Last week, an old college friend of mine had called. He wanted to invite me for his housewarming party as he had recently purchased a new house. During our conversation about work, life after college etc, he made a passing remark that he would have invested in equity funds too had they not been so daunting.

Think about it. This came from someone who just bought a house after months and months of research.

Buying a house is a fairly detailed and long drawn process. You need to…

Decide the budget -> Decide the location -> Search for properties offline/online -> Physically Inspect shortlisted properties -> Perform due diligence -> Secure housing loan -> Make the purchase -> And then, finally complete the registration.

Phew!!

Now here comes the shocker. Even for a person who is ready to put in so much effort, equity mutual fund investing seems to be extremely complex and confusing.

Why would this be?

Think about it. There are 40+ fund houses offering hundreds of different equity fund schemes across various categories. There are too many choices, jargons and the worry that – ‘what if we end up with the wrong choice’. Mostly this ends up paralyzing our decision making. Add to it, the fact that often top funds of the past suddenly seem to underperform and vice versa.

No doubt constructing an equity mutual fund portfolio is considered to be complex and daunting.

But can’t we just invest in the funds that have been doing well and move on?

Unfortunately, there is enough evidence that this strategy doesn’t work. In fact, portfolios with only the recent winners more often than not tend to underperform at some point in the future.

While this is counterintuitive, think about it. All of us naturally choose funds in this manner. If this had worked by now we wouldn’t be complaining.

True. But wait?!

Why would a portfolio of top performing funds not work well?

To understand this better, we need to take a step back and understand why some groups of stocks with certain common characteristics provide better returns vis-a-vis benchmark in the long run.

Well, there are a number of ‘factors’…

Investment researchers across the world have found out that a group of stocks with certain specific characteristics reward investors more than the popular market cap based benchmarks (such as Nifty 50). These characteristics are called factors.

Till date, a total of 7 factors have been identified, which have proven to be persistent (i.e they continue to keep working) and have worked across different equity markets.

- Value

- Quality

- Growth (evolved to become Growth at Reasonable Price)

- Small and Midcap

- Low Volatility

- Momentum

- Dividend Yield

The factors of Value, Quality, and Small & Midcap have been used by Indian Fund Managers in the mutual fund space. In addition, we also have a jugaad style, where Growth style has evolved slightly to become Growth at Reasonable Price (GARP) where value as a factor also gets blended.

While low volatility also works well in India (check out our inhouse product based on the low volatility factor here), this is a factor that Indian fund managers have not explored enough and is still very nascent in terms of its adoption.

Coming to the other factors, Dividend Yield hasn’t worked well in India. Momentum factor while it works well theoretically, but given its high turnover, is practically difficult to execute it on a larger scale. UTI has recently launched the first offering around momentum and we will need to wait and evaluate if this factor can be executed at scale.

At this point, let me stop and explain these four important investment styles

- Value – This style is based on the thesis that a basket of undervalued stocks will outperform the market over the long run. Value fund managers usually hold companies with relatively lower valuations (low Price to Earnings, low Price to Book ratio etc) in the belief that valuations will mean revert. These usually are companies with good fundamentals but are presently out of favour – unloved, underowned & undervalued. You can think of this like buying property available in a not so developed suburb, the worth of which you expect to improve over the next few years as the locality picks up.

- Quality – This style is based on the thesis that a basket of high quality stocks will outperform the market over the long run. The fund managers following this style usually invest in a group of companies with strong fundamentals as measured by Balance sheet strength, low debt, consistent cash flows, ROE, ROCE, Management quality and robust growth prospects. Valuations will not be considered as a key factor in quality focused funds. You can think of this as buying property in a posh neighbourhood.

- Growth at Reasonable Price (GARP) – This style is a blend of Growth and Value. The fund managers following GARP philosophy will invest in companies with potential for good earnings growth but are available at reasonable valuations. These funds will discard very expensive companies with good growth as well as very cheap companies with little to no growth.

- Size – This is based on the evidence that historically, smaller companies (Mid and Small Cap) tend to give better returns than larger ones in the long run.

The above four styles pertain to the Indian context. So, in order to ensure a bit of geographical diversification in the portfolio, we can add Global Exposure also to our list.

