Dependable quality, old world charm

Franklin India Prima Plus belongs to the old school of investing – steady and consistent in its performance. If you are the kind scouting for flashy returns, this fund would not have entered your radar.

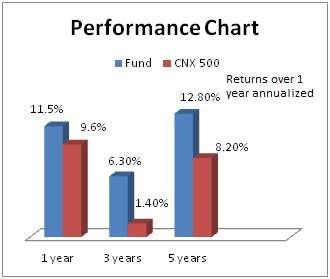

Launched in 1994 and tested through several market ebbs and flows, Franklin India Prima Plus is a good addition to a long-term portfolio of 5-15 years for investors with medium risk appetite. Its 5-year annual return of 12.8% is a good 5 percentage points more than its benchmark CNX 500.

Suitability

Franklin India Prima Plus is predominantly a large-cap fund with a little bit of midcaps to help up the return potential. It is therefore suitable for less-aggressive investors. Its track record of containing declines reasonably well also points to the fund being a good fit for investors with moderate risk appetite.

Given the volatile market conditions, any investing in equities is best done through SIPs and Franklin India Prima Plus will be no exception to this rule. But if you have a time frame of not less than 10 years and do have the money to spare, then lump sum investing may be a good idea at this juncture, given that both earnings and economic factors are at perhaps at their respective low points.

Performance

Franklin India Prima Plus has managed to stay in the top quartile of the performance chart consistently. But the fund did not make it to the toppers’ charts in recent years. Still, you’ll probably find the fund in the top ten of the diversified fund category over 7- and 10-year periods.

The fund’s ability to contain declines was well-demonstrated in 2008 as well as in 2011, if we take the recent years’ performance.

In 2008, the fund’s NAV fell 48% lesser than the 52% average fall seen in equity funds as well as broad indices. In 2011 too, it contained declines to just 16%; that was better than the category’s fall of 24%.

The fund’s ability to contain declines stems from two factors: one, its predominant exposure to large caps and two more important reason, its call on equities based on valuations. Now, this may sound strange, given that Franklin India seeks to invest in ‘high growth’ stocks that generate wealth.

High growth companies are defined by the fund as those that generate higher return on capital then their cost of capital. While stocks of high growth companies can also swing more with the markets, Franklin India Prima Plus has effectively contained this by taking good valuations calls.

The fund’s exposure to equities is typically high when markets are beaten down – the end of 2008 and 2011 being cases in point. By buying when valuations are attractive, the fund’s is in a better position to handle downsides from the highs (having bought stocks when they were low).

Similarly, valuation calls are taken when sectors become expensive. The 4% exposure to FMCG that the fund held a year ago has been eased over the course of the last one year, what with valuations steadily climbing northward for stocks in the space.

Portfolio

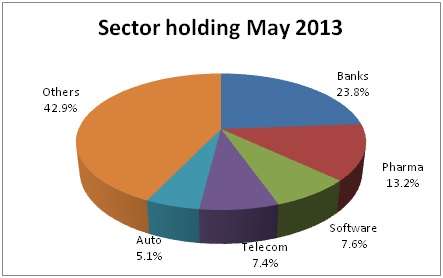

Franklin India Prima Plus has stocked its portfolio with growth sectors such as banks, telecom, auto and cement even as it holds IT and pharma.

Although pharma is perceived as a defensive space, the fund has picked high-growth stocks in the sector such as Dr Reddy’s Laboratories and IPCA Laboratories and thus reaped rich benefits.

Fund manager Anand Radhakrishnan also appears to have plenty of conviction in some of his picks; holding as he does, the market-neglected blue chip stock Bharti Airtel as his second top holding.

Such calls do lend a shade of contrarian characteristic to this fund. With a low portfolio turnover of about a third, the fund certainly gives time for its stocks to perform.

Hi Vidya

The article is really a good one about the fund insights. I have a question to you.

I had been investing in FT India Blue Chip fund via SIP growth option since 2007.

Do you find any major difference between these two funds, ofcouse India blue chip fund falls on large cap category where as india prima plus funds is in large and mid cap category, apart from this any difference in these funds.

Am in the opinion that if we hold FT India Blue chip doesnt need to have prima plus in one’s portfolio cos both are from same fund house and will have almost same strategy in asset allocation and portfolio of funds. Please advise on the same

Hi Sathish,

Yes you are right. You do not have to hold both the funds. Prima Plus will perhaps give marginally higher returns for the additional risk it takes via midcaps (this is evident when we see the risk-adjusted returns). Bluechip is a pure Bluechip fund and seeks to hold mostly leaders in the respective sectors. Besides, Prima Plus sector strategies and calls are slightly different as it is growth oriented. That means Prima Plus may hold largecaps but not necessarily the very big ones/leaders as often times, the growth in giants will be steady but not too high.

