You might have heard people talking about the wonders of compounding. When talking about the benefits of long term investments, investors are often told that over a long time, the compounding effect leads to higher accumulation. However, time and again we also come across articles claiming there is no compounding in mutual funds. They say anyone who talks about the wonders of compounding is lying. Why does this dichotomy exist and why only in case of mutual funds? Let us try to understand.

Understanding compounding

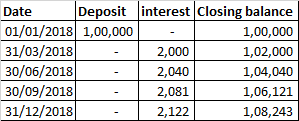

To start with, let us first talk about how compounding works in banks. When you put money in a bank FD, the interest rate you will get is stated in annual terms. However, for a cumulative FD, the interest is credited quarterly. This means that if the stated rate is 8% p.a., then the actual return is slightly higher as it compounds on a quarterly basis. Here is a simple illustration:

As you can see from the illustration, you have gained Rs. 8,243. However, at 8%, you should have gained only Rs. 8,000. Thus compounding has led to extra gains of Rs. 243.

This is the general understanding of compounding, where the interest is actually credited into your bank account every so often. The reason some people say there is no compounding in mutual funds is because there is no returns being credited to your account separately.

How do MF Returns compound?

So then, are people lying when they talk about the benefits of compounding in mutual funds?

Not really. What banks do with your fixed deposits is actually just one way how compounding works. But that is not the only way in which compounding can work. Because compounding does not mean interest getting credited into your account at regular intervals. Compounding refers to the increase in the value of an asset due to the returns earned on both the principal as well as the previously accumulated returns.

To state it more simply, compounding refers to a situation where you earn interest or returns on interest and returns which you have already earned. Looking at it this way, it is not hard to see how mutual fund returns are compounded.

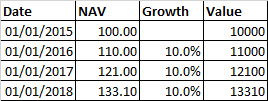

Let’s look at this simple example. It’s a hypothetical fund which has given 10% return every year. You made an investment on 1st January, 2015.

As you can see from the illustration, you earned Rs. 10,000 in the first year. The fund’s value, therefore, was Rs. 11,000 at the end of the first year. The 10% return of second year was on this entire Rs. 11,000, resulting in a net gain of Rs. 1,100. The return of the first year got compounded because your fund’s value had already increased by that amount. Same thing happens in the third year, resulting in a net gain of Rs. 3,310 in three years.

When you put money in fixed deposit, the value of the FD remains constant for three months, then the interest is credited and the value increases. Future interest is calculated on this total amount resulting in compounding. However, in mutual funds, whatever returns you earn or losses you make are adjusted from the value of your holdings on a daily basis. You don’t have to wait for the returns to be credited to your account, it happens automatically every single day. Hence the returns actually compound on a daily basis.

Understanding CAGR

Keep in mind though, that mutual fund returns are not expressed in daily compounded terms. It is shown as compounded annual growth rate or CAGR. This, again, is a way of showing returns which makes it intuitive and comparable. This is also a global standard of and facilitates comparison across asset classes and geographies.

Take this example. You are told you will earn 8% per year on a bond and may earn up to 12% per year in equities. You immediately know that you may get 4% more every year in equities. This helps you compare and make a decision. However, if you were told you will earn 4% every 6 months on a bond and 40.5% in 3 years in equity, that would make comparison and decision making nearly impossible.

So when we say that a particular fund gave returns of 15% p.a. over the last 3 years, it means that the 15% of the second year was not just on your invested amount, but also on the returns you earned in the first year. Similarly, the ‘15%’ of the third year was on both your investment and your returns of the first two years. The returns get compounded because the value of your holdings always reflects the returns you have already earned. Just as your FD would, once the interest is credited at the end of a quarter.

So mutual fund returns do get compounded because the NAV of the fund is adjusted on a daily basis. The returns you have earned at any point, whether positive or negative, are already reflected in the fund value. So any return you earn there on, will be on the return you have already earned. Hence your mutual fund returns are compounded just as much as your bank FD returns.

Your explanation is correct. But as laymen we always look at the value reflected in the CAS received every month and rejoice if it is up or feel lowly when the fund value is less than the amount invested! It always happens so as these are related to the Share Market. We have to accustom to these things slowly when compared to the already EMERGED markets.