When you look at low-risk options for parking short-term money, liquid funds are often opted for. But the tax-conscious amongst you often ask us if you should go for arbitrage funds instead since they are taxed at lower rates. Here, we stack up the pros and cons of the liquid and arbitrage funds and tell you how to decide what’s suitable for you.

What do the funds do?

These two categories of funds are very different in what they do. For starters, liquid funds hold debt instruments while arbitrage funds invest in equity.

Liquid funds aim to generate returns by accruing interest from underlying papers. They invest only in very short-term high-quality papers. Therefore, they have a very low credit risk and interest rate risk. Their holdings don’t see price volatility and this makes liquid fund returns stable. Barring exceptional circumstances, they don’t suffer losses even on a daily basis. This makes them an ideal option for temporarily investing surplus money.

Unlike other equity funds, arbitrage funds are low-risk because of their strategy. Arbitrage, as a strategy, aims at taking advantage of mispricing between the cash and the futures market. Arbitrage funds hedge their entire stock holdings. Essentially, there is no market risk despite investing in equity. However, because of this hedging, they also don’t enjoy equity-like returns.

The question of whether arbitrage or liquid funds are better options for short-term investments involves understanding three aspects – returns, risk, and taxes.

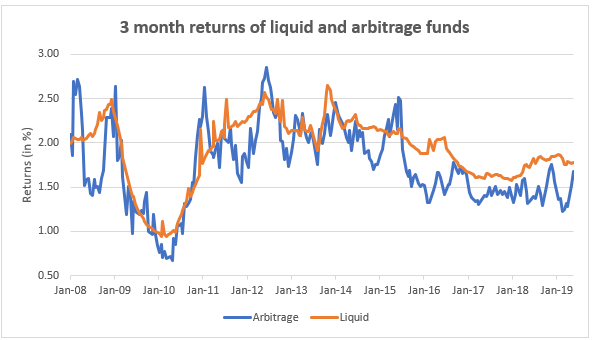

Comparing returns

The usual holding time frame for liquid funds is around 3 months or less. We used these time frames and the average returns of both the categories to understand how returns pan out. Here’s what we found.

- There is no distinct trend in returns:

Liquid funds move in line with interest rate cycles while arbitrage funds look for mispricing opportunities. While both categories have different factors affecting their returns, there is no clear correlation between stock market cycles and arbitrage fund performance. At best, arbitrage does well at market cycle inflexion points or in flattish markets.

2. Liquid funds, on an average, have returned better:

In the past 10 years, liquid funds gave higher returns than arbitrage funds 80% of the time if we consider 3-month and 1-month periods. Lack of arbitrage opportunities, smaller gains from hedging activity, and relatively higher expense ratios could be reasons pulling down arbitrage returns compared to liquid funds. The differential in returns is not high – it has averaged 0.16 percentage points in the 3-month rolling returns.

Risk

The risk that you would like to avoid with these funds is volatility. When you park funds for a period ranging from a few days to a few months, you can’t wait for funds to recover from any short-term falls. This is why it is important to look at how the funds contain downsides.

We looked at the last 5-year period, ignoring any losses arising from the IL&FS debt crisis. On a monthly basis, both categories fared well with only one arbitrage fund seeing a marginal loss. But on a daily basis, there is a huge difference in volatility. Liquid funds hardly saw one-day losses with 2 or 3 exceptional instances while arbitrage funds suffered one-day losses around 30% of the time.

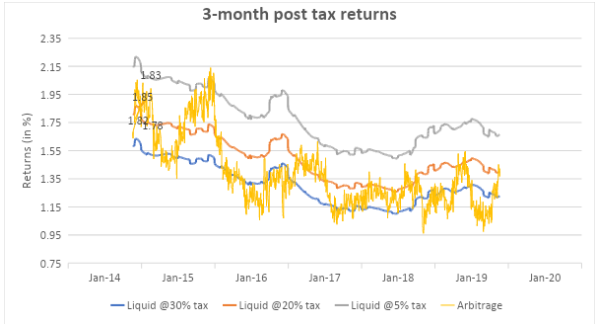

Post-tax returns

Now that we have discussed risk and return aspects, we’ll move on to what’s important – what are the post-tax returns you will realise.

Returns are absolute and post-tax

Since these funds are held for less than a year, short-term capital gains tax becomes more relevant. Debt funds are taxed at your income tax slab rate and equity funds are taxed at flat 15%. With liquid funds generally outpacing arbitrage funds in terms of returns, it is only the taxation that makes a difference.

- The above graph looks at 3-month post-tax returns for the last 5 years. On a post-tax basis, arbitrage funds score over liquid funds only for those in the highest 30% tax slab.

- Based on rolling 3-month returns since 2014, arbitrage funds returned better 64% of the time for these investors.

- If we consider 1-month returns, the number is 56% of the time. That means, they had better chances of realising higher returns with arbitrage. There are higher chances that those in the 30% tax bracket earn more on arbitrage funds than not.

- In the 20% and 5% brackets, arbitrage funds lag liquid funds even post-tax. This is mostly because of the low differential in tax rates. In fact, for those in the 5% bracket, the tax outgo on liquid funds is lower than arbitrage funds. With generally lower returns in arbitrage funds, the low tax differential keeps them from beating liquid funds.

Is there a clear winner?

As always, what is better for each investor varies. To summarise the points discussed:

- For those in the 30% tax bracket: Consider including arbitrage funds in your short-term portfolio (2-12 months), if you are keen on maximising tax savings. However, remember to keep expectations realistic. Arbitrage funds are not going to deliver high returns. As explained above, they work only because they have a significantly lower tax rate.

- For those in the 5% and 20% tax brackets: Avoid investing in arbitrage funds as you are better off with liquid funds. Either your tax itself is lower with liquid funds, or you’ll likely be earning more from liquid funds despite paying the tax.

- Holding period matters: Arbitrage funds are volatile for very short periods such as a few days. Since liquid funds stick to a simple very short-term accrual strategy, they are stable and will serve time frames of even a couple of weeks. If you have a requirement of less than 2 months, stick to liquid funds. Use arbitrage funds only if you have at least a 2-month period.

- Do not use arbitrage funds for STPs: Liquid funds are the only option for STPs as they do not deliver even 1-day losses barring extreme situations. Arbitrage funds frequently fall on a 1-day basis, as mentioned above. As a result, running an STP may inadvertently result in you booking losses.

Which funds to go for

Now that we have established arbitrage funds will profit investors in the 30% tax bracket, we move on to some good picks.

| Returns in % | ||||

| Scheme Name | 3-month | 6-month | 1 year | Fund Size (in Cr) |

| Edelweiss Arbitrage fund | 1.58 | 2.99 | 6.33 | 3,283 |

| Kotak Equity Arbitrage fund | 1.66 | 2.95 | 6.43 | 12,574 |

Returns as of 24 May 2019

When it comes to returns, Edelweiss Arbitrage and Kotak Equity Arbitrage have been category toppers. Both funds are consistent in beating their peers across different timeframes. Since they are for short term, volatility is an important parameter to look at. Kotak Equity Arbitrage is among the least volatile funds in its category. Edelweiss Arbitrage fund is slightly more volatile, but then it manages better on the return front. Both funds fare better than the category average in containing downsides as well, using metrics such as the worst return delivered and the probability of losses in different periods.

To sum-up, arbitrage can be selectively used for tax efficiency. They are not substitutes for liquid funds in terms of stability and liquidity.