Persistent Systems Ltd – Re(AI)magining the World

Incorporated in 1990 and headquartered in Pune, Persistent Systems Limited is an AI-led, platform-driven digital engineering and enterprise modernization company that partners with global enterprises across the software development and technology transformation lifecycle. Its business is organised across three industry verticals – Software, Hi-Tech & Emerging Industries; Banking, Financial Services & Insurance (BFSI); and Healthcare & Life Sciences – and is anchored on three AI pillars: Engineering Hyper-Productivity, Business Hyper-Productivity, and Enterprise Data Readiness, underpinned by proprietary platforms SASVA, iAURA and GenAI Hub. Persistent serves 20 of the Fortune 50, including 7 of the top 10 technology companies and 4 of the top 5 banks in both the US and India, delivered through a 27,502-strong workforce spread across North America, India, Europe and the rest of the world. As of March 31, 2026, the company held a portfolio of 121 patents spanning AI infrastructure, data intelligence and autonomous agents.

Products and Services

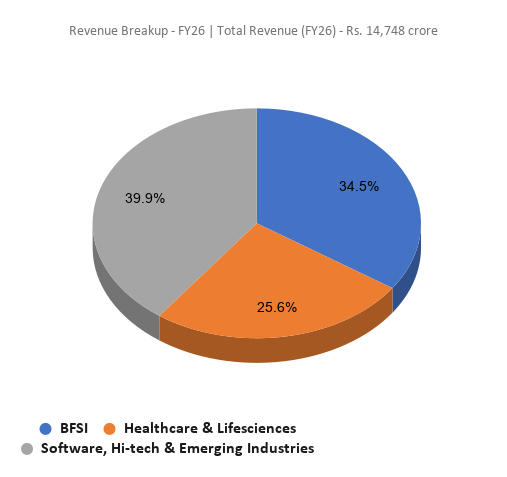

- Banking, Financial Services & Insurance (BFSI) — The largest and fastest-growing vertical, contributing 34.5% of Q4FY26 revenue (FY26: 34.6%), up from 31.6% in FY25. Persistent serves 4 of the top 5 banks in both the US and India and top 3 of the top 5 fintechs. Service offerings within BFSI span core banking and insurance platform modernization (including COBOL-to-cloud migration), payments infrastructure (FedNow, real-time settlement), enterprise data modernization for regulatory compliance (BASEL, AML, KYC, DORA), and agentic AI-led digital underwriting and cost transformation.

- Healthcare & Life Sciences (HL&S) – Contributing 26.3% of Q4FY26 revenue (FY26: 25.6%), Persistent works with 2 of the top 5 health providers and payors, 3 of the top 5 pharmaceutical companies, and 4 of the top 5 clinical research organizations. Offerings include care management platform engineering, clinical and research data unification, AI-driven drug discovery (protein structure prediction, molecular simulation via NVIDIA BioNeMo), and cloud-native CRO platform transformation.

- Software, Hi-Tech & Emerging Industries – The largest vertical by revenue at 39.2% of Q4FY26 (FY26: 39.8%), serving 7 of the top 10 global technology companies. This vertical anchors Persistent’s AI-led SDLC proposition – engineering hyper-productivity via SASVA – alongside product engineering, platform carve-outs, SAP services, and software-to-cloud transformation for technology and industrial companies.

Subsidiaries: As of FY26, the company has 21 subsidiaries and one controlled ESOP trust.

Investment Rationale

- AI-led, platform driven model – Persistent’s defining feature is its ability to position the GenAI/SDLC disruption as a net tailwind rather than a threat. The “Sixth Orbit” strategy is anchored on three AI pillars — Engineering, Business Hyper-Productivity and Enterprise Data Readiness — operationalised through proprietary platforms SASVA, iAURA and GenAI Hub, a 500+ agent portfolio, and 121 patents. Critically, SASVA runs as a model-agnostic native layer integrating Anthropic, OpenAI, Copilot and Gemini, letting Persistent monetise client tool choices rather than be disintermediated. Management has guided a $2 billion revenue for FY27, with the June 2026 AI Investor Day serving as a near-term catalyst.

- Steady margin expansion underpinned by operating leverage and capital efficiency – Beyond growth, the quality of earnings is improving. FY26 EBIT margin expanded 90bps YoY to 15.6% (EBIT +31.5%, PAT +33.2%), with management reaffirming a 16-17% aspiration while explicitly prioritising growth and capability investment over near-term margin capture. The company demonstrates disciplined execution: ROCE of 44.4% and ROE of 26.3% rank among the best in the sector, while OCF/PAT strengthened to 94.7% in FY26 from 82.6% in FY25, indicating strong cash conversion.

