With equity markets scaling new peaks, those of you who are already invested in equity funds, or are new to equities, may be thrilled. Thanks to the move, you may wish to make hay while the sun shines by setting short-term goals for the equity investments you just started. That is where your investment mistakes may begin.

This week, let’s just revisit some investment basics that are simple, effective and not risky, reminding us to stick to our investment habits at all times.

Mistake #1: Going short-term with equities and long-term with deposits

For most of you who are testing waters with equities, it might seem like you’re playing it safe by taking short-bets in equities and building wealth for the long-term with fixed deposits. There begins the most inefficient, inflation-hit way of building wealth.

As a result, investing for long-term goals such as your children’s education or your own retirement may be happening through Recurring Deposits (RDs), while you might be planning to buy a home next year by investing in equities.

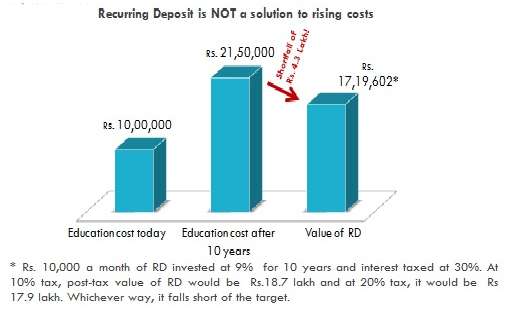

Just take a look at the image below on how investing in RDs may not fetch you the required amount given the surging cost of education (inflation at 8%).

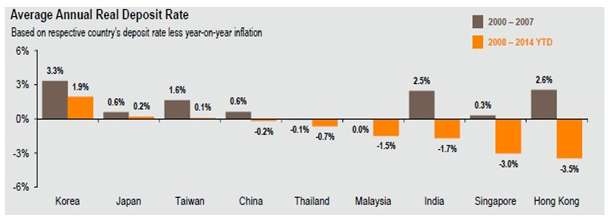

Besides, data (below) from JP Morgan AMC suggests that the ‘real interest rate’ in India – that is, your deposit rate post inflation, has been negative since 2008. Hence, to believe that your investment is safe, when it cannot fetch you what you need, is equivalent to losing money in these ‘safe options’.

On the other hand, it does not help to invest in equities for the short term. Had you invested in equities in late 2007 or in the beginning of 2008, you may have lost anywhere between 50-60% in equity funds in a year’s time.

If your short-term goal depended on this investment, your goals would have gone for a toss. Added to it, you may close your doors to this asset class, dubbing it as risky and unpredictable.

But the truth remains that equities have time and again shown to deliver over the long term. 10-year or 15-year rolling returns of equities have never been negative.

Hence, if you have long-term goals, allocate some equities through equity funds and asset balance it with debt funds or other debt options. Avoid using equity options for short-term goals.

Mistake #2: Doubting the ability of SIPs

Even if you did start off investing for the long term, some of you may be doubting the ability of SIPs to perform when markets keep hitting new highs. This may tempt you to stop SIPs.

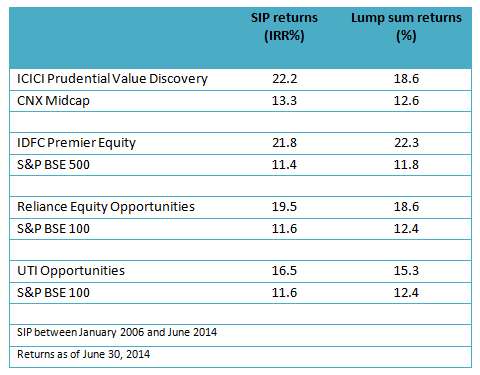

Others may believe that they are at a peak and may not wish to start SIPs now, waiting for the market to fall. Just take a look at the data below that shows how SIPs made in funds from our ‘Select Funds‘ list from January 2006 till date have performed.

This investment would have seen a massive rally from 2006 till the beginning of 2008 (that means you invested continuously in an up-trending market). But then, you would also have averaged well in 2008 and 2011 (when the markets fell).

