The Sensex has galloped nearly 10,000 points in the space of just over a year. This incredible run has come in even as reforms disrupted the corporate and economic recovery process. Can 2018 score a repeat of 2017, as reforms and recovery get underway?

On a wing and a prayer

Step back and look at the run in 2017. There are three characteristics to it. These characteristics are set to have an impact on what 2018 can turn out to be.

One, the expected economic recovery was delayed. The government had spent the years between 2014 and 2017 improving macro-economic variables and the hope was that this would finally translate into growth. However, the after-effects of 2016’s currency withdrawal and the implementation of the GST not only disrupted the normal functioning of business but also delayed growth. GDP growth slowed to 6% for the first half of the FY-18 fiscal against 7.7% in the comparable period of FY-17. This apart, lending and borrowing activity was slack as banks and companies continued to attempt repairing their balance sheets; the Reserve Bank eventually forced banks to deal with their bad loans.

Two, there was an abnormal complete lack of volatility in the markets. This phenomenon is odd given the several events that should have, by all accounts, caused some worry. Apart from the GST, crude oil prices were rising, the Reserve Bank was becoming cautious on inflation, companies were seeing their raw material costs rise on higher commodity prices, farm produce prices were crashing despite good monsoons, and bond markets were signalling pessimism. Despite it all, volatility (by looking at rolling 1-month Sensex returns) was the lowest in 2017, compared to the years since 2007.

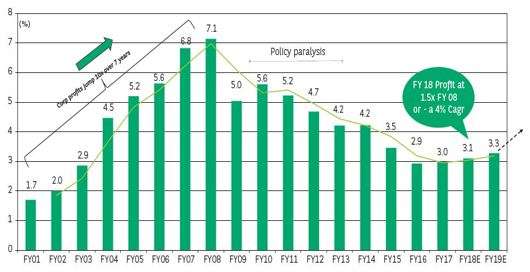

The third was that market valuations found no earnings growth support. Overall corporate revenues and profits grew just 10% and 3% in the April-September 2017 period against the year ago. That hardly supports the 36% returns in the Nifty 500 index. The two charts below show the contribution of corporate profit to GDP and the PE movement of the Nifty 50 and the Nifty Free Float Midcap 100.

The chart above shows the proportion of corporate profit to GDP over the years. Source: BNP Paribas MF

In other words, valuations that ran ahead of fundamentals and delayed economic growth by one-off structural reforms did not deter the market from moving up. That there was no fear was also reflected in the low volatility in the market in 2017. Why was this and what is the market taking cognisance of to keep itself afloat? Let’s look at the drivers.

Long-term drivers

On the macro-economic front, indications are that growth has bottomed out. The September quarter GDP number at 6.3% was better than the 5.7% of the June 2017 quarter. So what can drive growth in the longer term?

- Reforms: 2017 was a year when several reforms were undertaken. These reforms work towards a stronger economy over the long term but caused disruptions in the medium term. The GST was the biggest of these, and the impact it can have on logistics, corporate costs and profit margins, tax compliance, and government revenues will start to come into play. Bank recapitalisation and the insolvency regulations have begun the bank balance sheet clean up. This can also fire up lending; while non-food credit has picked up in the past few months, it is still the lowest in several years. Real estate regulations and a drive to implement housing for all can step up construction activity. The Bharatmala road project, along with urban infrastructure development, and railway industrial corridors can step up infrastructure activity. The market appears to be betting on these reforms to shore-up corporate profitability on one hand and drive consumerism on the other.

- Broader consumption story: While the Indian equity story has successfully ridden the urban consumer story and will continue to, there is more hope now on rural consumption picking up. The government’s ambition of doubling of farm income is a key to this. The focus on improving irrigation and reducing monsoon vagaries besides enabling better pricing for farm produce through a nation-wide electronic market (already implemented) can realise this ambition. Another move already implemented is providing crop insurance to farmers to cover losses. Focus will also be on improving rural infrastructure and increasing incomes from allied activities. If successful, this goal can have significant impact on growth. From a corporate perspective, this will make rural consumption a strong story to bet on. Companies are already citing higher rural income as a growth driver in addition to a revival in urban spending, for the upcoming quarters. The RBI’s November 2017 consumer confidence survey notes that the majority of consumers expected to increase spending in the coming year, even as they expect inflation to rise. Consumption indicators, such as car and two-wheeler sales, aviation passenger traffic, growth in sales for consumer discretionary such as retail companies, restaurants, and FMCG companies are also picking up after subdued quarters in 2017.

- Investment: This is the one GDP component refusing to move. But with reform disruptions out of the way and bank clean-up and insolvency proceedings underway, this could improve gradually. There are some signs of a revival in manufacturing sentiment; if these persist, it could finally kickstart growth. For example, the November IIP index staged a massive 8% growth after spending the rest of 2017 at a level below 5%. The Manufacturing PMI index rose to a 5-year high in December. Industrial credit has actually managed to rise 1% in November 2017 (latest available RBI data) against contraction in credit in earlier months. However, even if this were to remain sedate and companies use their existing capacities more, the trigger to revenue and earnings can be healthy enough.

