Rainbow Childrens Medicare Ltd. – Paediatric Hospitals

Rainbow Childrens Medicare Ltd (RCML) operates a chain of paediatric hospitals with prenatal centres. The company was founded in 1999 by Dr. Ramesh Kancharla in Hyderabad, with its focus on child and women healthcare. The Rainbow Group has seven hospitals in Hyderabad, three in Bengaluru, two each in Delhi and Chennai, and one each in Vijayawada and Visakhapatnam. The Group also has three outpatient clinics in Hyderabad, Vijayawada and Visakhapatnam with a total count of sixteen hospitals. RCML operates under the brand, “Rainbow Children’s Hospital” and “Birthright by Rainbow”. RCML’s operational subsidiaries, Rainbow Specialty Hospitals Private Limited (RSHPL) operates a cardiac hospital in Hyderabad and Rosewalk Healthcare Private Limited (RWHPL) runs a boutique maternity hospital in Delhi. The Group has a total capacity of around 1,655 beds, of which around 1,230 were operational as on FY23.

Products & Services:

The company’s Paediatric services segment operating under the brand “Rainbow Children’s Hospital” includes newborn and paediatric intensive care, paediatric multi-specialty services, paediatric quaternary care (including organ transplantation); whereas the women care services segment under “Birthright by Rainbow” offers perinatal care services which includes normal and complex obstetric care, multi-disciplinary fetal care, perinatal genetic and fertility care along with gynaecology services.

Subsidiaries: As on FY23, the company had 6 subsidiaries.

Key Rationale:

- Hub and Spoke Model – Rainbow Children’s Hospital is built on strong fundamentals of multidisciplinary approach in a child centric environment with a unique doctor engagement model, where doctors work exclusively on a fulltime, retainer basis to offer 24/7 consultant led service, which is particularly important for children’s emergency, neonatal, paediatric intensive care services and to support paediatric retrieval services. The company follows a hub-and-spoke operating model where the hub hospital provides comprehensive outpatient, inpatient care, with a focus on tertiary and quaternary services while the spokes provide 24/7 emergency care in paediatrics and obstetrics, large outpatient services and comprehensive obstetrics, paediatric and level 3 NICU (Neonatal Intensive Care Unit) services. This model is successfully operational at Hyderabad and is gaining traction in Bengaluru. The endeavour is to replicate this approach in Chennai and across the National Capital Region. Subsequently Rainbow intends to expand into tier-2 cities of Southern India.

- Latest Updates – The company has appointed Mr. Sanjeev Sukumaran as Chief Operating Officer (COO). He has over 25 years of experience in strategic management, business advisory, sales and marketing, business development, and client relationship management across a diverse range of sectors. During the quarter, the company signed an agreement to lease for a brownfield ~80 beds spoke hospital at Sarjapur, Bengaluru. The hospital is strategically located and will make an important part of the Rainbow network in the city. This hospital is likely to commence operations during the last quarter of the FY24. Also, an additional block with an outpatient department and an IVF facility at Rainbow LB Nagar, Hyderabad to enhance the patient facilities at the existing hospital and cater to the future growth at this spoke hospital.

- Q4FY23 – The company’s revenue increased by 49% YoY to Rs.317 crore in Q4FY23. The EBITDA increased by a whopping 104% YoY from Rs.48 crore in Q4FY22 to Rs.98 crore in Q4FY23 and the EBITDA margin has improved by 826 bps from 22.6% in Q4FY22 to 30.9% in Q4FY23. The Profit after tax for the company has reported a massive growth of 339% YoY from Rs.12 crore in Q4FY22 to Rs.54 crore in Q4FY23. The number of operating beds have improved from 1150 in Q4FY22 to 1232 in Q4FY23.

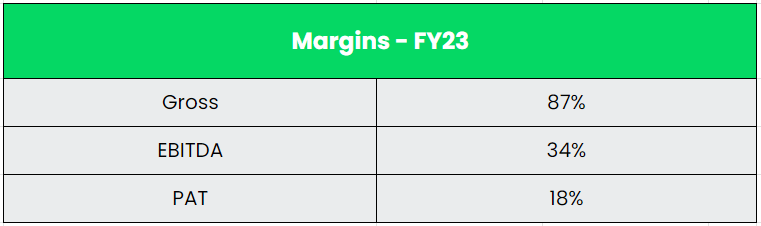

- Financial Performance – The revenue and PAT CAGR have grown at 24% and 42% between FY18-23. The operating cashflow of the company is consistently positive and growing historically. The company generated around Rs.700 crore of cashflow from operations in the last 5 years. The EBITDA to OCF conversion has been strong for the company and it is around 82% in FY23 from 73% in FY22. The company has zero debt in its balance sheet with only lease liabilities of Rs.570 crore as on FY23.