Over the long term, as markets invariably go through cycles, your SIPs tend to automatically average at lower costs and deliver well.

Similarly, even if you had started your SIP in the market peak of January 2008 but continued, no harm done. Your SIP returns, had you continued till June 2014, would have been in the range of 16-25% IRR for established funds.

This establishes the fact that SIPs are your best bet if you want to build wealth with minimal disruptions.

Mistake #3: Chasing fund returns, chasing asset returns

If you are picking equity funds based on the one-year chart topper list, you are buying yourself trouble. Many funds that were underperformers or stuck with stocks that they could not exit may have seen a rally in such stocks during a momentum move (that typically lifts the good and bad stocks) resulting in their NAVs inflating.

If you had picked one such fund, chances are that you will see its performance slip in the next year or two.

Consistency always pays. Look for funds (check out our Select Funds list) that have performed across market cycles, or check with your advisor on such funds.

The idea of investing in equity funds is to hold for the long term; shuffling the portfolio because you ended with poor performers, or because you are keen to have only the chart toppers will not help you build wealth.

Similarly, avoid the tendency of running behind asset classes that you think will deliver. More often than not, only after the asset class delivers would you be entering.

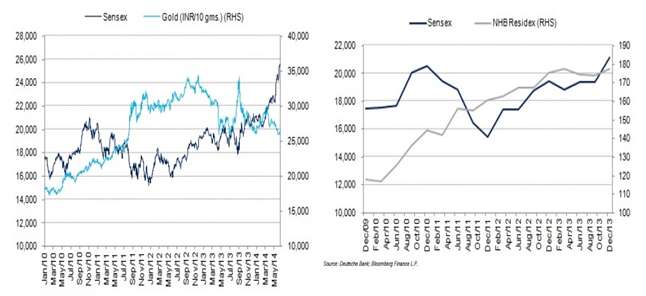

Look at the performance of the Sensex with the National Housing Bank index for residential prices – NHB Residex, and also against gold. Would you have been able to enter gold at the right time and exit by 2012?

Or would you have been able to time your entry into real estate in 2011? Instead of chasing asset classes, consider allocating across asset classes. That way, at all points, you would have some of them delivering.

In all, whether it is a bull market or a bear market, you simply need to follow these commandments:

– Risks, especially when taken with quality equity funds, usually pay off in the long run as suggested by historical data. Be willing to take some risks for the long haul and play it safe for the short term, market sentiments notwithstanding. If you can do that with real estate, there is no reason why you cannot assume equity risks.

– Run an SIP based on the time frame of your goal and do not stop the SIP until you are closer to your goal. Even if you consider switching funds, continue the SIP in the changed fund. You never know what averaging opportunities you miss on, when you stop SIPs.

– Give asset allocation its due and do not be lured by returns in one particular asset class at one point in time. Chasing returns is a never ending game and seldom favours you. Entering gilt funds in 2013 and burning your hands, or buying gold based on its high double-digit returns (2011-12) and then seeing them fall later are grim reminders of the result of chasing asset returns.

Hi Vidya,

Nice article. i have one question.

(1) If your financial goals are 15 to 18 years away how much allocation we can give for equity? what is your opinion on giving 100% allocation to equity during initial period?

(2) My portfolio consists of equity mutual fund,+ ppf+ LIC policies. My debt component is PPF and LIC policy. I know LIC policies are not good investment product but i’m not surrendering it because i’m considering it as my debt allocation and more overover my policy will be expairing in few years time.

My question is how do we Rebalanc portfolio if one assest class moves up ? E.g equity investments now.

(3) Is rebalancing of portfolio is required if your financial goals are more than 15 years away? or just leave the investment as it and review only the performance periodicaly?.

Thanking you in advance. Would truly appreciate your help.

Warm regards

Shaji Unni

Hello Shajji,

1. your call depending on your ability to take a fall. We do not advocate it.