What to expect in 2018

In our view, market returns have come in ahead of improvement in corporate fundamentals. Please read our view on earnings revival here. We think 2018 will be a year when these fundamentals will come into place to justify the rally. This year can be more subdued to allow for economic green shoots to actually take root and sustain.

- Earnings catch up: Corporate earnings failed to take off due to reform headwinds, 2018 is set to be a year where earnings finally grow. The government is only likely to continue implementing established reforms and not start new ones. Large-cap companies have already showed a recovery in earnings, going by the September 2017 quarter results where stocks with a Rs 5,000 crore and above capitalisation grew 8% in profits. The Nifty 50 saw double-digit growth in revenues and profits after six quarters of muted performance. The available latest December quarter results also show aggregate revenue and earnings growth at 13% and 25% respectively. A low base will aid the revival too.

- Toned down returns: With fundamentals falling in place to justify valuations and the market run up, a further rise from here may be limited. A repeat of 2017 seems unlikely. The good news though, is that with subdued returns and long-term drivers working out, the market situation becomes less worrisome. It provides more comfort than the situation a decade ago; we are not yet at a growth peak both for the economy as a whole and for companies. High capacity utilisations, a large growth in earnings, high economic growth are some signs that the room for growth is limited and we are not there yet. Globally too, growth is coming in.

- Resurfacing volatility: There are several events lined up for 2018 which can bring back volatility and reduce the buoyant positive sentiments. The first is the budget, due next month. The last full-fledged one before the general election, the risk is that the budget turns populist and provides short-term sops to the rural segment. This will affect the fiscal prudence and long-term growth path that the government has adopted in all its budgets thus far. The second is the several state elections lined up over the year which will be cues for 2019’s general election and political stability. The third is inflation and crude oil, and resultant RBI policy action. Global factors include central bank action of various countries and a squeeze in abundant liquidity.

What should you do?

The characteristics of the 2017 market show that for now, returns have run ahead with virtually no volatility. 2018 will be a year when focus will return to fundamentals and growth along with external and election-based risks. Given this, there is no single strategy that comes out ahead. Here is what you should do.

- Which market-cap segment to be in: Use the market rally to shift to attractive market-cap segments. The rally mid-caps and small-caps have seen since 2014 provides a good opportunity to shift into large-caps, which are more attractively-valued today. This is especially if you have an overdose of mid- and small-cap funds. Small-cap funds are anyway reorienting their portfolios away from small-caps and into larger stocks. Since January 2014, mid-cap funds have on an average delivered an annualised 30% return. The large-cap market segment has had more corrective phases and has not rallied as sharply as mid-cap and small-cap funds. In terms of earnings performance too, stocks in the large-cap bucket have shown stronger recovery than those in the small-cap set.

- What strategy to follow: There is no one way here. Mix funds following different strategies to capture the maximum the market has to offer. As we’ve said, markets would now pay attention to growth and are unlikely to reward simply in anticipation of it coming in, as it has been so far. However, growth is not going to be uniform across sectors. The September 2017 earnings numbers present a mixed picture, especially in sectors such as capital goods and engineering. Though infrastructure as a whole can pick up, several companies are in tight financial circumstances. Consumer companies look to be bouncing back the quickest, but valuations are far more stretched here. Pharmaceuticals are a mixed bag with US-focused players still struggling. Software looks to be a value play but still face headwinds. The margin of outperformance for funds has narrowed over the past couple of years. Because funds follow different methods of stock-picking, holding funds that have different ways of doing this maximises your portfolio’s ability to gain. What are the strategies to look for? Value-based and growth-based strategies are one. Concentrated allocation and diversified allocation could be another. Others involve taking tactical stock and sector calls to capture quick market movements and those that prefer to take longer-term calls on growth prospects. For those on the more conservative side, including funds that take cash calls will be useful.

- When to invest: There is no way other than SIP now (or STPs run over 10-12 months if you have a lump-sum). There is even less certainty now that markets will head higher. Trying to time markets is getting harder. Resumption in volatility can help average costs if you run systematic plans. Don’t stop your SIPs because you would miss volatility advantages. Further, in volatile markets, chances to catch corrections may be brief and missed if you don’t act quickly. Don’t also be scared into exiting equity altogether. Not staying invested can cause opportunity loss. In the space of the past four months, markets have broken past highs four times. In 2015, the Sensex was at an apparent peak of 30,000. Today’s market leaves this level far behind. Remember that equity is for the long-term and staying invested is what allows you to benefit from the returns. If your goal is approaching – i.e., you need to liquidate your investments for a purpose – this year or next, you can move equity towards ultra short-term funds.

Of course, in all this, keep in mind that you need to have an asset-allocated portfolio. It will help protect your portfolio and reduce the effect of market downturns and volatility. It serves you better than trying to time markets.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.