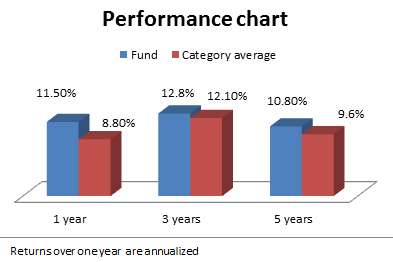

If you want to earn FD-plus returns with a portfolio of high-quality debt and very marginal exposure to equity, then Birla Sun Life MIP II Savings 5 (Birla Savings 5) is right up your alley. With a 3-year annualised return of 12.7 per cent, and a 5-year return of 10.8 per cent, the fund managed to beat its category average by 70-100 basis points. That is a big deal considering that it has, on an average, held less than 10 per cent in equity as opposed to the 20-25 per cent holding of most peers.

This could also be a good time to be in the fund, considering that the rally in gilt may continue for some more time.

The fund and its suitability

Birla Savings 5 is a debt-oriented fund but with more debt holding than its peers. It invests 85-90 per cent of its assets in debt and rest in equity and cash. It is typically compared with funds in the MIP (monthly income plan) category.

Birla Savings 5 is part of FundsIndia’s Select Funds list. Some of you have asked us as to why this fund is part of the list when its returns (depending on the time-frame they are looking at) are often lower than some of the peers. Our answer has been that the fund delivers returns commensurate with the risk it has taken. And the risk it takes is far lower than most peers, given the fund’s low exposure to equity. We will explain how this strategy panned out for the fund later but for now, suffice to know this fund is ideal for low-risk investors looking for FD-plus returns with a 3-year time frame.

If you opt for this fund, go with the growth option. If you wish to generate income, start a systematic withdrawal plan after (preferably) three years, instead of depending on the dividend pay-out option; in order to be tax efficient.

Performance

Birla Savings 5 has a risk-adjusted return (measured by its Sharpe Ratio) that is among the best in its category, next to its sister fund Birla Sun Life MIP Wealth 25 and UTI MIS Advantage, when rolled daily for 1-year returns over the last three years.

The most noteworthy performance point for this fund is its ability to contain downsides well, a job that this category of funds ought to do. Over the last 10 years, 1-year returns rolled daily suggests that the fund had negative returns (of -0.15 per cent) on just one occasion, on January 4, 2010, as a result of unfavourable gilt returns and of not having ridden the equity wave due to its low exposure. Except for this, the fund never slipped into the red for any 1-year time-frame, at any point in these 10 years. As opposed to this, peers such as Franklin India MIP or HDFC MIP LTP had negative 1-year returns 4-5 per cent of the times. Peers fell in the range of 11-18 per cent when they went into the negative zone.

Over 3-year time-frames too (in the last 10 years), the fund’s performance has been good. With a rolling 3-year average return of 9.6 per cent annually, the fund bettered its sister fund Wealth 25 (9.4 per cent) marginally, with far lower risks and far better minimum returns.

As investors, you will have to compare the fund’s average return of 9.6 per cent over the last 10 years with those offered by 3-year FDs. According to RBI data, such returns would be about 8 per cent if you reinvested the money every three years, and even if you chose longer period FDs. And remember, tax would eat up a chunk of your FD returns, while MIPs will enjoy capital gains indexation benefit.

Portfolio

In the past two years, Birla Saving 5 has had less than 10 per cent of its holdings in equities. Of its current 10 per cent holding in equity, about 6 per cent is in mid-cap stocks. Still, this is spread over 21 stocks (out of a total of 35 stocks) and may not hurt even in the event of a mid-cap bubble.

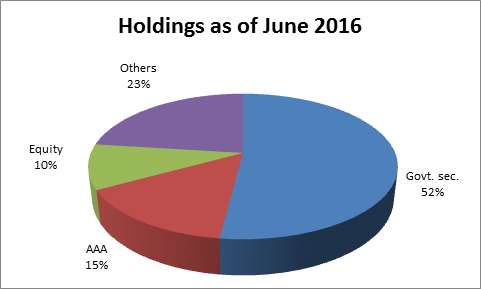

The fund has mostly held gilts with an average maturity of over 10 years. Currently with an average maturity of 12.8 years (as of June 2016), the fund has gained handsomely from the gilt rally, generating 9 per cent returns year to date as opposed to a category return of 7.1 per cent.

The fund’s overweight position in gilt and low to nil holdings in equities paid off handsomely in the calendar year 2008. Even as the equity market took a hit that year, it was a period when gilt outshone. With little or no exposure in equities that year, the fund delivered a handsome return of 28.5 per cent that year (the CRISIL 10-year gilt index delivered 27 per cent, indicating that is where the returns came from). This, when its peers fell between 1-12 per cent!

The year 2008 was a classic example of how, even with equity exposures as low as 20-25 per cent (the average holding of MIP funds in equities), MIP funds can be vulnerable to equity market falls. As investors, you will do well to know that MIP funds as a category do not come without risks. Funds such as Savings 5 would give you relatively low volatility, if you are content with the FD-plus returns.

The fund has a compact AUM of Rs. 247 crore.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

I’m investing 5k every month on PPF but year to year interest rate is coming down. Can I stop PPF and choose this ?

