A majority of active large cap funds (read as managed by fund managers) have underperformed their benchmark indices in the last few years.

This leads to the obvious question –

Are passive funds a better and simpler way to play the large cap segment?

We had earlier written on how we were thinking through this question a year back (link).

Here is a quick summary of our earlier view…

What was our earlier view in Dec-19?

Long Term View:

Flexi cap funds with large cap bias which have more flexibility in adding mid and small caps will be a better alternative for pure large cap funds from a longer-term perspective.

In line with our long term view, starting Dec-19, for fresh investments, we had started preferring ‘large cap oriented flexi cap funds’ instead of pure large cap funds.

Short Term View:

Back in Dec-19, we were close to historical lows both in terms of

- Underperformance of Mid cap vs Large cap – indicating midcaps were attractive

- Underperformance of Equal-Weight indices (Nifty 50 & Nifty 100) vs Market Capitalization weighted indices (Nifty 50/ Nifty 100) – indicating extreme polarization where returns were led by top 5-10 stocks

Historically, the relative performance between these segments tends to be cyclical in nature with periods of outperformance followed by underperformance and again followed by outperformance.

Our view was that a trend reversal (read as mean reversion) could happen over the next 1-3 years – leading to

- Mid caps outperforming large caps

- Reduction in Polarization – i.e The concentration of performance only across the top 5-10 stocks will reduce and performance will get more spread out

These are normally periods where active large cap funds outperform their benchmarks given their mid cap exposure of 10-20% in active funds and much more diversified stock exposure.

So while we had avoided incremental investments into large cap funds, for investors already invested in well managed large cap funds (with a consistent track record and proven fund managers), we continued with the exposure in line with the view that active large cap funds may outperform their passive counterparts over the next 1-3 years.

How has this view played out?

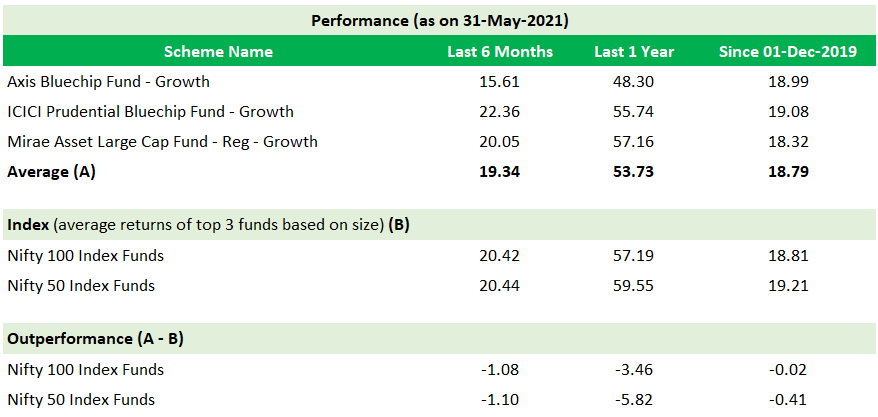

The returns since the time of our call for FUNDS INDIA SELECT list of large cap funds are similar to the passive alternative Nifty 100 Index Fund (in fact slightly lower if we consider Nifty 50 Index Fund).

The key point being – There has not been any large outperformance from active funds as we were expecting.

So the outcome so far is not supporting our short term view.

Given this context, let us revisit our underlying logic which went behind the view and check if it still holds true.

View 1: The concentration of performance only across the top 5-10 stocks will reduce and performance will get more spread out

