risk level in addition to being long-term. For example, if you already have mid-cap funds, then adding another one may increase your risk too much. Please route portfolio-specific queries through your advisor (Talk to your advisor feature on your MF dashboard). This forum is for discussion only.

Thanks,

Bhavana

can i park my retirement savings in these funds and do swp for monthly income. Will it give higher return and capital safety?

pl reply

Joseph

joesouza14@gmail.com

Hi Joseph, Sorry about the delayed reply. Can there be capital safety and high return? 🙂 The returns will be middle order and will be lower risk than equity but not nil risk.

thanks

Vidya

Hi Vidya,

Can I suggest me one small and mid cap fund and one multicap fund for long term investment.

Hi Krishna,

Fund suggestions would depend on the other funds you hold and your risk level in addition to being long-term. For example, if you already have mid-cap funds, then adding another one may increase your risk too much. Please route portfolio-specific queries through your advisor (Talk to your advisor feature on your MF dashboard). This forum is for discussion only.

Thanks,

Bhavana

For a person of 53 Yr 6M, and to retire in 6 years, which MF (like Equity savings )Plan are best, which particular ES are good for ex to invest say 5K per month ( to be divided in to 2 or 23 funds) and through SIP for 5 years, to get good returns than bank RD.

Hello,

Apologies for the delay in reply. Equity savings funds are good options if you want superior return than bank FD. Debt funds will also deliver higher returns than bank FD and they are more tax-efficient as well. So it depends on how much risk you are willing to take. Equity savings funds are higher risk and more volatile than pure debt funds, but they can deliver higher returns. They need longer holding periods of around 2-3 years to deliver. If your goal is to just to earn higher returns and you are willing to take some risk, then equity savings funds are an option. Please note that each fund has its own range of un-hedged and hedged equity and debt (equity savings funds are hybrid funds). So you will need to check with the fund to understand how much risk it takes.

Thanks,

Bhavana

For a person of 53 Yr 6M, and to retire in 6 years, which MF (like Equity savings )Plan are best, which particular ES are good for ex to invest say 5K per month ( to be divided in to 2 or 23 funds) and through SIP for 5 years, to get good returns than bank RD.

Hello,

Apologies for the delay in reply. Equity savings funds are good options if you want superior return than bank FD. Debt funds will also deliver higher returns than bank FD and they are more tax-efficient as well. So it depends on how much risk you are willing to take. Equity savings funds are higher risk and more volatile than pure debt funds, but they can deliver higher returns. They need longer holding periods of around 2-3 years to deliver. If your goal is to just to earn higher returns and you are willing to take some risk, then equity savings funds are an option. Please note that each fund has its own range of un-hedged and hedged equity and debt (equity savings funds are hybrid funds). So you will need to check with the fund to understand how much risk it takes.

Thanks,

Bhavana

Who should consider investing in this class of funds?

Moderate risk profile investors with an investment horizon of 2-3 years. And also who looks for moderate returns with equity taxation.

Thanks

Sathya

Can these funds be used to save emergency funds?

Hi Arun,

These funds are not suitable for keeping the emergency funds. Keep the funds in Liquid and Ultra short term funds.

Thanks

Sathya