Different styles do well at Different times…

While these investment styles have proven to work across long time periods (10+ years), all these styles do not perform equally well across all short term periods. All investment styles go through their cycles and have phases of underperformance followed by significant outperformance and the cycle repeats. In the longer run, the phases of outperformance compensate more than enough for the lean phases of underperformance.

This simply means all styles will inevitably have to go through the pain of temporary underperformance.

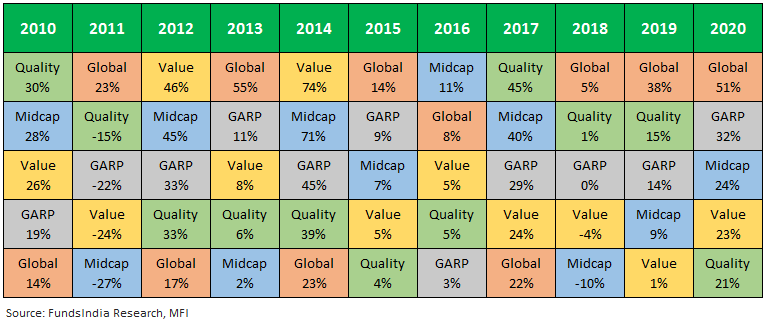

We have selected one equity fund under each style and evaluated the performance of the five styles in every calendar year since 2010. As seen below, there is no style that consistently outperforms as the styles keep rotating in and out of favour.

By only picking funds that have done well in the recent past, you are likely to end up with a portfolio concentrated on one or two styles. When these styles go out of favour, your entire portfolio might go through prolonged underperformance for years.

So, how to identify which style will perform well in the next few years?

Well, that’s the million-dollar question! We have no choice but to remain humble and remember the obvious that it is extremely difficult to predict when these styles will be in favor or go out of favor.

Despite this, we can build a simple and effective portfolio using the time tested magical tool – Diversification.

Instead of trying to predict which style will work over the next 5-7 years, we prefer to diversify across these five styles.

Our belief is that – Time in the style is more important than Timing the style!

So how do we build a simple and effective equity portfolio?

Here is an approach that we internally use to build fund portfolios for our clients. We call it the ‘5 Finger Framework’. This framework offers adequate diversification across the investment styles and ensures that the portfolio at an aggregate level provides consistent performance over 5 year periods with significantly lower volatility (thanks to diversification).

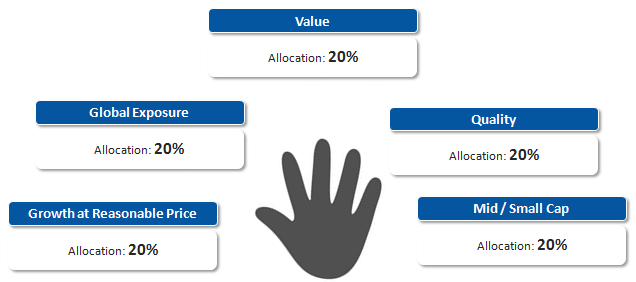

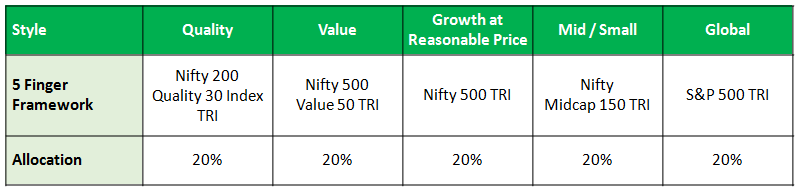

The 5 Finger Framework

Like we need all the five fingers in our hand to perform our daily activities effectively, a good equity fund portfolio needs all the five styles – Quality, Value, Growth at Reasonable Price, Mid / Small Cap and Global Exposure to perform effectively. Our Select Funds are chosen in a way that all these various styles are adequately represented and played via the best funds. Under the 5 Finger framework, the equity portfolio is split equally across all these styles.

But will this diversify away the performance as well bringing it back to index performance?

To be honest, even we had this doubt.

All styles have been proven to outperform broader benchmarks (say Nifty 50, Nifty 500) over the long run but with occasional periods of temporary underperformance. The idea was that combining these styles can keep the long term outperformance thesis of the styles intact while addressing the short term underperformance issue.