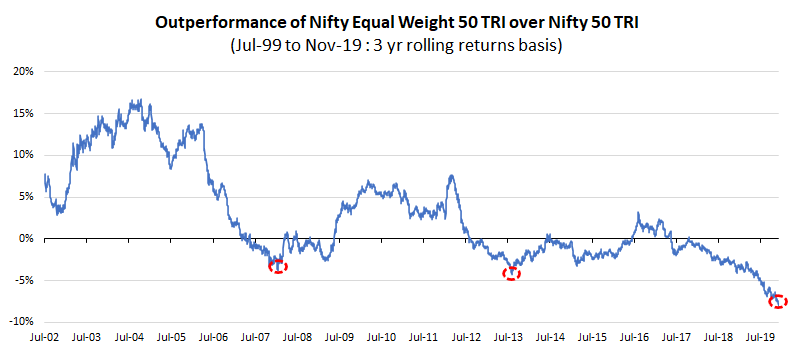

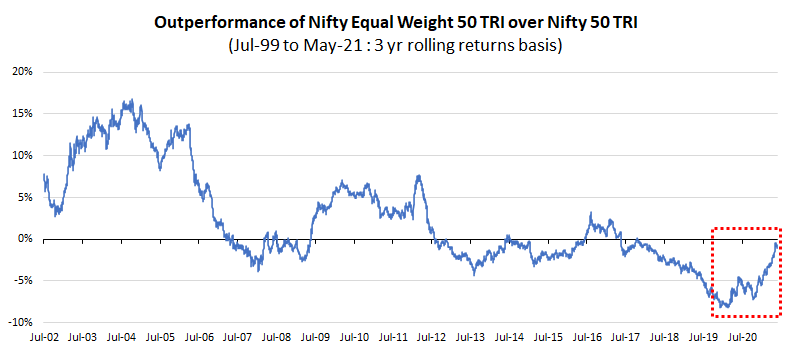

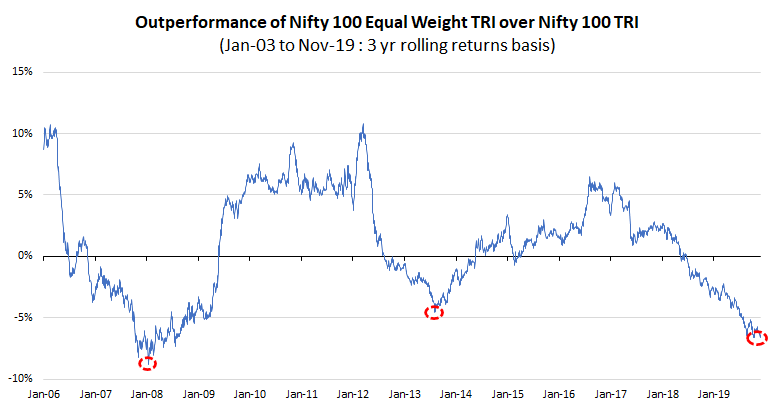

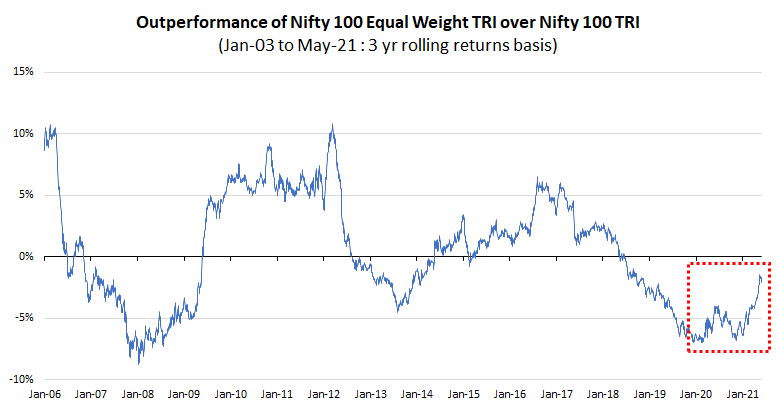

This is captured via the performance differential across equal weighted indices and market cap weighted indices. The 3 Year underperformance of equal weighted index vs market cap weighted index was stark in Dec-19 and our expectation was – ‘this will start to improve’.

