Fortis Healthcare Ltd. – Transforming lives, Growing Together

Incorporated in 1996 and headquartered in Gurugram, Fortis Healthcare Ltd. (“Fortis” or “the Company”) is amongst India’s leading healthcare delivery companies and one of the largest healthcare services providers in the country. The company offers an integrated spectrum of healthcare facilities spanning hospitals, diagnostics and day-care specialty hospitals. Fortis operates a network of 36 healthcare facilities, including joint ventures and O&M facilities, spread across 12 states in India. This network comprises ~6,100 operational beds, including O&M beds, complemented by a diagnostics arm running over 400 labs across the country.

Products and Services

The company’s services can be categorised into two segments:

- Healthcare includes inpatient and outpatient services, sale of medical and non-medical items and management fees from hospital.

- Diagnostics includes pathology and radiology services.

Subsidiaries: As of FY25, the company has 29 subsidiaries and 2 associates and joint ventures each.

Investment Rationale

- Capacity Expansion Underway – Fortis has pursued an active network expansion strategy in FY26, combining brownfield initiatives with select acquisitions to strengthen its footprint in key geographies. The company added ~800 beds during the year, of which ~500 beds came through inorganic additions – the acquisition of People Tree Hospital in Bengaluru, Shrimann Hospital in Jalandhar, Punjab, and a long-term lease arrangement for a 200-bed multi-specialty hospital in Greater Noida that strengthens its presence in the NCR region. The company also launched Adayu, a 36-bed specialised mental healthcare facility in Gurugram, offering multidisciplinary treatment. This expansion was supported by a capex outlay of ₹700 crore during FY26. Looking ahead, Fortis has outlined a further brownfield expansion of ~1,800 beds over FY27-FY30. Of this, FY27 alone is expected to see the addition of 400+ beds, led by the operationalisation of a new tower at FMRI, along with incremental capacity at Noida, Manesar, Amritsar and FHKI Kolkata.

- Volume led momentum – Fortis delivered healthy revenue growth across both its hospital and diagnostics segments in FY26, driven primarily by improved bed utilisation and case mix. Occupied beds grew 15.2% to 3,270 in FY26 from 2,838 in FY25, though overall occupancy moderated slightly to 68% from 69%, a trend also visible in Q4FY26 (68% vs 69% in Q4FY25) despite a 17% YoY increase in occupied beds for the quarter. Hospital business ARPOB improved 3.4% YoY to ₹2.51 crore p.a. in FY26, with Q4FY26 ARPOB at ₹2.56 crore against ₹2.51 crore in Q4FY25, up 2.0%. This translated into hospital business revenue of ₹2,023 crore in Q4FY26 (up 19% YoY) and EBITDA of ₹446 crore (up 20% YoY). Growth was led by key focus specialties – Radiation Therapy and Robotic Surgeries grew 19% and 66% YoY respectively, while the Top 6 specialties (Cardiac, Orthopedics, Neurology, Gastroenterology, Oncology and Renal Sciences) grew 18.9% and contributed ~62% of overall revenues. International Patient revenues rose 18.5% to ₹639 crore, forming 7.8% of hospital business revenue. The diagnostics business (Agilus) also scaled up, with revenue and EBITDA growing 11% and 36% YoY respectively, on the back of ~40.8 Mn tests conducted in FY26 versus ~39.2 Mn in FY25.

- Q4FY26 – During the quarter, the company generated revenue of ₹2,365 crore, achieving an increase of 18% as compared to the ₹2,007 crore of Q4FY24. EBITDA improved by 22% YoY, from ₹435 crore to ₹531 crore. Net profit stood at ₹271 crore, a growth of 44% from ₹188 crore of Q4FY25.