This is still theory, let us see how the evidence stacks up…

Superior Performance and Strong Risk Management…

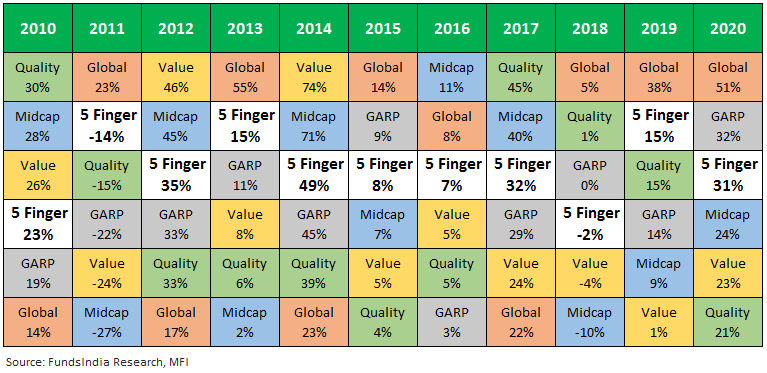

In order to see how the 5 Finger Framework has worked in the past, we have built a sample portfolio with five equity funds (one from each style with 20% allocation to each – all are part of Fundsindia Select Funds). For the global exposure style, we have taken an index fund due to the dearth of actively managed funds with proven long-term track record. For the other four styles, we have considered actively managed funds.

The backtested results clearly indicate that the portfolio performance becomes much more consistent when using this framework instead of focusing on one particular style.

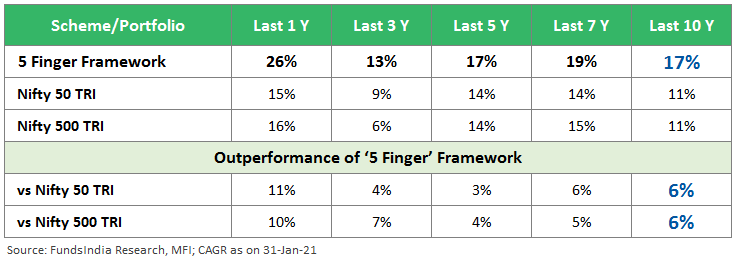

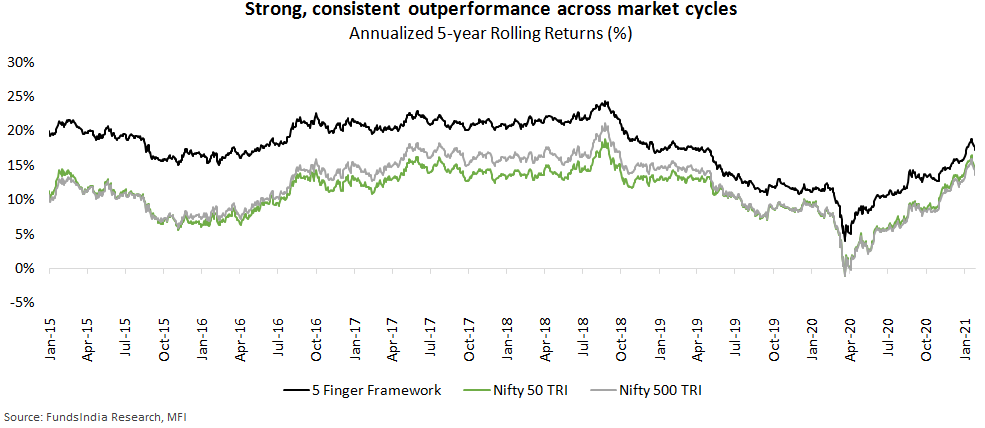

Now, let us see how the 5 Finger portfolio fares in the long run against Nifty 50 TRI and Nifty 500 TRI.

