After the bountiful double-digit returns witnessed in the equity category in 2014, 2015 may have been a letdown. This year will go down in your portfolio history as one of those turbulent years, with a good dose of a roller-coaster ride for you. As to how our list of Select Funds fared, we can say the funds kept their head above waters. And that was not an easy task, considering that the S&P BSE Sensex fell 6 per cent (calendar year until December 24, 2015).

Our equity funds as a category delivered 3 per cent on an average for the above period. That’s a good 9 percentage points more than the Sensex, and a comfortable 4 percentage points more than the -1.2 per cent return of the S&P BSE 500 (which is a better comparison as our equity funds are a mix of large, diversified and mid-cap funds).

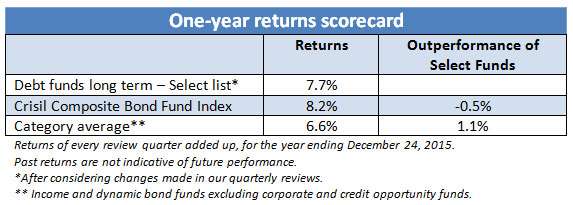

Debt, of course, was the outperforming asset class this year. But even there, while the first and third quarters of 2015 saw debt sizzle, the second and fourth quarters were sedate. As a result, returns could not be sustained for the full year. Our long-term debt funds delivered 7.7 per cent on an average, but could not overtake the ever-challenging Crisil Composite Bond Index’ return of 8.2 per cent. We will discuss why it was so, later.

Resist mid-cap temptation

Overall, it was a tough year. We could have loaded our list with mid-cap funds, considering the fact that they were outperforming early on this year. However, we resisted the temptation of doing so. One, we knew that the correction in large-cap stocks was a result of Foreign Institutional Investors (FIIs) selling and profit booking, and that afforded good valuation opportunities to enter and build wealth for the long term. Two, even while mid and small caps would deliver in the short term, their stretched valuations did not appear to lend much scope for sustained returns. Three, some of the small and mid-cap stocks showcased irrational exuberance, not backed by fundamentals. As a result, the abnormal returns in small and micro-cap funds held the risk of fizzling out.

In all, as always, we reminded ourselves that consistency matters over flash-of-the-pan returns. So, while we knew the absence of chart toppers may drag our Select Funds list’s near-term returns, we also knew we would not have to worry about it in the long term. And in a year like 2015, it was important to protect downside, than run behind returns; and our funds held ground on that count.

In this roundup, we have considered only two major categories of funds – all equity funds (large, diversified, mid and ELSS) and our long-term debt funds as the other categories serve limited purposes. Since we review the funds every quarter, we have adjusted the returns chart for changes made during our review. We have considered point-to-point returns for this purpose (up to December 24, 2015). The returns mentioned are average returns for that category.

Before going further, let me state the caveat that one-year performance will neither not tell you whether our calls were good enough, nor will it let you know where we lack. You may view this as a disclosure exercise as we like to keep you informed at all points, and the end of the year is a good juncture to take a re-look.

Also, 2015 was a quirky year for one key reason: it was a year when the market fell – but strangely characterised by fall in large-cap stocks, even as mid-cap stocks delivered. Hence, when you look back for past performance record, do not be enamoured by a mid-cap fund’s ability to have delivered in a market-negative year, and conclude that the fund outperforms in a down market. The 2015 charts may not tell the correct picture. You will do well to compare it with peers as well.

Equity fund performance

The 3 per cent returns that came by for the equity fund category was, of course, made possible only because of mid-caps. A number of large-cap and diversified equity funds ended with negative returns. Still, a handful of them that took a little more mid-caps than their peers, managed to reverse the category trend.

SBI Bluechip, which was among the top funds in the large and diversified equity category was a key performer in our list, in this category. We would call it a relatively aggressive fund in this category. Besides, funds such as Franklin India Prima Plus (which we added a quarter ago), BNP Paribas Equity and Mirae Asset India Opportunities did quite well, and their contrarian calls, that ended as timely ones (and not aggressive exposure to mid-caps), helped them.

