“It doesn’t feel like a 7.5 per cent growing economy.” – This is probably the most fashionably spelt statement in the institutional investor segment at this point in time. And with IIP numbers, especially on the capital goods front, not showing much of a revival, the hope of a private capex spending simply remains wishful.

This, together with reforms continuing to act as a drag, has meant continued pressure on the earnings of companies. Or is it? Not entirely. Be it the core production numbers – those that feed into real industrial activity, or the other macro indicators such as transport or credit, all point to a steady recovery. Their key takeaway is this: failed monsoons, reforms drag, and of course, lack of private capex spending may not really pull down the pick up of economic activity. And that is a sign of a turnaround for the corporate story.

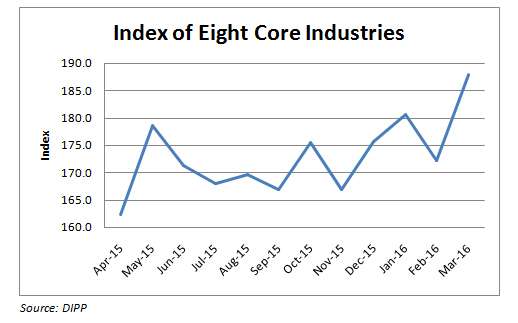

Core industries

Let’s dive head-on into numbers that matter the most. What numbers matter most? It is the core production numbers that actually feed into other industrial activity. This is the ‘Index of Eight Core Industries’. This is an index that is less tracked than the Index for Industrial Production, and accounts for 38 per cent of the IIP. Also, it is often a lead indicator for the activity in other manufacturing sectors in the economy.

This index consists of production data for coal, crude oil, natural gas, petroleum refinery products, fertilisers, steel, cement and electricity production. As can be seen in the graph below, while monthly dips and V-shaped recoveries are seen, the broader trajectory has clearly been up, especially after hitting a low in November 2015. Positively, production of key industries such as steel, coal, cement and electricity have seen a jump ranging from 11 per cent -31 per cent between November 2015 and March 2016. The only sectors that have remained flat – crude oil, fertilisers and natural gas – are known to have capacity constraints.

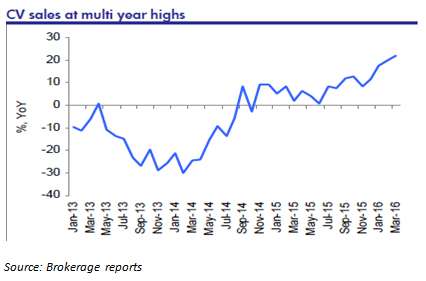

Transport

Another important indicator of economic activity is the pick in the sales of commercial vehicles. More demand for transport vehicles speaks volumes of production and consumption activity. The data below shows a steady pick in the demand for commercial vehicles.

Not to be outdone, passenger car sales (more an indicator of consumption strength), grew every quarter (compared with a year ago) in FY-16, except for the last quarter of March 2016, when there was a soft drop over a year ago.

People were travelling in hoards too (an indicator of business climate). For the quarter ending March 2016 alone, passengers who flew by air rose by 24 per cent to 230 lakh (source DGCA). And this double digit growth story has played out from the September 2015 quarter.

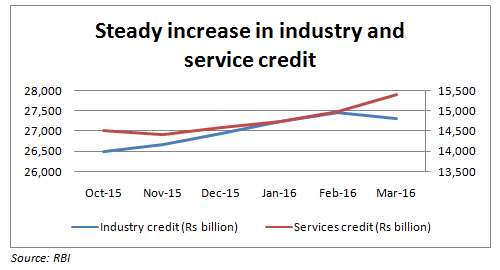

Credit

What are banks doing with their money? Credit growth (money lent by banks), especially for industrial credit, has been lukewarm, no doubt. But it has not been bad, if one sees the lending month after month in recent months. The graph below shows – except for March 2016, when there was a marginal dip – there has been a slow and steady pick up in industrial credit. Service credit has been relatively better, seeing no dips post November.

We knew anecdotally (going by the increased lending of mutual funds and other institutions through debt papers) that companies were borrowing more in the debt market. We took one of the short-term borrowing options available to companies namely, commercial papers, to see the growth. The amount outstanding, as borrowed money jumped close to 2 times between March 2015 and now, is Rs. 3,406 billion. But this is just the due; money lent would be multiple times that since this is typically short-term lending.

More interestingly, lending rates, which were in the range of 7.44-14.92 per cent in March 2015, have come all the way down to 6.84-11.22 per cent. Clearly, not only are companies borrowing, they are borrowing at lower costs, at least for their short-term needs such as working capital. While they may be refinancing some of their high cost loans, the jump also means their working capital requirements (from improved capacity utilisation) could be higher.

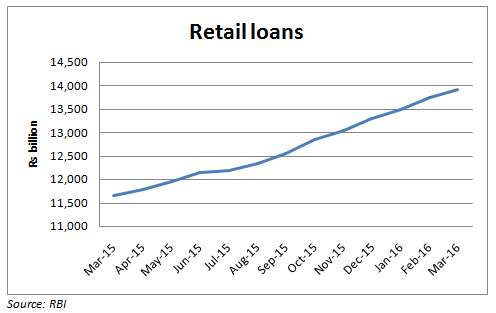

But the feel good story comes from our own hands! Personal loans, be it homes, consumer durables, vehicles, or your credit card outstanding are up by 19 per cent in the past one year (up to March 18, 2016). Clearly, the consumption slowdown story notwithstanding, we have been spending to rev up the economy’s growth.