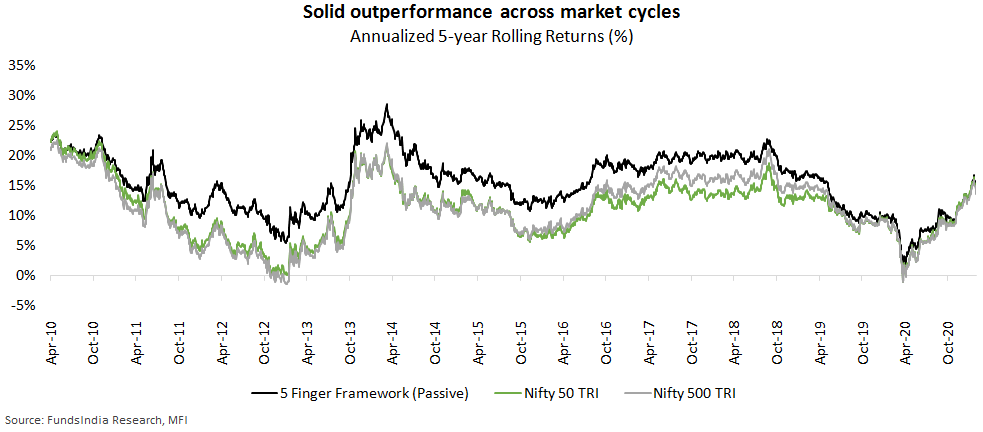

Consistent superior performance across different market cycles…

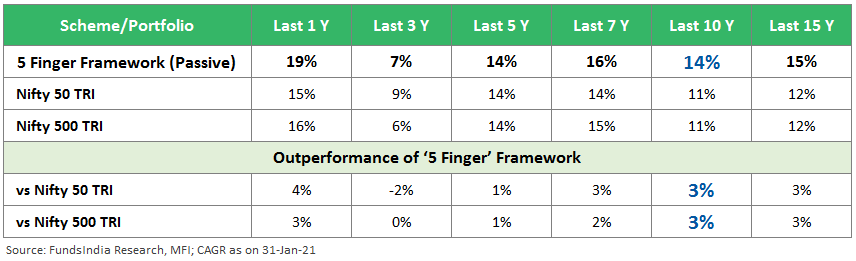

In the last 10 years, the 5 Finger Framework has delivered 6% higher returns on an annualized basis over the benchmark indices.

This approach has worked very well consistently with an average CAGR of 17% across all the 5-year periods since 2010.

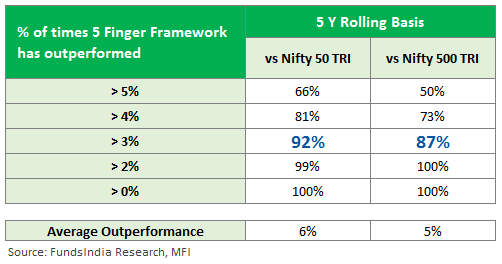

There is a significant outperformance of 5% – 6% over 5-year periods on average versus the benchmarks. In fact 92% of the times, the 5 Finger framework has outperformed the Nifty 50 TRI by more than 3% over rolling 5 year periods.