- Growth spread across many clients and a strong deal pipeline – Persistent’s growth is broad-based rather than dependent on a handful of accounts. Its banking and financial services (BFSI) vertical led the way in FY26 with 28.4% growth, supported by steady momentum in healthcare and technology. The client base is also deepening — the number of clients generating over $5 million in annual business rose from 55 to 62, and those above $1 million grew from 191 to 201 over the year. The deal pipeline backs this up: total contract value (TCV, the worth of all deals signed) reached about $2.4 billion for FY26, and headlined by a marquee new SAP services deal worth over $50 million. With its largest clients steadily expanding while overall concentration stays controlled, the business looks well-diversified and resilient.

- Q4FY26 – During the quarter, Persistent reported consolidated revenue of ₹4,055.9 crore, up 25.1% YoY, marking its 24th consecutive quarter of growth. The higher rupee-terms growth was partly helped by a weaker rupee, with the average exchange rate at ₹93.0 per dollar versus ₹86.4 a year earlier. Operating profit (EBIT) rose 30.5% YoY to ₹659.2 crore, with the EBIT margin improving 70 basis points YoY to 16.3%. Net profit grew 33.7% YoY to ₹529.3 crore translating to a net margin of 13.1%.

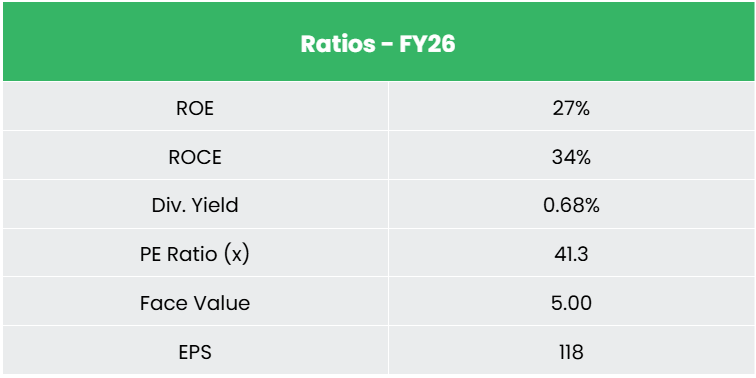

- FY26 – For the full year, consolidated revenue stood at ₹14,748.4 crore, up 23.5% YoY in rupee terms (17.4% in dollar terms). Operating profit (EBIT) grew 31.5% YoY to ₹2,303.5 crore, with the EBIT margin expanding 90 basis points to 15.6% (including a small ~0.6% one-time impact from the new labour codes). Net profit rose 33.2% YoY to ₹1,865.1 crore, with the net margin at 12.6% and EPS at ₹119.7. The Board recommended a final dividend of ₹18 per share, taking the total FY26 dividend to ₹40 per share, up from ₹35 in FY25.

- Financial Performance – The 3-year revenue and net profit CAGR stands at 21% and 28% respectively between FY24-26. The company has a debt-to-equity ratio of 0.06. The 3-year average ROE and ROCE are around 25% and 31%.

Industry Overview

The Indian IT-BPM sector has emerged as a critical pillar of the economy, with revenue estimated at ₹25,68,159 crores (US$297 billion) in FY25, growing at a CAGR of ~9.2% from ₹10,42,915 crores (US$167 billion) in FY18. Export revenue reached ₹20,14,751 crores (US$233 billion) in FY25, registering 16.5% growth from US$200 billion in FY24, with IT services accounting for 66% of total exports, followed by Business Process Management at 26% and Engineering R&D and software products at 8%. The sector directly employs 5.8 million professionals, with India ranking third globally among startup ecosystems with over 68,000 tech startups and improving seven places to 38th in the 2024 Global Innovation Index. The computer software and hardware sector attracted cumulative FDI inflows of ₹8,31,772 crores (US$110.16 billion) between April 2000–June 2025, ranking second in sectoral FDI and contributing 15.54% of total cumulative FDI equity inflows. India’s IT sector is on track to double revenue to ₹43,23,500 crores (US$500 billion) by 2030, driven by AI adoption, cloud transformation, and expansion of Global Capability Centers expected to generate 22–25% of net new white-collar tech jobs.

Growth Drivers

- AI and emerging technology proliferation

India’s AI market is projected to reach US$131.31 billion by 2032 at a CAGR of 42.2%, with AI expected to contribute US$957 billion to GDP by 2035, supported by the IndiaAI Mission’s ₹10,300 crores (US$1.19 billion) five-year allocation underpinned by deployment of 38,000 GPUs. - Cloud adoption and data center expansion

India’s public cloud services market is projected to reach US$13 billion by 2026 and US$17.8 billion by 2027, with data center capacity expected to triple from ~870 MW in 2023 to 2,500 MW by 2027, driving the broader market to US$15 billion by 2030 on the back of 850 million+ internet users and 10 billion+ monthly UPI transactions. - Expanding Global Capability Centers and geographic diversification

GCCs are expected to generate 1.2 million of the 4.7 million new tech jobs projected by 2027, with the GCC workforce projected to reach 3.46 million by 2030, while non-metro cities drove over 50% IT hiring growth in H1 2025 at ~30% cost savings over metro alternatives.