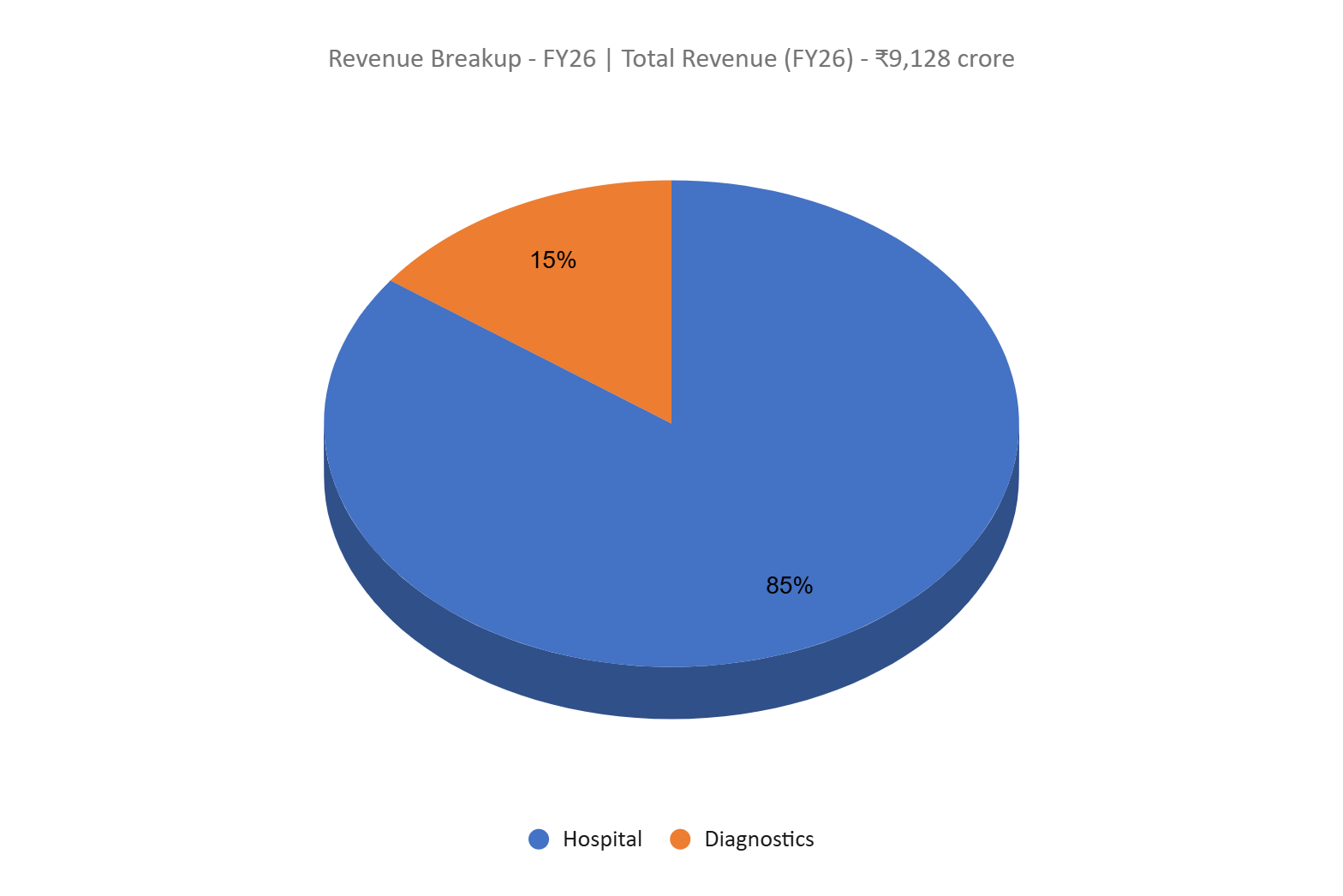

- FY26 – The company generated revenue of ₹9,128 crore, an increase of 17% compared to FY25 revenue. The growth was primarily driven by ~19% growth in hospital business revenue which contributes 85% to the company’s revenue. EBITDA is at ₹2,085 crore, up by 31% YoY. The company posted a net profit of ₹1,064 crore, a growth of 32% YoY. EBITDA margin has improved from 20% to 23%. Hospital business has improved its EBITDA margin from 21% to 22% and diagnostics arm EBITDA margin from 18% to 24%.

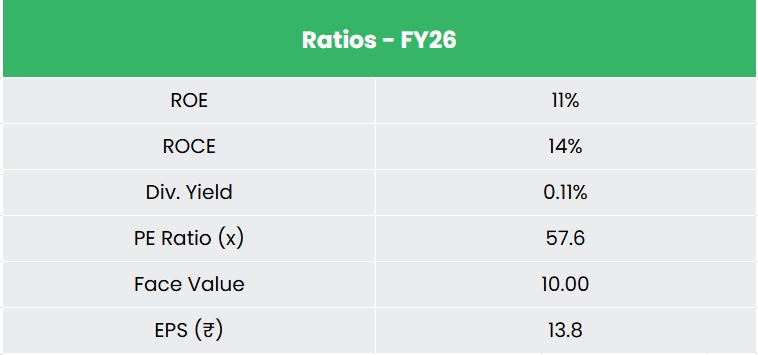

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 13% and 27% between FY24-FY26. The 3-year average ROE and ROCE for the company is around 10% and 12% for the past 3 years. The company has a healthy capital structure with a debt-to-equity ratio of 0.35.

Industry

The Indian hospital market, valued at US$ 98.98 billion in 2023, is projected to grow at a CAGR of 8.0% between 2024 and 2032 to reach an estimated US$ 193.59 billion by 2032, reflecting the sector’s steady expansion on the back of strengthening healthcare coverage, improving service standards, and rising expenditure by both public and private players. Growth is increasingly being driven by Tier II and Tier III cities, where healthcare demand is expected to grow at 16-18% CAGR over the coming years, outpacing the 12-14% CAGR projected for metro cities and signalling sustained momentum beyond 2025. India has also emerged as a preferred destination for high-end diagnostic services, supported by significant capital investment in advanced diagnostic infrastructure that is extending access to a wider population base. Despite this progress, structural gaps remain, with the country estimated to require an additional 3.6 Mn hospital beds, 3 Mn doctors, and 6 Mn nurses by 2034 to align with global healthcare benchmarks.