Still, if one believes that this does not feel like a roaring economy – true, it certainly is not. None of these is actually yet to reflect in the earnings growth of companies that are already under tremendous expectations from market valuations. Why is this so? Be it the core production numbers or CV sales pick up or credit pick up, all of these are but initial signs of pick up in activity. They feed into the rest of the production activity.

For instance, CV sales happens in anticipation of higher volume of goods to be transported. Higher credit off-take would be a sign of deployment of money by companies into their business. Hence, it is a precursor. But what about the core production numbers? Why are they not reflected in Corporate India’s growth? They have to, to some extent; but there is no inflation to offer a quick boost to the top line of companies. None of these core production activities had pricing power. Companies have been managing earnings expansion through lower input costs with volume just turning around.

Hence, the wait will have to be longer for volumes to push the sales of Corporate India. The next swing in equity markets could, therefore, come from the top line growth, if the core data remains what it is.

But then, seldom does the investing world wait for numbers. It looks for direction. If these directions provide confidence for a recovery, then you should probably be investing now, not later.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Fantastic writeup Vidya. I am a recent investor in Funds India but I think I made the right decision despite apprehensions about investing online.

Consumer behaviors are indicators of economy upslides but I would say the bottom line for most consumers like me is do I invest at a time when the overall market is flat or apprehensive of taking on new commitments?

That being said, I do see value in what your article points out and do hope that the road to Corporate recovery in India is a lot faster than predicted.

Thanks for your insights! As a non-finance lad, its nice to understand the general climate in the financial sector through your writeups. Kudos to you guys!

Hello Abhishek, Thanks! to remove apprehensions and let investors know why you should be investing in volatility, we did a few stories. One of them is here with link to the other as well. https://blog.fundsindia.com/blog/advisory/fundsindia-strategy-the-time-to-invest-more-and-where-to-invest/8836

thanks,

Vidya

Which Equity fund might yield the best of profits in the upcoming 5 year span and is worth investing ?

Excellent write-up Vidya. I am a new investor in FI since April 2016 and based on the FI recommendations, I started investing in MFs. Though, initially in the first two weeks almost all schemes were in green but are not so now….however, I have been regularly reading very informative articles by you and that gives me the courage not to panic but to remain invested, go through the ups and downs and at the end see some favourable results and value to the hard-earned money that is invested on belief and trust on my advisors, ably guided by specialists like yourself.

Though, I am from a non-financial background, the content, systematic explanation of various factors and the value that lies below the facts (which we as investors should grasp) in your articles are very clear and concise and encourages me to dig further for such reading materials.

Keep up the good work…in fact, from day one, I have experienced excellent support and assistance from the FI team and with confidence I am able to say that my selection to go with FI as my investment vehicle was never wrong..and look forward to a lifetime relationship with FI.

Best regards and wishes to all at FI

Hello Sir,

Thank you for the kind and encouraging words. We hope to continue to provide support and value. rgds. Vidya

Which Equity fund might yield the best of profits in the upcoming 5 year span and is worth investing ?

Excellent write-up Vidya. I am a new investor in FI since April 2016 and based on the FI recommendations, I started investing in MFs. Though, initially in the first two weeks almost all schemes were in green but are not so now….however, I have been regularly reading very informative articles by you and that gives me the courage not to panic but to remain invested, go through the ups and downs and at the end see some favourable results and value to the hard-earned money that is invested on belief and trust on my advisors, ably guided by specialists like yourself.

Though, I am from a non-financial background, the content, systematic explanation of various factors and the value that lies below the facts (which we as investors should grasp) in your articles are very clear and concise and encourages me to dig further for such reading materials.

Keep up the good work…in fact, from day one, I have experienced excellent support and assistance from the FI team and with confidence I am able to say that my selection to go with FI as my investment vehicle was never wrong..and look forward to a lifetime relationship with FI.

Best regards and wishes to all at FI

Hello Sir,

Thank you for the kind and encouraging words. We hope to continue to provide support and value. rgds. Vidya

Fantastic writeup Vidya. I am a recent investor in Funds India but I think I made the right decision despite apprehensions about investing online.

Consumer behaviors are indicators of economy upslides but I would say the bottom line for most consumers like me is do I invest at a time when the overall market is flat or apprehensive of taking on new commitments?

That being said, I do see value in what your article points out and do hope that the road to Corporate recovery in India is a lot faster than predicted.

Thanks for your insights! As a non-finance lad, its nice to understand the general climate in the financial sector through your writeups. Kudos to you guys!

Hello Abhishek, Thanks! to remove apprehensions and let investors know why you should be investing in volatility, we did a few stories. One of them is here with link to the other as well. https://blog.fundsindia.com/blog/advisory/fundsindia-strategy-the-time-to-invest-more-and-where-to-invest/8836

thanks,

Vidya