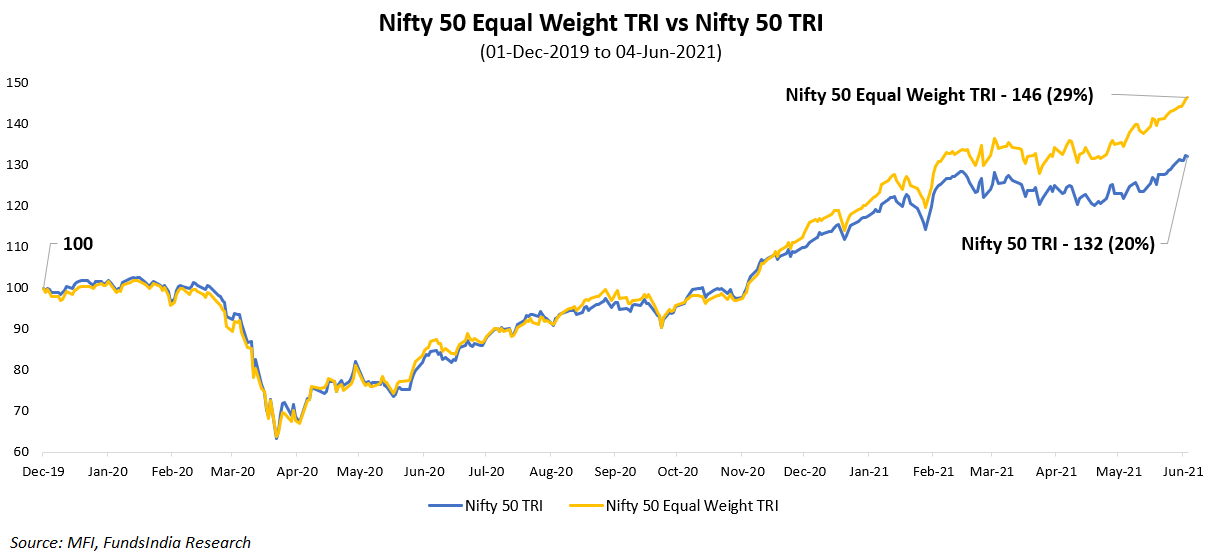

Let us check for Nifty 50 vs Nifty 50 equal weight.

Before: In Dec-19

After: In May-21

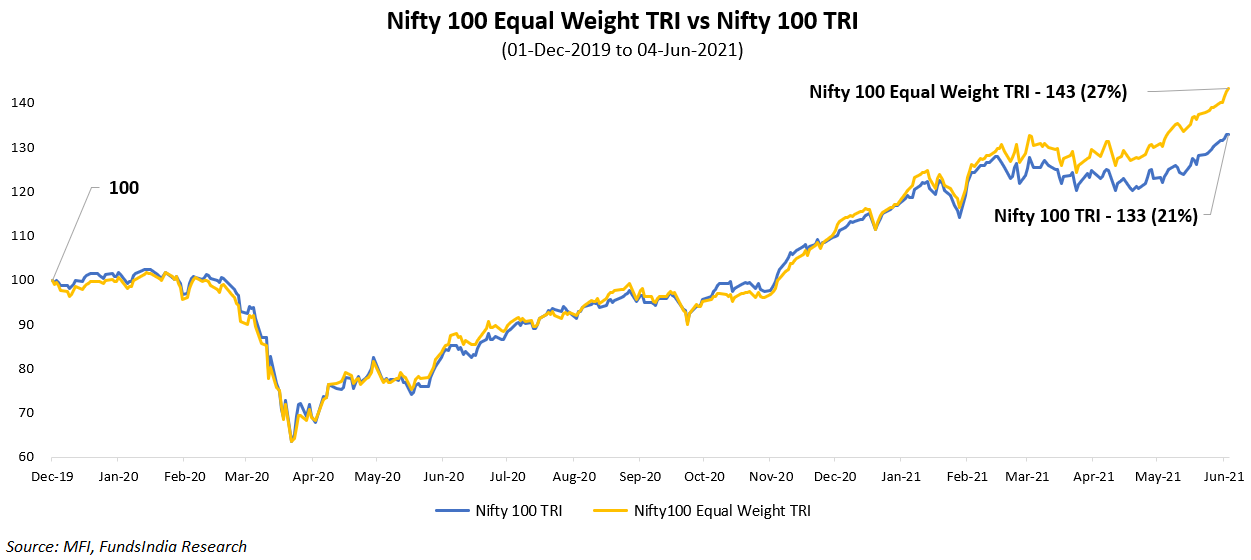

Let us check for Nifty 100 vs Nifty 100 equal weight.

Before: In Dec-19

After: In May-21

So the trend reversal as we expected has started.

Let us also check the actual returns to confirm.

