What A value fund that invests across market capitalisations Why Whom Moderate to high-risk investors with a 5-year plus horizon

Markets have given up their post-election euphoria and are factoring in global concerns. In this volatility, aggressive investors can go for midcaps and smallcaps as opportunities are ripe. But for the tamer among you, funds investing across market capitalisations are a lower-risk route to capitalise on the same opportunity.

HDFC Capital Builder Value is an option here. The fund’s category is value, and it invests across market caps. It has historically sported a good mix of largecaps, with higher exposure to mid-and-small caps than other value-based funds such as Franklin India Equity.

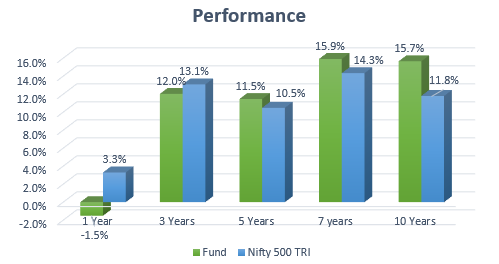

HDFC Capital Builder Value’s 3-year return averaged 14.6% since 2009, compared to the Nifty 500 TRI’s 11.1% and the 13.2% of peer funds. Since its inception in 1994, the fund’s 5-year return is 19.3%, against the Nifty 500 TRI’s 15.4%.

Steady performer

HDFC Capital Builder Value (HDFC Capital Builder) is not among the flagship or talked-about funds from the HDFC stable. Nor is it a chart-topper, posting flashy returns. What it is, is a stable, multicap fund that has steadily been notching above-average returns. On a rolling 3-year basis over the past decade, HDFC Capital Builder has ranked in the top quartile of similar funds more than 75% of the time. It beats the Nifty 500 TRI 96% of the time. The same holds over longer 5-year periods as well.

The fund can falter on a 1-year basis though, where it can slip lower down the rankings. However, this is attributable to the value orientation of its strategy. In the past year, for example, buying into some NBFC stocks, other beaten-down stocks such as Vedanta, Mahindra & Mahindra, and Apollo Tyres hurt. These stocks, however, may be well-placed to pick up on fundamental strength. Of late, exposure to Yes Bank and IndusInd Bank also weighed on returns.

Returns as of 17th June 2019. Returns over 1 year are annualised.

Strategy

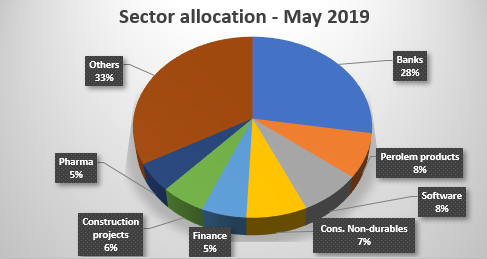

HDFC Capital Builder looks for value in both stocks and sectors. For example, it added Mahindra & Mahindra over the past year, but it is still underweight on the sector as a whole. It has picked up stocks such as Inox Leisure, Wonderla Holidays and VRL Logistics at various points in the past few years. On a sector basis, it increased exposure to pharma and oil & gas over the past year and software over much of 2018. It has infrastructure companies ranging from pure construction players to conglomerate Larsen & Toubro.

In sector weights, the fund does not deviate too drastically from the Nifty 500. This, along with timely identifying stocks and sectors, helps it clock steady returns. The fund doesn’t stick to an all-value strategy, another factor that bolsters performance. It can hold more expensive stocks either because they show promise or were earlier low-PE stocks that have rallied.

For instance, Dabur, Trent, GSK Consumer Healthcare, have all been part of the portfolio and can hardly be called value stocks. This strategy is similar to Invesco India Contra. It helps shore up returns in market phases where value does not hold up and thus prevents prolonged periods of underperformance that is the risk with pure value.

The fourth contributing factor is HDFC Capital Builder’s efficiency in pruning laggards. The fund does not give stocks too long a tether to turn performers, preventing them from dragging returns too much. Stocks such as NHPC, Mahindra Logistics, General Insurance Corp., ONGC, Tata Steel, for instance, have been pulled out of the portfolio over the past two years. Value-based strategies can lead to holding on to underperformers in the wait for them to be re-rated, and removing underperformers helps keep this risk at bay. The fund is also quick to book profits on or exit stocks where money has been made.

This also means that HDFC Capital Builder’s portfolio churn and volatility is on the higher side than those of Franklin India Equity, ICICI Pru Value Discovery, or Kotak India EQ Contra. Compared to multicap funds in general, though, volatility is lower than peers and risk-adjusted returns (measured by Sharpe) hold above the category average.

Suitability

Owing to lags in shorter-term periods, HDFC Capital Builder needs a holding period of at least 5 years. Mid-and-smallcap exposure can go up to 30-35% of the portfolio, and thus suits investors with a moderate and high-risk appetite. For long-term high-risk investors, it can serve as part of the core largecap exposure as well.

Portfolio

HDFC Capital Builder shares little similarity with other value funds, with overlaps mostly in the top banking stocks that are found in all equity portfolios. Its dominant sector exposure has always been banking, where it has steadily been overweight over the past five years. The fund has had limited exposure to NBFCs, but even this has been pruned.

Software is another sector where holding has dropped as stocks rallied significantly. The fund has instead upped oil & gas holdings, through a variety of stocks such as Reliance Industries, GAIL, and BPCL. Pharma and metals exposure has also been increased. This apart, the fund has several cyclical engineering, infrastructure, cement, and capital goods stocks.

HDFC Capital Builder has an AUM of ₹4,685 crore. Its manager is Miten Lathia.

Read more about this fund here.