A recent release by the RBI had placed bank deposits held by individuals at a whopping Rs 33 lakh crore as of March 2013. That is close to one half of the total deposits lying with banks. Of this, a good 36.5% is held in savings bank account. 56.7% in term deposits and rest in current account.

Yes, the perceived ‘safety’ factor, ‘familiarity’ with your bank and little differentiation in the nature of deposits offered across banks, makes you to stick to these familiar products. While it may be good for you to have a fixed returning component in your portfolio, it’s time you knew that deposits no longer beat inflation.

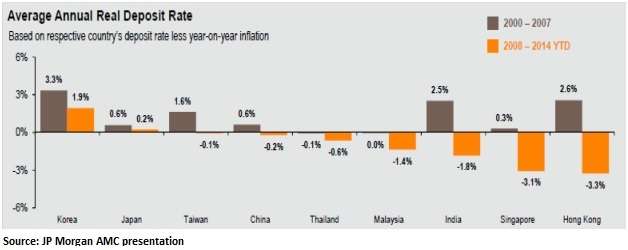

Take a look at the graphics below that shows the ‘real’ deposit rate earned by you between 2008 and 2014. ‘Real rate’ is the return you get after deducting inflation or price rise. The data shows that you would have earned an average negative 1.8% in India if you had been investing in deposits over 2008-14.

Simply put, the interest income from deposits would not have helped you keep pace with rising cost of goods and services.

As a result, you would have to dig into your capital/savings put away for other purposes to meet your goal.That means, lower capital left to generate future income!

But why talk about inflation? Did you know your post-tax returns in deposits themselves are unattractive for you? And the ‘negative’ return could be worse if you considered taxes? A quick calculation will tell you a 9% deposit would only fetch you about 6.3% return if you were in the 30% tax bracket.

Do you know what all this could mean to you?

– At high inflation, investing in deposits alone may not be sufficient to secure your children’s higher education costs.

– Unless your savings rate is very, very high, deposits alone will not suffice to build a retirement kitty. You will spend more from your capital and erode it during your retirement years

Now that too means erosion of capital is it not? So, while you might be under the impression that you lose your capital through so-called ‘risky’ investments like ‘equities’ inflation silently kills you safe investment returns as well.

If you wish to move out of this vicious cycle, you simply have to diversify to better yielding asset classes or bear the pain later. Here are some simple ways to wean yourself away from the culture of merely investing in deposits:

– Start off with simple and smart strategies such as using a liquid fund to park some amount of your surplus, instead of letting it lie in your savings account. Know more about how liquid funds can supplement your savings account here: Liquid funds

– Do not lock all your money in FDs. Read this to know how FDs lack in performance when it comes to post-tax returns.Fixed deposits and income funds. Go for debt funds and if you have some risk appetite, and willing to wait for the long haul go for equity funds.

– Start substituting long-term RDs with some SIPs. SIPs in mutual funds, are not only highly tax efficient but fetch higher returns. Read this to know more: SIP. While the illustration in this article talks about income funds, if you have a 5-year plus horizon, then go some equity funds as well to help deliver far superior returns to deposits.

Hi Vidya,

I would like to know what should be the ideal proportion/ratio of allocation of money among financial assets like Mutual Fund, FMP, Fixed Deposit, Gold (ETF), Equity shares and money lend in the market (at specified interest rate to friends/businessman).

Hello Vivek, Much would depend on your time frame, risk appetite, surplus and existing mix.You may use your FundsIndia account to seek our advice on this (use your help tab and advisory support). thanks, Vidya

Hi Vidya,

I would like to know what should be the ideal proportion/ratio of allocation of money among financial assets like Mutual Fund, FMP, Fixed Deposit, Gold (ETF), Equity shares and money lend in the market (at specified interest rate to friends/businessman).

Hello Vivek, Much would depend on your time frame, risk appetite, surplus and existing mix.You may use your FundsIndia account to seek our advice on this (use your help tab and advisory support). thanks, Vidya