Great! So our view has started to play out as per expectation – the returns are getting more evenly distributed and the polarization of returns in the top 5-10 stocks is reducing.

Let us now check our second view.

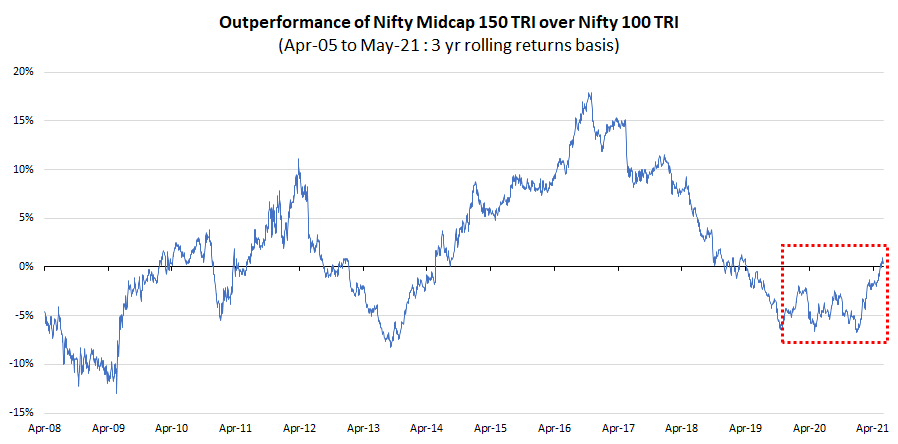

View 2: Mid and Small caps will start to outperform large caps due to mean reversion

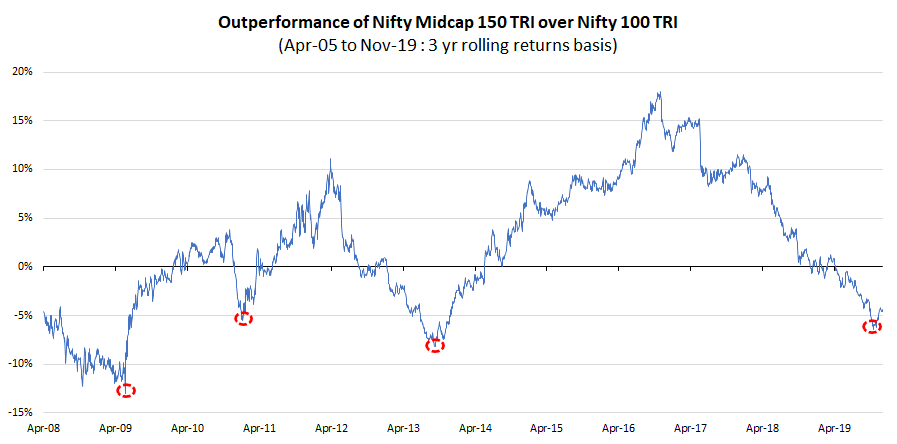

Let us check for Midcap vs Large cap 3 year rolling relative performance

Before: In Dec-19

After: In May-21

So the trend reversal has started as mid caps have started to outperform large caps as expected.

Let us also check the actual returns to confirm.

So our second view has also started to play out as per expectation.

Overall both our views have started playing out with strong trend reversal seen in the last 6 months.

So while active large cap funds are yet to show major signs of outperformance, the environment in our view, is gradually turning favourable for large cap active funds to outperform.

This is also in line with evidence from US markets that ‘Outperformance in Active Strategies have been Cyclical’.

So putting all this together,

We continue with our view that Active Large Cap funds may have a 1-3 year period where the environment is favorable for them to outperform.

But what about our Long Term View (7-10 years)?

Our Long Term View is that, given the 1) Narrow Universe (Top 100 stocks), 2) High Portfolio Overlap with Benchmark and 3) Higher Expense ratio, it is difficult for large cap fund managers to provide meaningful outperformance over the long term.

Even for those funds which build differentiated portfolios and outperform over the long run, behaviorally it will be challenging for investors to stick to these portfolios especially during periods of intermittent underperformance.

While this contradicts our short term view, let me explain our rationale in detail.