Industry:

Owing to the country’s overall economic development and growing population, the Healthcare industry has emerged as one of the largest contributors to the Indian economy, both in terms of revenue generation and employment opportunities. The Indian Health Care sector is expected to grow to Rs.8,620 billion by FY26 with a CAGR of 12%. The expansion of private and public healthcare facilities, as well as increased knowledge about childcare and early identification of diseases, are expected to drive growth in the maternity and paediatric care market in India. In FY2020, the combined market share of paediatric and maternity care in hospitals was approximately 33% of the total hospital market, amounting to Rs.1,390 billion. Private maternity care held a 45% share of the total maternity market, and it is projected to expand at a compound annual growth rate (CAGR) of 12% between FY2020-26, reaching a market size of Rs.330 billion. Similarly, the private paediatric care market constituted 60% of the overall paediatric market and is predicted to grow at a CAGR of 14% during FY2020-26, eventually achieving a market size of Rs.1,340 billion.

Growth Drivers:

- 100% FDI in the healthcare industry has been approved through the automatic route for investments in the development of hospitals, healthcare facilities and the manufacture of medical products.

- In the Union Budget 2023-24, the government allocated Rs.89,155 crore (US$ 10.76 billion) to the Ministry of Health and Family Welfare (MoHFW).

- A number of socioeconomic reasons have contributed to an increase in the average age of pregnancy in the country. The age group of 25-29 years accounted for 32% of births in FY2010-15andmoving forward, the age groups 25-29 years and 30-34 years are predicted to contribute a greater proportion of live births. This trend towards delayed pregnancy can cause increased complications, which may result in a higher demand for maternity healthcare in India.

Competitors: Apollo Hospital, Narayana Hrudayalaya, KIMS, etc.

Peer Analysis:

RCML is having a chain of paediatric hospitals whereas, its peers are having super speciality and multi-specialty hospitals. So, RCML have a niche space in the hospital business itself. In terms of fundamentals, RCML is competing well with its peers.

Outlook:

The company remains the only listed paediatric hospital chain. The company crossed an important milestone of a million outpatients across the group and successfully completed 20 liver transplants and five kidney transplants with excellent results. During the year, the Company has successfully inaugurated a new hospital with 100 beds in the Financial District of Hyderabad, as well as a 55-bed hospital in Sholinganallur (OMR), Chennai. The company has also won two bids to build Greenfield hospitals in Gurgaon, Haryana, with a 300-bed facility in sector 44 and a 100-bed Spoke Hospital in sector 56. The Gurgaon hospital will be a high capex, multi-specialty hospital, different from their routine children’s hospitals. The current ARPOB (average revenue per operating bed) for the hospital group is Rs.48,900, but the Gurgaon hospital will have a higher ARPOB. The company is adding roughly 400 beds in the next two to three years, which will result in a 50-50% mix between mature and new hospital beds. The break-even timing for new hospitals is one to one and a half years, depending on location and size. The company has guided for Rs.420 crores of EBITDA for the current financial year, with high teens growth in revenue.

Valuation:

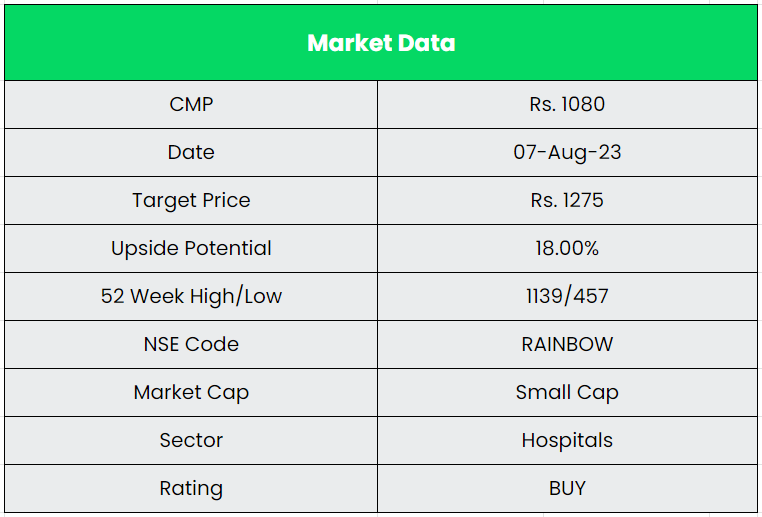

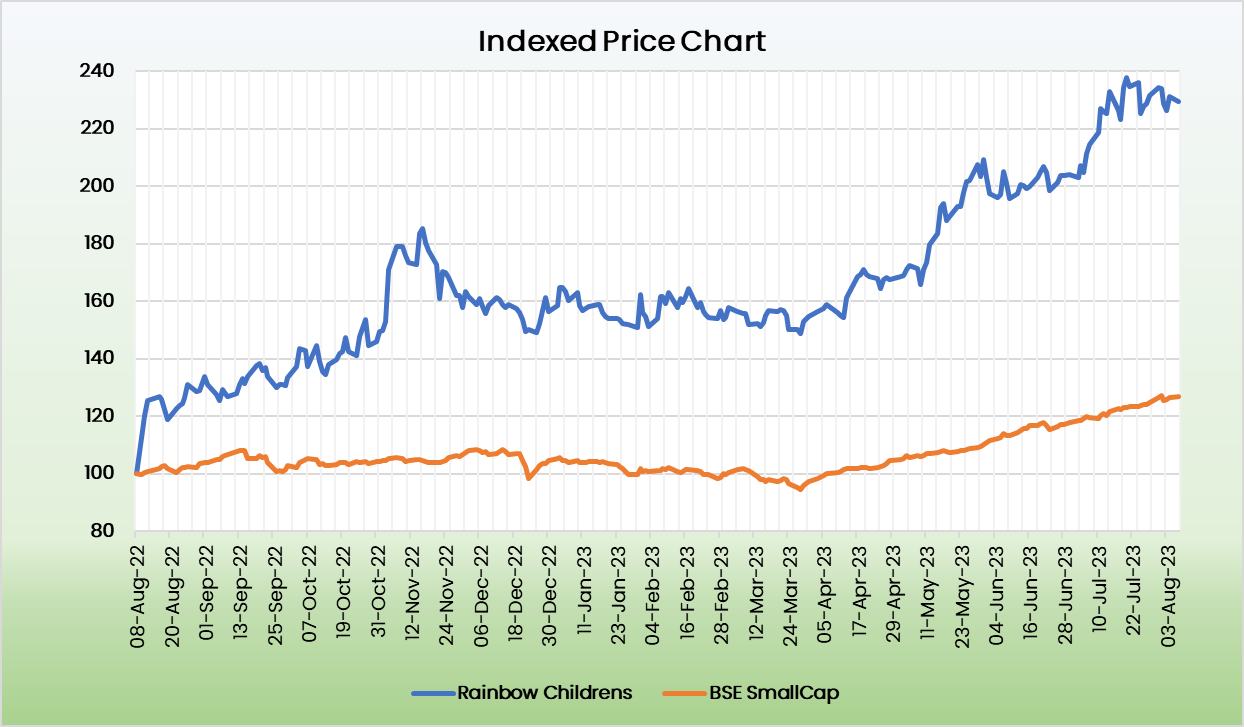

Rainbow’s asset-light, hub and spoke model of expansion has been the success story so far. The company’s debt free position and strong cash conversion will drive the expansion going forward. We recommend a BUY rating in the stock with the target price (TP) of Rs.1275, 23x FY25E EV/EBITDA.

Risks:

- Attrition Risk – The company’sperformance and the execution of its business strategies depend substantially on its ability to attract, recruit and retain doctors in specialties such as paediatrics, obstetrics and gynaecology. Inability to recruit or retain the professionals will impact the quality of the services.

- Regulatory Risk – The company is required to comply with a variety of regulations at the central, state and local levels. These regulations cover a wide range of areas, including patient care, privacy, safety, and record-keeping. Non-compliance with these regulations can lead to fines, legal action, and damage to the hospital’s reputation.

- Competitive Risk – The Rainbow Group has revenue dependence on paediatrics and obstetrics specialities and faces high competition from established hospitals in Chennai, Delhi and Bengaluru, where it is a recent entrant with limited brand recognition, however the company has substantial scale-up plans in these cities which is expected to improve the brand identity in these regions.