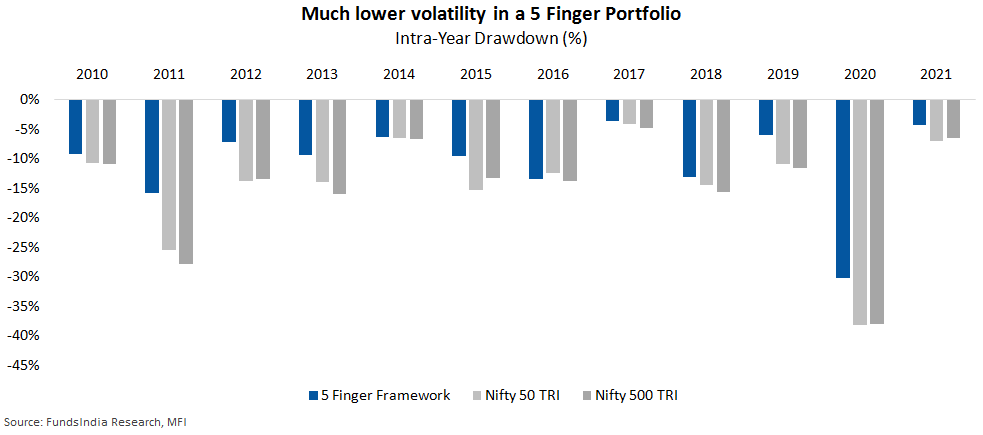

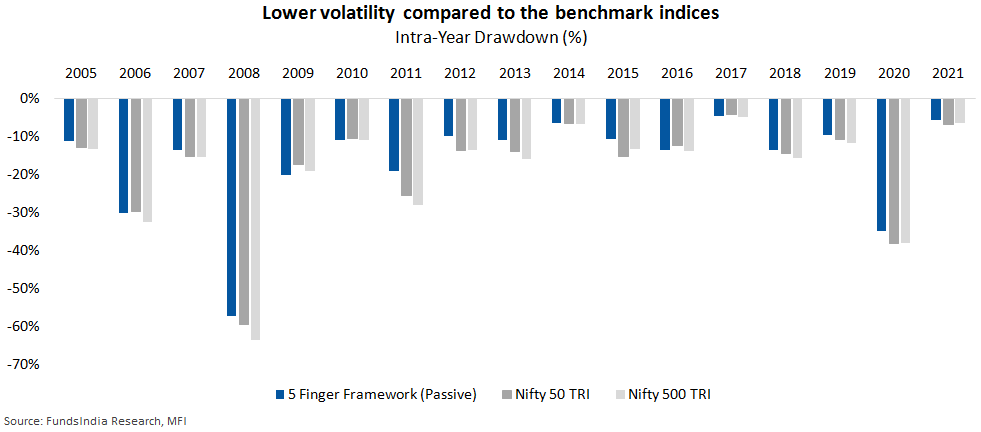

5 Finger Framework shines in the risk management aspect as well…

The 5 Finger portfolio has a Downside Capture Ratio of ~57% against the Nifty Indices i.e. it roughly captures only 57% of the falls suffered by the broader market. A ratio less than 100% indicates strong risk management ability of the portfolio.

As seen from the intra-year declines (maximum falls faced by the broader market within a year), the portfolio using the 5 Finger framework has fallen lower than the benchmarks.

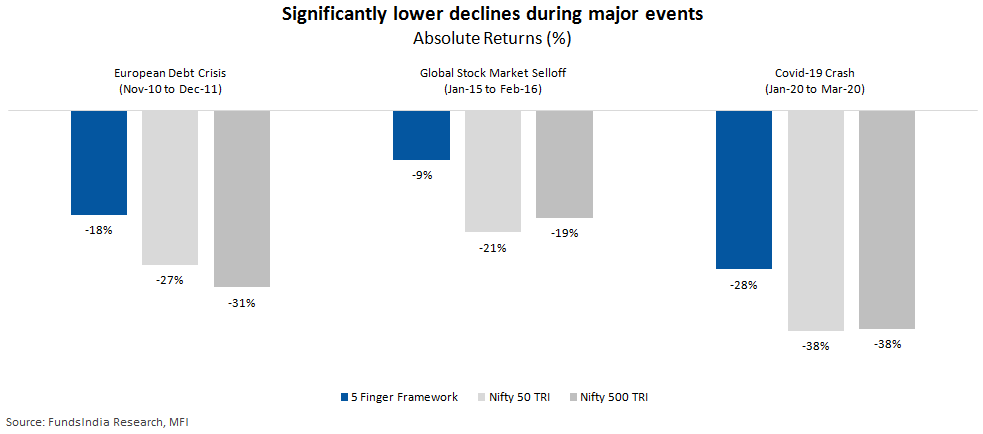

We can also see that this approach has been resilient during the major market declines in the past 10+ years resulting in low falls.

Okay, but what if these results are driven by the fund choices and not the strategy itself?

Here is the ‘unbiased’ passive version…

Let us re-create the 5 Finger portfolio by only using the indices respective to the five styles..!

The performance of this portfolio from Apr-05 (first data point when all the indices were in existence) has been evaluated. Despite the passive nature of the portfolio, the 5 Finger framework delivers better performance than the benchmarks.

The performance has also been consistent over 5-year periods with an average outperformance of 4%.

The passive 5 Finger framework has beaten the benchmark indices three-fourth of the times by more than 2%.