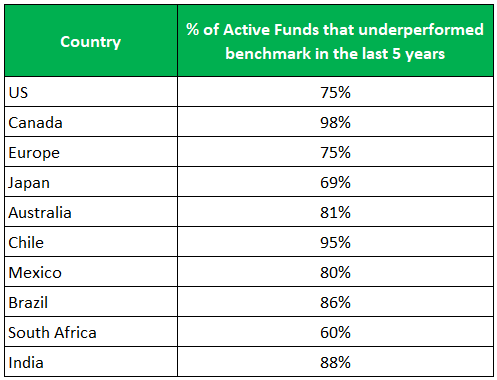

1. Overwhelming Global Evidence

Globally large cap active fund managers are finding it incrementally more difficult to outperform passive index funds.

In the last 5 years, majority of large cap active funds had underperformed their benchmarks.

Here is the startling evidence…

Source: https://us.spindices.com/spiva/#/reports

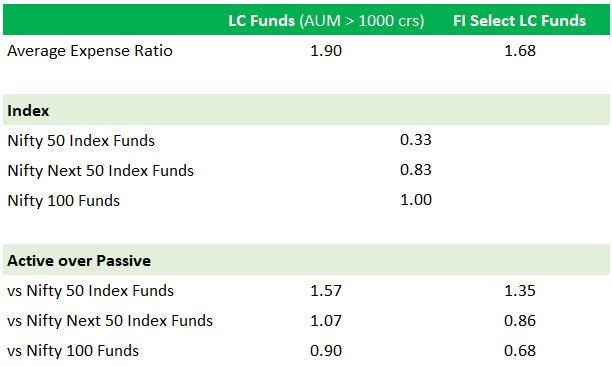

2. Expense Ratio Differential

As seen below there is a differential of around 1-1.5% in expense ratios between active and passive funds. This in essence means that active fund managers have to provide a 2-4% outperformance over the index to end up with a 1-2% actual outperformance accounting for the difference in expense ratios.

3. How different are the portfolios from their passive benchmarks?

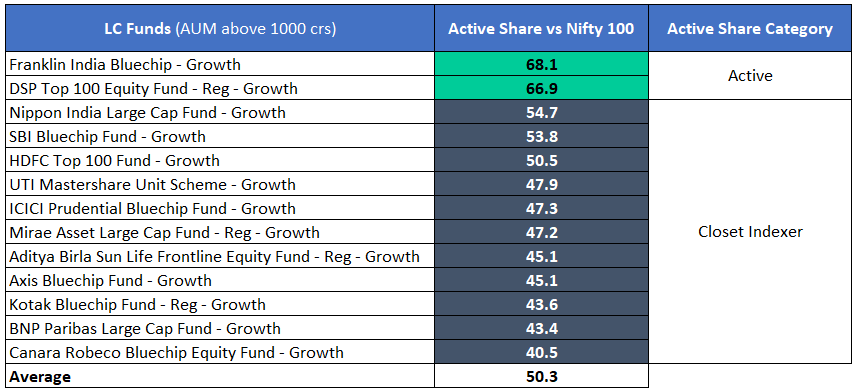

Many fund managers that claim to be active fund managers deviate only modestly from their benchmark indexes. One way to quantify the degree of divergence is through active share, a statistical measure comparing a fund’s holdings against those in the fund’s benchmark.

Developed by former Yale University finance professors Martijn Cremers and Antti Petajisto, active share can be assessed along a spectrum, as shown below.

Under this model, an active share of 60% or higher is required to be considered genuine “active management”; 20%- 60% is designated “closet indexing”; and less than 20% is deemed “index” (passive). By taking active share into account, investors needn’t rely solely on returns to gauge how an active manager is adding value.