Kotak Select Focus too did well, its concentrated bets managing to deliver. Axis Equity and UTI Opportunities were the ones to conspicuously lag behind. A few missed calls, besides staying true to their market cap, did not help them in a large-cap unfriendly year.

Tax-saving funds too, by and large, delivered well; their flexibility to move between large and mid-caps being fully utilised by them with deft shifts across quarters. It also helps that these funds have less redemption pressure as you invest in them for tax-saving purpose with a lock-in.

In all, if you take out the mid-cap funds, and see the large and diversified category (including ELSS), their returns were 0.6 per cent. You could call it flat, but better than the fall in the Sensex, BSE 100 or the BSE 500.

Our mid-cap funds, although performing well, did not have it that easy, and managed out-performance of just 0.5 percentage points over the S&P BSE Midcap. This is because we mostly stick to mid-cap funds that have very limited, or no exposure to small and micro-cap stocks. Barring Franklin India Smaller Companies Fund (whose market cap is still larger than other small-cap funds), our Select Funds list has mid-cap funds with a good dose of large mid-caps and emerging large-caps. As opposed to this, the S&P BSE Midcap has a good dose of smaller market cap companies.

Similarly, our mid-cap funds also marginally underperformed the category average as a result of a number of funds that invest in smaller-cap companies. These funds delivered higher returns as small-caps outperformed mid-caps.

While the outperformance of funds such as SBI Magnum Midcap, Mirae Asset Emerging Bluechip or Franklin India Smaller Companies did not surprise us, given their focus on mid to small-sized companies, BNP Paribas Midcap’s outperformance was rather conspicuous. That the fund managed this without dipping into smaller companies was evidence to its deft stock picking skills, contrarian as they may seem.

Overall, we did not make too many changes in the equity space in 2015. We don’t think we missed too many opportunities in this space. If we chose to miss some (in the mid-cap space), it was a conscious decision. Still, we could have brought in a boring fund like Franklin India Prima Plus earlier and perhaps just waited it out with ICICI Pru Top 100 (whose performance is improving).

We think it is important, at this juncture, not to get excited by the mid-cap outperformance over large and diversified funds. We believe large and diversified funds have sufficient opportunities to pick quality bluechip companies at reasonable valuations. Hence, return potential from this point may be better.

Debt funds

In the debt fund category, chances are that you will see plenty of funds that have delivered higher than our 6-fund debt-long term fund list. This could have been either because the others were high on gilt, and took long duration calls, or instead took high credit risks. We have stayed away from these extremes. Our funds take some duration calls (Birla Sun Life Dynamic Bond, UTI Dynamic Bond), and others depend on a mix of good credit and improving credit themes to generate income accrual.

We believe the latter is a more sustainable way to generate returns. When we took the entire income fund universe and compared our funds, we saw that the chart toppers in this universe were those with higher credit risk (corporate bond opportunity funds).

We believe these funds are not suitable for all investors, and need some understanding of credit risk. While we may review those funds separately, we would hesitate to introduce them as a part of a core portfolio.

Leaving that aside, our funds still underperformed the Crisil Composite Bond Index. That this index holds over a third in long-term gilt did not help our cause as we do not take in long-term gilt funds for we think investors need active entry and exit strategies for those. The limited exposure that our income/dynamic bond funds hold in gilt (and that too with medium average maturity) generated returns, but not sufficient to beat the index. We are not too worried about this as we think the funds can beat their index over 3 years or more, with their current strategy.

Do note that the best in debt funds is not over for two reasons – more rally as a result of dip in interest rates is expected and this will deliver capital appreciation. The corporate credit story (deleverage and improvement in rating) is yet to unravel itself, and will likely deliver relatively more sustained returns than the interest rally.

Debt funds, as a part of your long-term debt allocation, is a must. 2015 demonstrated why your portfolio is better off with asset allocation.

What’s in it for you

If you are going to ask whether you should shuffle your portfolio based on the changes in our Select Funds list, the answer is ‘no’. Your portfolio would have been built with a specific goal, purpose, time frame, or risk profile; and many of the funds we exit are not really ‘sells’. The Select Funds list makes an endeavour to feature good funds at that point in time. Hence, for investors entering afresh, it is a good list to refer. It is not a portfolio by itself.