But yes, with both funds having a large-cap bias, and having the same fund manager, there will be duplication is stock holding to a good bit.

tks

Vidya

This is a very good recommendation given the market volatility. http://ddramanathan.blogspot.in/

I have invested in Prima Plus from 2004 to 2012 and i could get an excellent return.these gains are used to buy SIPs in Reliance Equity Opp ( midcap) and Quantum Long Term (large Cap) Funds which are also doing well.

Hello sir,

Thanks for sharing your experience. That appears to be a very good strategy. All the best! tks, vidya

Hi Vidya,

I have a query on a topic not related to the post. I was under the impression that SEBI has totally abolished percentage based entry loads. However, when I was investing through the MF page on Fundsindia, I find the “Commission disclosure” sheet having inputs between 0.5% to 2.0% for several equity schemes. Am I missing something here? or is the data being shown obsolete.

Thanks,

Siva

Hello sir,

Entry loads are indeed abolished. What you probably saw was the disclosure of FundsIndia’s fee received from the mutual fund houses. The expense ratio will cover them. Expense ratio is the total expense (including fund management fee and other admn. charges that a fund house incurs) that a fund house is allowed to charge on each fund for running and managing the fund. One such expense is the distributor fee. Such a fee is paid by the fund house to every distributor of mutual funds. Hope this clarifies. Thanks, Vidya

Thanks for the reply, Vidya. I re-checked the page, it says “Upfront Fee (Percentage)” followed by another column “Trail Commission (Annual Percentage)”. I thought Trail commissions are the only ones left after the abolishing of Entry load. Please correct me if I am wrong.

Hello Sir,

As long as funds are able to keep their expense ratio within the prescribed limit, they may choose to pay upfront and trail commission. Quite a few of them do not pay upfront and pay only trail fee while others pay both.

tks

Vidya

Hi Vidya,

I have a query on a topic not related to the post. I was under the impression that SEBI has totally abolished percentage based entry loads. However, when I was investing through the MF page on Fundsindia, I find the “Commission disclosure” sheet having inputs between 0.5% to 2.0% for several equity schemes. Am I missing something here? or is the data being shown obsolete.

Thanks,

Siva

Hello sir,

Entry loads are indeed abolished. What you probably saw was the disclosure of FundsIndia’s fee received from the mutual fund houses. The expense ratio will cover them. Expense ratio is the total expense (including fund management fee and other admn. charges that a fund house incurs) that a fund house is allowed to charge on each fund for running and managing the fund. One such expense is the distributor fee. Such a fee is paid by the fund house to every distributor of mutual funds. Hope this clarifies. Thanks, Vidya

Thanks for the reply, Vidya. I re-checked the page, it says “Upfront Fee (Percentage)” followed by another column “Trail Commission (Annual Percentage)”. I thought Trail commissions are the only ones left after the abolishing of Entry load. Please correct me if I am wrong.

Hello Sir,

As long as funds are able to keep their expense ratio within the prescribed limit, they may choose to pay upfront and trail commission. Quite a few of them do not pay upfront and pay only trail fee while others pay both.

tks

Vidya

Hi Vidya

I have one question to you. Am holding Fidelity equity fund(L&T equity fund) since inception from 2005 via SIP till now. Do you feel I need to switch to FT prima plus fund(as both are under large and mid cap catetofy). I do have FT blue chip fund via sip since 2007.

What your opinion on the Fidelity equity fund after management changed to L&T? If you feel switch to Prima plus fund is right, then I do have FT blue chip fund from same fund house.

Do I continue with L&T fund for some more time as my horizon is for long term

Please comment

Hello Sathish, L&T Equity, slipped a bit but appears to be gaining footing again. What to hold and what to substitute has to be a portfolio call. If you hold your portfolio of mutual funds with FundsIndia, kindly use the ‘Ask Advisor’ feature to write to us and we will review the portfolio as a whole before recommending any switch. This feature is available to all investors who hold their funds in the portal. thanks, Vidya

Madam,

I can Invest only 2000 rs per month through SIP’s. So, through Funds India I can invest in two mutual funds with SIP of 1000 rs each. Till now i have not invested in any of MF and my age is 20 now. So Please Suggest me Which two funds i have to invest and it can be a large cap or large&mid cap or whatever it may be.

Hi Teja,

We appreciate your motive to start investments at the right age. You can take a look at our Smart Solutions Shubh Aarambh portfolio. It is ideal for beginners, giving small exposure to equities. However, if you feel you can take on pure equities through SIPs right away, pl use our ‘Ask Advisor’ feature (click help tab in your FundsIndia account to see this feature). Mention what is your investment time frame and what is your risk appetite (higher risk means you can take on market falls in the short term) and whether you have any goal in mind. This feature will help us track your queries and respond to you better than through the blog. You can even schedule a call back from our advisors (to discuss your investment plan) using this feature.