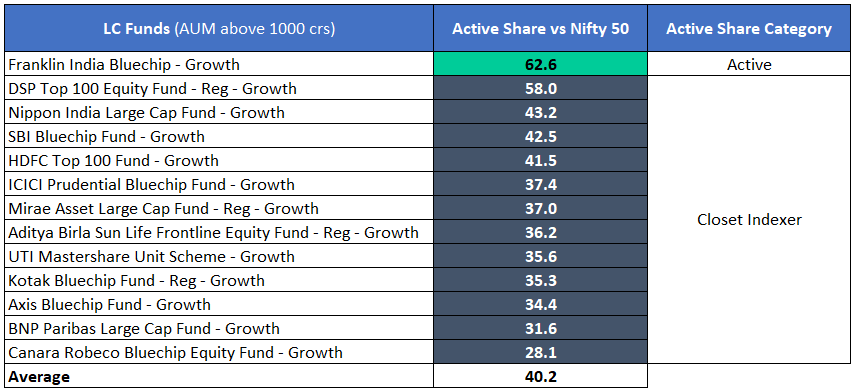

Let us check where our Indian large cap funds fit in this spectrum

As seen above, all large cap funds except for one fund, fall in the ‘Closet Indexer’ classification. This means that most funds on average have only 40% of their portfolios which are different from their underlying benchmark. In other words, on average there is roughly 60% overlap for actively managed large cap funds with their passive benchmarks.

Imagine the difficulty of an active fund manager who with a 40% differentiated portfolio, has to outperform the index by 2-4%.

4. Sticking to long term outperformers is difficult

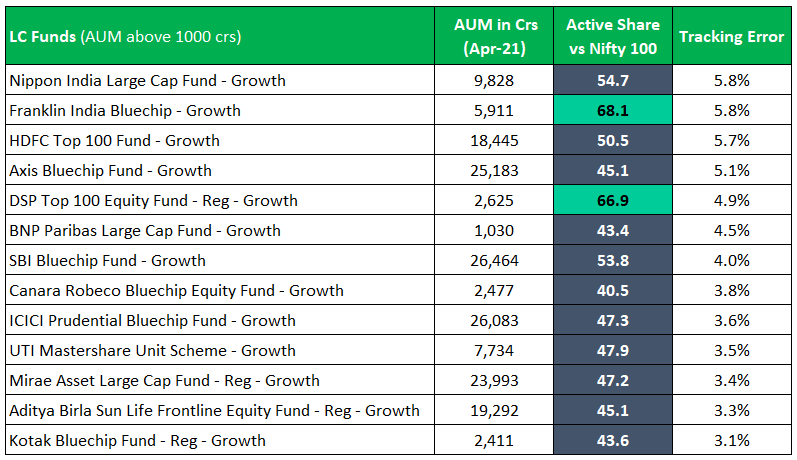

To outperform passive funds by a significant margin over the long term, fund managers will have to take meaningfully different exposures.

This also means that in the short run there might be a stark differential in performance versus benchmarks. This is indicated via a metric called tracking error. High tracking error reveals that the active large cap fund’s performance is significantly different from the performance of the benchmark and vice versa.

High tracking error is inevitable if you run a differentiated portfolio. This means there will be periods of stark performance differential.

While stark outperformance obviously is not a problem, there will also be periods of stark underperformance. So from a behavioral standpoint, given the usual tendency to exit funds after short term underperformance and choose funds with short term outperformance, it is tough to stay the course in funds with differentiated portfolios which is also necessary for long term outperformance.

Summing it up

What is our take on the Large Cap Active vs Passive Debate?

Long Term View:

- Prefer Large Cap Oriented Flexi Cap funds over Large Cap funds

- If you only want pure Large Cap Exposure prefer Passive funds (refer our earlier article here)

Our Long Term View is that, given the narrow universe, high portfolio overlap with benchmark and expense ratio differential it is difficult for large cap fund managers to provide meaningful outperformance over the long term. Even behaviorally it will be challenging for investors to stick to differentiated portfolios especially during periods of underperformance.

Short Term View:

We may see a temporary intermittent phase where many large cap funds are able to outperform their benchmarks over the next 1-3 years.

This is led by our view that mid caps have started to outperform large caps and the polarization of returns in top 5-10 stocks is reducing.

What are we doing?

We are gradually moving out of the Active Fund Large cap space and for investors looking for pure large cap options, passive funds are a better option.

For building our equity portfolios, we continue to prefer actively managed flexi cap and mid/small cap active funds. The key parameters that we look for are consistency in investment style, consistency in performance, long term performance track record, experienced fund manager and good risk management.

Our Equity portfolio construction is based on our Five Finger Strategy where we diversify across different investment styles, market cap segments and geographies. You can read about our unique strategy here.