Shunmuga Priya – this fund is not a tax-saving option under Sec 80C if you are investing in PFF to save tax. It will give you FD-beating returns.

I’m investing 5k every month on PPF but year to year interest rate is coming down. Can I stop PPF and choose this ?

Shunmuga Priya – this fund is not a tax-saving option under Sec 80C if you are investing in PFF to save tax. It will give you FD-beating returns.

I’m investing 5k every month on PPF but year to year interest rate is coming down. Can I stop it and choose this ?

Very well explained – the merit of this plan is clearly brought out! The observation that MIPs with just 20-25% equity are at risk of giving negative returns during an equity market fall (as in 2008) is interesting. It makes me think about the role of equity-oriented balanced funds which have over 65% in equity. These will limit the returns of the fund when the market is good for equities owing to the relatively high percentage of debt holdings in the fund (as compared to pure-equity funds), and if they are not really that effective in containing the downsides in a bad market for equities, will a portfolio not be better off having only pure-equity funds and debt funds (or MIPs with low volatility like this)?

Karthik, very good point. But then, that is the beauty of equity isn’t it. It can be very unishing over the short term but exceedinly rewarding over the long term – even if one;s allocation is 65-70% – we have seen that good balanced funds actually even beat the category average of diversified equity funds simply because they are less volatile. Balanced funds will of course fall in bear markets. But they fall at least 5-8% points lesser than pure equity. Since they don’t fall hard, when the recoup, they find it easier. Hence long term returns actually favour balanced funds, despite the fact that their returns might seem capped in the short rallies. MIPs are typically considered for 3 year periods or for low-risk income generation purposes. There, low volatility is key. Hence, equity should not cause damage there..it should only add some extra returns.

thanks, Vidya

I’m investing 5k every month on PPF but year to year interest rate is coming down. Can I stop it and choose this ?

Very well explained – the merit of this plan is clearly brought out! The observation that MIPs with just 20-25% equity are at risk of giving negative returns during an equity market fall (as in 2008) is interesting. It makes me think about the role of equity-oriented balanced funds which have over 65% in equity. These will limit the returns of the fund when the market is good for equities owing to the relatively high percentage of debt holdings in the fund (as compared to pure-equity funds), and if they are not really that effective in containing the downsides in a bad market for equities, will a portfolio not be better off having only pure-equity funds and debt funds (or MIPs with low volatility like this)?

Karthik, very good point. But then, that is the beauty of equity isn’t it. It can be very unishing over the short term but exceedinly rewarding over the long term – even if one;s allocation is 65-70% – we have seen that good balanced funds actually even beat the category average of diversified equity funds simply because they are less volatile. Balanced funds will of course fall in bear markets. But they fall at least 5-8% points lesser than pure equity. Since they don’t fall hard, when the recoup, they find it easier. Hence long term returns actually favour balanced funds, despite the fact that their returns might seem capped in the short rallies. MIPs are typically considered for 3 year periods or for low-risk income generation purposes. There, low volatility is key. Hence, equity should not cause damage there..it should only add some extra returns.

thanks, Vidya

How do I interpret these: “7.59% GOI 2029” and “8.13% GOI 2045”? These are two of many instruments that Wealth 25 is holding in its portfolio.

I am invested in Wealth 25 and HDFC MIP LTP, and my investment horizon is long. Should I consider moving one of these to Savings 5?

Hi Vijay 7.59% GOI 2019 means interest rate (coupon rate) of 7.59% and maturity of 2029. It does not mean the fund will hld it till 2029. They may sell anytime and gain in the market, if there are opportunities. In general, longe the maturity, highe rtheswings in prices when interest rates move. In other words, longer dated gilts make more returns or more losses (depending on rate cycle) and are riskier. You need not move based on this. If you need lower exposure to equity than the other MIP funds, use Savings 5. thanks, Vidya

FYI, the credit profile of this fund has changed considerably. Over 80% of its debt portfolio is now in bonds rated AA and below, according to MorningStar. I think the suitability of this fund should be reassessed.

Karthik, very true. We will have to redo this article as it is an old one. We will cover it again. thanks, Vidya

FYI, the credit profile of this fund has changed considerably. Over 80% of its debt portfolio is now in bonds rated AA and below, according to MorningStar. I think the suitability of this fund should be reassessed.

Karthik, very true. We will have to redo this article as it is an old one. We will cover it again. thanks, Vidya

How do I interpret these: “7.59% GOI 2029” and “8.13% GOI 2045”? These are two of many instruments that Wealth 25 is holding in its portfolio.

I am invested in Wealth 25 and HDFC MIP LTP, and my investment horizon is long. Should I consider moving one of these to Savings 5?

Hi Vijay 7.59% GOI 2019 means interest rate (coupon rate) of 7.59% and maturity of 2029. It does not mean the fund will hld it till 2029. They may sell anytime and gain in the market, if there are opportunities. In general, longe the maturity, highe rtheswings in prices when interest rates move. In other words, longer dated gilts make more returns or more losses (depending on rate cycle) and are riskier. You need not move based on this. If you need lower exposure to equity than the other MIP funds, use Savings 5. thanks, Vidya