For a person looking for a low-risk mutual fund option for parking short term money, we recently took a look at the pros and cons of arbitrage funds vs. liquid funds. However, this mostly works only for time periods lower than one year. For time frames longer than this, you will be sacrificing returns by opting for these funds. So for longer timeframes, your choices are conservative hybrid funds or equity savings funds.

Funds in these two categories differ significantly in what they do. Conservative hybrid funds primarily invest in debt securities, with 10-25% of their portfolio going towards equity. The debt portion of these funds is managed dynamically. They may take credit risk, go for duration strategies when appropriate or simply stick to accrual strategies. For instance, the average credit exposure for a particular fund during the last 6 months has gone as high as 65%. The category average is 16.6%. They can also carry some long duration papers, the category average maturity is 3.43 years.

Equity savings, on the other hand, invests primarily in equity with about 25% of their portfolio going to debt. However, the equity portion of these funds is partially hedged, leaving them with a net equity exposure of 35-40%. The hedged portion neutralises equity risk, making these funds much lower risk than balanced advantage funds and hybrid aggressive funds.

Both conservative hybrid and equity savings funds are meant to be held for a short period of time, typically around 2 years. With that in mind, let us look at which category is more suitable for which type of investors.

Returns

In terms of returns, conservative hybrid funds generally manage to beat equity savings funds. On a 1-year rolling basis in the past 5 years, the category average returns for conservative hybrids was 9.26% while that for equity-savings was 8.31%. Conservative hybrid funds have outperformed equity savings funds on 72% of the occasions.

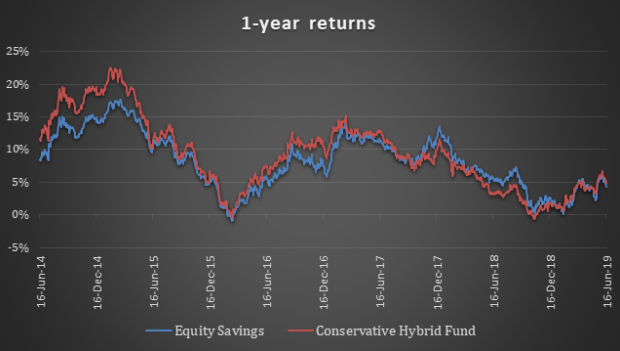

Here is a graph of 1-year returns over the past 5-years. As you can see, equity savings has mostly lagged conservative hybrid funds, more so in bull markets.

The outperformance of conservative hybrid funds can be explained by their strategy. Many of these funds adapt their portfolios to the debt market and thus generate reasonable returns. Even for funds that stick to high-quality accrual, the average maturity of the papers is around 2 years which have yields higher than liquid or ultra-short duration funds. The equity portion, though small, still give a push to returns, especially in bull markets.

For equity savings funds, though, the hedged portion delivers arbitrage-like returns which are generally on par with liquid funds. This reduces their return potential compared to conservative hybrid funds.

Risk

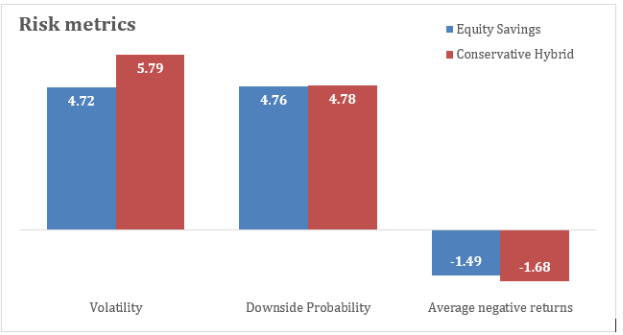

Volatility is an important concern when investing in funds for the short term. Both these categories have equity exposure, and as such, are subject to volatility. Additionally, conservative hybrid funds may also suffer some volatility if they take duration calls. On this count, equity savings funds tend to be less volatile and contain downsides better.

To check the volatility, we took the standard deviation of 1-year returns over the past 5 years. We also looked at the downside probability, i.e., the likelihood of getting negative returns on a 1-year basis in both these categories. While the probability itself is pretty similar, the downsides tend to be slightly bigger in conservative hybrid funds. The average of 1-year negative returns of equity savings funds is -1.49% while that for conservative hybrid funds is -1.68%.

Taxation benefits

However, we cannot ignore the tax advantage offered by equity savings funds. Since they get the tax treatment of equity, in periods over 1-year, they enjoy a lower tax rate of 10%. However, conservative hybrid funds continue to be taxed at slab rates up to a period of 3 years.

For taxpayers in the 5% slab, the conservative hybrid is the clear winner as it gives higher returns and suffers lower tax. As with arbitrage and liquid funds, the tax differential isn’t large enough to overcome the return differential between the two categories.

If the investor is in the 20% tax slab, there’s, unfortunately, no clear winner. In the last 5 years, you’d have had an equal chance of getting higher or lower returns in either category. However, for someone in the 30% tax slab, equity savings managed to do better 72.5% of the times. Therefore, such investors can opt for equity savings funds.

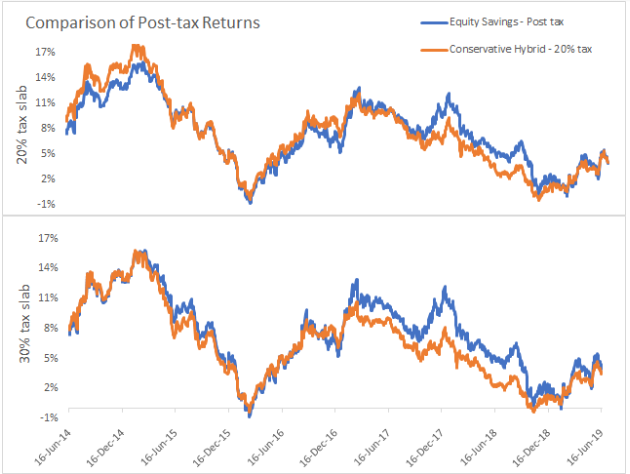

In the following graph, we look at the excess returns equity savings fund would generate for someone in the 20% and 30% tax brackets.

Which category should you pick?

- For investors in 5% tax slab – Conservative hybrid is the clear winner. The returns are higher and it suffers lower tax rates, resulting in decisively higher returns.

- For investors in 20% tax slab – Either of them is equally likely to outperform the other. You could take a decision based on either of two things. One, on your risk level – if you are very low-risk, you can consider equity savings funds as you will get the same returns for slightly lower risk. If not, you can opt for either category. Two, on your interpretation of the rate cycle and strategy of the conservative hybrid fund – if the fund takes duration calls and the rate cycle is downward, you could get better returns out of conservative hybrid funds.

- For investors in 30% tax slab – Equity savings has a higher likelihood of giving better post-tax returns. Take care not to use equity savings funds for time-frames longer than 3 years – aggressive hybrid funds and balanced advantage are better bets for such time-frames.

All investors should, however, keep in mind that these are probabilistic analyses. Your actual returns may vary depending on the time and frequency of your investments.

Which fund should you pick?

In the equity savings category, our recommendation is Kotak Equity Savings fund. This fund has been around for a while and has been consistent in its performance.

In the conservative hybrid category, our recommendation is ICICI Prudential Regular Savings fund. This fund does well in containing volatility. This helps the fund deliver better risk-adjusted returns compared to its peers.