Thanks, Vidya

Is there a difference in amount i had to pay when i invest directly through respective mutual fund website and through fundsindia.com .

Yes, Vinod, when you buy directly in each mutual fund website, there is no distributor involved, hence your NAV will be slightly higher. It is called the direct plan. If you buy through distributors such as FundsIndia, the NAV will be slightly lower as it is net of distribution fees paid by AMCs to the distributors. You may wish to read how we vary from direct investing here: https://blog.fundsindia.com/blog/fundsindia-vs-direct-investing

Thanks.

Is there a difference in amount i had to pay when i invest directly through respective mutual fund website and through fundsindia.com .

Yes, Vinod, when you buy directly in each mutual fund website, there is no distributor involved, hence your NAV will be slightly higher. It is called the direct plan. If you buy through distributors such as FundsIndia, the NAV will be slightly lower as it is net of distribution fees paid by AMCs to the distributors. You may wish to read how we vary from direct investing here: https://blog.fundsindia.com/blog/fundsindia-vs-direct-investing

Thanks.

This is a very good recommendation given the market volatility. http://ddramanathan.blogspot.in/

Hi Vidya

The article is really a good one about the fund insights. I have a question to you.

I had been investing in FT India Blue Chip fund via SIP growth option since 2007.

Do you find any major difference between these two funds, ofcouse India blue chip fund falls on large cap category where as india prima plus funds is in large and mid cap category, apart from this any difference in these funds.

Am in the opinion that if we hold FT India Blue chip doesnt need to have prima plus in one’s portfolio cos both are from same fund house and will have almost same strategy in asset allocation and portfolio of funds. Please advise on the same

Hi Sathish,

Yes you are right. You do not have to hold both the funds. Prima Plus will perhaps give marginally higher returns for the additional risk it takes via midcaps (this is evident when we see the risk-adjusted returns). Bluechip is a pure Bluechip fund and seeks to hold mostly leaders in the respective sectors. Besides, Prima Plus sector strategies and calls are slightly different as it is growth oriented. That means Prima Plus may hold largecaps but not necessarily the very big ones/leaders as often times, the growth in giants will be steady but not too high.

But yes, with both funds having a large-cap bias, and having the same fund manager, there will be duplication is stock holding to a good bit.

tks

Vidya

Hi Vidya

I have one question to you. Am holding Fidelity equity fund(L&T equity fund) since inception from 2005 via SIP till now. Do you feel I need to switch to FT prima plus fund(as both are under large and mid cap catetofy). I do have FT blue chip fund via sip since 2007.

What your opinion on the Fidelity equity fund after management changed to L&T? If you feel switch to Prima plus fund is right, then I do have FT blue chip fund from same fund house.

Do I continue with L&T fund for some more time as my horizon is for long term

Please comment

Hello Sathish, L&T Equity, slipped a bit but appears to be gaining footing again. What to hold and what to substitute has to be a portfolio call. If you hold your portfolio of mutual funds with FundsIndia, kindly use the ‘Ask Advisor’ feature to write to us and we will review the portfolio as a whole before recommending any switch. This feature is available to all investors who hold their funds in the portal. thanks, Vidya

I have invested in Prima Plus from 2004 to 2012 and i could get an excellent return.these gains are used to buy SIPs in Reliance Equity Opp ( midcap) and Quantum Long Term (large Cap) Funds which are also doing well.

Hello sir,

Thanks for sharing your experience. That appears to be a very good strategy. All the best! tks, vidya

Madam,

I can Invest only 2000 rs per month through SIP’s. So, through Funds India I can invest in two mutual funds with SIP of 1000 rs each. Till now i have not invested in any of MF and my age is 20 now. So Please Suggest me Which two funds i have to invest and it can be a large cap or large&mid cap or whatever it may be.

Hi Teja,

We appreciate your motive to start investments at the right age. You can take a look at our Smart Solutions Shubh Aarambh portfolio. It is ideal for beginners, giving small exposure to equities. However, if you feel you can take on pure equities through SIPs right away, pl use our ‘Ask Advisor’ feature (click help tab in your FundsIndia account to see this feature). Mention what is your investment time frame and what is your risk appetite (higher risk means you can take on market falls in the short term) and whether you have any goal in mind. This feature will help us track your queries and respond to you better than through the blog. You can even schedule a call back from our advisors (to discuss your investment plan) using this feature.

Thanks, Vidya