2. You have the answer. Having a ‘debt portfolio’ made of traditional insurance policy does not allow rebalancing simply because you would not even know the value of your debt component. In general, asset rebalancing can be done by an annual review and if the asset classes move by say more than 5 percentage poitns or so from your orgl. allocation, you can sale a part and add to the asset class which fallen. This is done done with the help of technology in our ‘Smart Solutions’. Just a click by the investor is enough to rebalance.

3. Rebalancing has shown to generate a couple of percentage points more than a portfolio not rebalanced over 5-10 year time frames.

thanks, Vidya

Hi, with the change in debt funds tax rate going upwards for LTCG and the holding period trebled, is it still advisable to hold on to the exsting investement, or exit ?

Hello Sachin, It depends on what category of funds you hold. If you hold income or other long-term debt funds, their holding period is anyway meant to be at least 3 years and when rates fall, they will likely generate double digit returns. If you have short-term debt funds that you wish to redeem in the near term, then unless you need to money, you may consider holding it for longer (as again a rate fall will trigger returns). But if you have liquid or ultra short term funds, then in any case you would only be mostly holding short term and have STCG even now.thanks, Vidya

I invested in in liquid, ultra short term and short term debt funds (growth option )as they are giving better returns than bank FDs post tax. I can wait for 3 years. Is there any chance of their giving less returns in the next 3 years ,if the general interest rates go down ?

what should I do now?

Hello Murthy, When general interest rates fall, FD and savings rate will also fall. Hence, what you hold will continue to give better returns than the traditional options, although they may not give the current high returns. Also, by waiting for 3 years, since you will get indexation benefit, tax impact will be low or nil. thanks, Vidya

Hi Vidya,

Nice article. i have one question.

(1) If your financial goals are 15 to 18 years away how much allocation we can give for equity? what is your opinion on giving 100% allocation to equity during initial period?

(2) My portfolio consists of equity mutual fund,+ ppf+ LIC policies. My debt component is PPF and LIC policy. I know LIC policies are not good investment product but i’m not surrendering it because i’m considering it as my debt allocation and more overover my policy will be expairing in few years time.

My question is how do we Rebalanc portfolio if one assest class moves up ? E.g equity investments now.

(3) Is rebalancing of portfolio is required if your financial goals are more than 15 years away? or just leave the investment as it and review only the performance periodicaly?.

Thanking you in advance. Would truly appreciate your help.

Warm regards

Shaji Unni

Hello Shajji,

1. your call depending on your ability to take a fall. We do not advocate it.

2. You have the answer. Having a ‘debt portfolio’ made of traditional insurance policy does not allow rebalancing simply because you would not even know the value of your debt component. In general, asset rebalancing can be done by an annual review and if the asset classes move by say more than 5 percentage poitns or so from your orgl. allocation, you can sale a part and add to the asset class which fallen. This is done done with the help of technology in our ‘Smart Solutions’. Just a click by the investor is enough to rebalance.

3. Rebalancing has shown to generate a couple of percentage points more than a portfolio not rebalanced over 5-10 year time frames.

thanks, Vidya

Hi, with the change in debt funds tax rate going upwards for LTCG and the holding period trebled, is it still advisable to hold on to the exsting investement, or exit ?

Hello Sachin, It depends on what category of funds you hold. If you hold income or other long-term debt funds, their holding period is anyway meant to be at least 3 years and when rates fall, they will likely generate double digit returns. If you have short-term debt funds that you wish to redeem in the near term, then unless you need to money, you may consider holding it for longer (as again a rate fall will trigger returns). But if you have liquid or ultra short term funds, then in any case you would only be mostly holding short term and have STCG even now.thanks, Vidya

I invested in in liquid, ultra short term and short term debt funds (growth option )as they are giving better returns than bank FDs post tax. I can wait for 3 years. Is there any chance of their giving less returns in the next 3 years ,if the general interest rates go down ?

what should I do now?

Hello Murthy, When general interest rates fall, FD and savings rate will also fall. Hence, what you hold will continue to give better returns than the traditional options, although they may not give the current high returns. Also, by waiting for 3 years, since you will get indexation benefit, tax impact will be low or nil. thanks, Vidya