When we write to you about our quarterly reviews, we make it clear whether a fund that exits our list needs to be exited, or is a ‘hold’. Over and above this, when in doubt, you should talk to our advisors, who will customise the Select Funds list to suit your specific need.

Our suggestion to you would be to use our portfolio review service (through our advisors) more actively, not just to choose funds, but even to decide when you want to exit something. This way, you will have some assurance on whether you are not making the wrong moves, and you can continue to hold an optimal portfolio.

2016 would be an interesting year that will very likely separate the wheat from the chaff in stocks. Earnings growth and pick up investment activity in companies will show who is really beginning to move. Fund managers would have to pick stocks alike and we reckon a return differential between funds would be hard unless fund managers spot ugly ducklings early on, or bet on dark horses. Either which way, there are interesting times ahead!

Happy investing and a very prosperous new year to you!

Hi,

http://www.fundsindia.com/select-funds

Can you pls add a column for 10 yr returns in the above page? i know for some funds it may not applicable, but having it for some funds for which its applicable will give very good view for long term investors like me.

Thanks,

Suhas

Hello Suhas, This particular article is merely a 1-year round-up and not meant to discuss long-term performance. You can check 10-year returns online in valueresearch and other portals. thanks, Vidya

I have read many articles not favoring HDFC Equity and Top 200 or de-rate them for recent years. They have been best performers for many years. Do you still recommend them if someone has horizon of 25 years via SIP or move to other funds.

Hello Rajni, Both these funds are volatile in the short to medium term but will likely egenrate market beating returns over the time frame you are talking of. Hence, you can continue. Vidya

A very well researched and nicely written story . My compliments to the author . My view is that select mutual funds delivered far better than large cap equities – many of then like ITC and Tata Steel down in the dumps for instance . For me personally , my own investment in SBI MF’s Small and Micro Fund turned out be a particularly good investment , moving upwards all the time 🙂

A very well researched and nicely written story . My compliments to the author . My view is that select mutual funds delivered far better than large cap equities – many of then like ITC and Tata Steel down in the dumps for instance . For me personally , my own investment in SBI MF’s Small and Micro Fund turned out be a particularly good investment , moving upwards all the time 🙂

A very well researched and nicely written story . My compliments to the author . My view is that select mutual funds delivered far better than large cap equities – many of then like ITC and Tata Steel down in the dumps for instance . For me personally , my own investment in SBI MF’s Small and Micro Fund turned out be a particularly good investment , moving upwards all the time 🙂

Is the current list of select funds in dashboard final for first quarter of 2016 or there is going to be a change ?

I think it would be more prudent to research performances of funds during “crisis Years” when markets had a sharp fall, That period shows the ability and deftness of a FUND MANAGER and the FUND performance. Would this be correct Ms Vidya Bala?

Is the current list of select funds in dashboard final for first quarter of 2016 or there is going to be a change ?

Hi,

http://www.fundsindia.com/select-funds

Can you pls add a column for 10 yr returns in the above page? i know for some funds it may not applicable, but having it for some funds for which its applicable will give very good view for long term investors like me.

Thanks,

Suhas

Hello Suhas, This particular article is merely a 1-year round-up and not meant to discuss long-term performance. You can check 10-year returns online in valueresearch and other portals. thanks, Vidya

A very well researched and nicely written story . My compliments to the author . My view is that select mutual funds delivered far better than large cap equities – many of then like ITC and Tata Steel down in the dumps for instance . For me personally , my own investment in SBI MF’s Small and Micro Fund turned out be a particularly good investment , moving upwards all the time 🙂

I think it would be more prudent to research performances of funds during “crisis Years” when markets had a sharp fall, That period shows the ability and deftness of a FUND MANAGER and the FUND performance. Would this be correct Ms Vidya Bala?

I have read many articles not favoring HDFC Equity and Top 200 or de-rate them for recent years. They have been best performers for many years. Do you still recommend them if someone has horizon of 25 years via SIP or move to other funds.

Hello Rajni, Both these funds are volatile in the short to medium term but will likely egenrate market beating returns over the time frame you are talking of. Hence, you can continue. Vidya