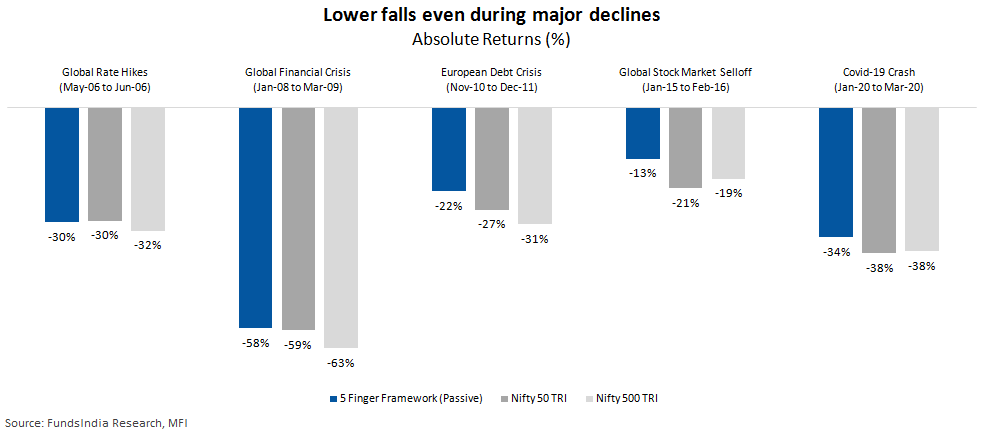

The passive approach has a downside capture ratio of ~83% when compared to the benchmarks indicating its ability to withstand volatility.

The intra-year declines of the 5 Finger portfolio even when invested in indices have been than lower the benchmark indices.

And the same story (better risk management) is evident during major market declines as well!

So that clears the issue of our fund selection bias. The 5 Finger strategy works great as a concept as seen from combining the passive style indices and with the right set of active funds in the portfolio, the strategy becomes even more potent.

What else should you know before you build your portfolio using the 5 Finger Framework?

Annual Rebalancing of the Portfolio

As different styles do well at different periods, your portfolio allocation to different styles may drift over a period of time. Even when you start with an equal allocation of 20% to each style, the same portfolio could automatically become slightly unbalanced after, let’s say, an year with increased allocation to styles that were performing well during the year and reduced allocation to styles that were not doing well. If unattended for a long time, the allocation could unintentionally tilt towards certain styles (which are currently performing) with lower allocation in other styles. This defeats the whole purpose of diversification and again makes the portfolio concentrated towards recent performing styles.

Portfolio rebalancing is a simple action which ensures that your portfolio maintains equal allocation to each investment style. At the end of every year, you can revisit your portfolio and rebalance it if the allocation to any style changes more than +/- 5%. By rebalancing, you just have to sell the excess portion in styles with increased allocation and use that amount to buy in styles with reduced allocation.

The portfolio performance shown so far is of a portfolio rebalanced annually whenever allocation deviates more than +/- 5%. The performance deteriorates if left unbalanced.

Fund Selection & Suitability

The performance of any strategy is as good as its underlying funds. You can invest in one or more funds under each style. But it is important to pick the right funds under each style. You can refer to our Select Funds list where we identify good funds and experienced fund managers to play the particular styles.

The 5 Finger approach is suitable only for patient investors with longer time frames (at least 5 to 7 years). Some styles may go through relative underperformance over several years. It is important to stick with such investment styles and stay invested despite the underperformance in order to reap the full benefits of diversification as we can never know when investment styles go in and out of favor.

Please remember that at all points in time there will be 1 or 2 investment styles which are underperforming. The good part is these 1 or 2 styles will keep rotating over the years.

This is by design and should be considered as a feature rather than a bug!

Summing it up

- Different investment styles work well during different market phases. Hence it becomes important to diversify across investment styles.

- Every investment style goes through its own phase of underperformance and outperformance

- Picking funds based on past performance leads to overconcentration in few styles which are performing well – as these styles go through their inevitable phase of underperformance, your entire portfolio may go through long periods of underperformance

- An alternate approach to equity fund portfolio construction – 5 Finger Framework – Allocate 20% to each of the five investment styles – Quality, Value, Growth at Reasonable Price, Mid & Small Cap and Global Exposure

- Rebalance once a year – whenever the allocation to a particular style deviates by more than +/- 5%.

- This approach delivers consistent performance over long periods with much lower temporary declines compared to broader indices

- Suitable for patient long-term investors (7+ years) who can stick to the overall strategy and stay invested even in investment styles that underperform as a part of the overall portfolio.