Peer Analysis

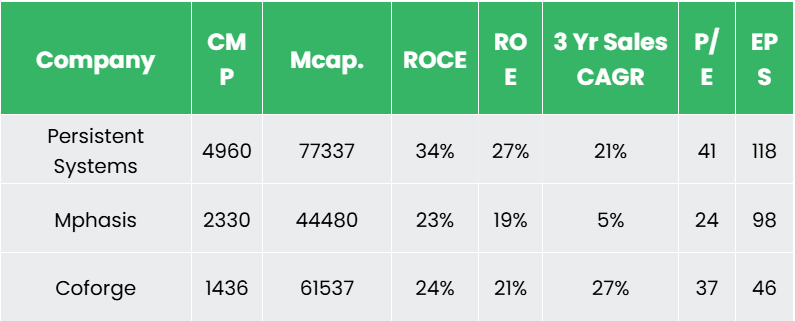

Competitors: Mphasis Ltd, Coforge Ltd etc.

The company boasts an industry leading return profile, and demonstrates disciplined capital allocation and superior margins, while maintaining an unencumbered balance sheet.

Outlook

Persistent does not provide formal financial guidance, but management’s commentary points to continued healthy growth in FY27. The company reaffirmed its target of reaching a $2 billion annualised revenue run-rate – around ₹17,800 crore a year by the end of FY27, with healthcare & life sciences and BFSI to lead and run neck-and-neck in FY27, followed by the technology vertical – a modest shift from FY26, when BFSI was the clear standout. On profitability, it has reiterated an aspiration to operate in the 16-17% EBIT margin range, while making clear that revenue growth and continued investment in AI capabilities take priority over near-term margin gains. AI adoption is expected to accelerate over the coming quarters, led by technology clients who adopt fastest, while regulated sectors like banking and healthcare move more gradually from pilots to enterprise-wide rollouts, albeit, acknowledging that AI could compress some traditional software-development work, particularly in technology which is expected to be more than offset by winning incremental market share.

Valuation

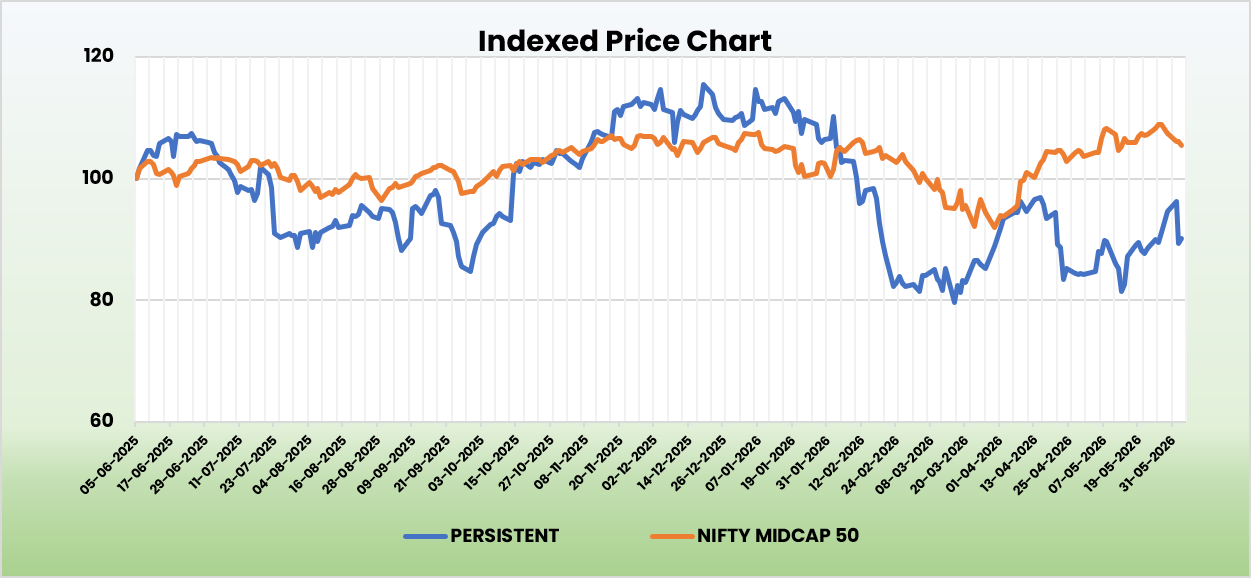

Persistent’s strong positioning in the AI adoption wave and well diversified business verticals position it to capitalize the AI driven industry tailwinds. We recommend a BUY rating on the stock with a target price (TP) of Rs. 6,037, 37x FY28E EPS, an upside potential of ~20%. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.