Growth Drivers

- Increased Government Healthcare Spending – The Union Budget 2026-27 allocated ₹1,06,530.42 crore (US$ 12.05 billion) to the Ministry of Health and Family Welfare, marking a ~10% increase over the Revised Estimates of FY 2025-26 (₹96,853 crore).

- Expansion of Public Health Insurance Coverage – The government has allocated ₹9,500 crore (US$ 1.08 billion) towards Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) for FY27, reinforcing its flagship health insurance scheme aimed at providing financial protection and improving access to quality healthcare for a large section of the population.

- Favourable Demographic and Behavioural Shifts – Rising income levels, an ageing population, growing health awareness, and a changing attitude towards preventive healthcare are expected to drive higher demand for healthcare services in the years ahead, supporting sustained growth across the sector.

Peer Analysis

Competitors: Aster DM Healthcare Ltd, Global Health Ltd, etc.

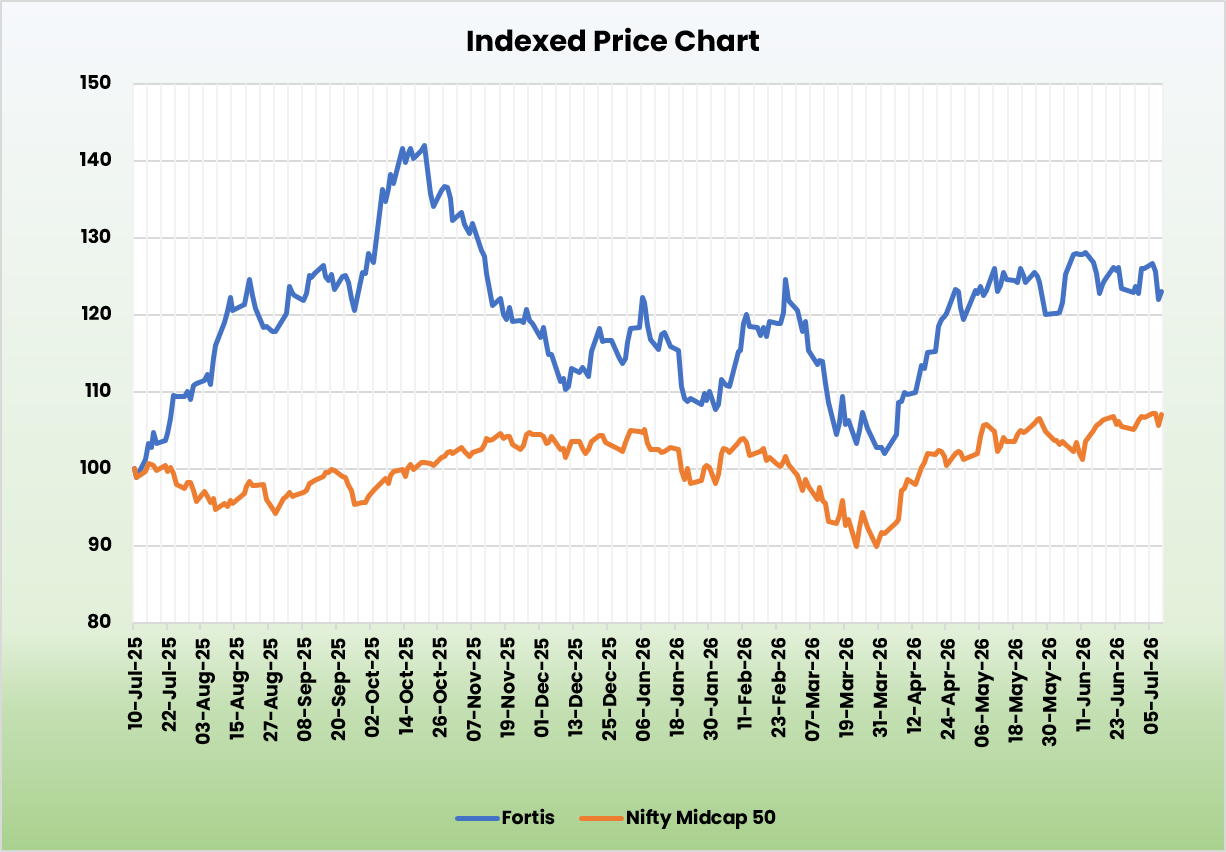

We believe the company is fairly valued relative to its peers, supported by strong fundamentals, robust revenue growth, consistent returns on invested capital, and higher operating margins that reflect disciplined cost management and operational efficiency.

Outlook

Fortis is well-placed to sustain its growth trajectory over the coming years, with planned brownfield capacity addition of ~1,800 beds over the next four years, of which more than 400 beds are expected to come online in FY27 itself, led by the FMRI tower and balanced additions at Noida, Manesar, Amritsar and FHKI Kolkata. On the back of this expanding bed base and improving occupancy across mature facilities, management expects the hospital business to deliver revenue growth in excess of 15% for the current financial year, accompanied by a further ~150 bps improvement in EBITDA margin. The diagnostics business is also expected to see continued margin expansion, with EBITDA margins guided to improve from the 22-23% range achieved in FY26 to around 23-24% in the coming year, reflecting steady operating leverage as testing volumes scale up.

Valuations

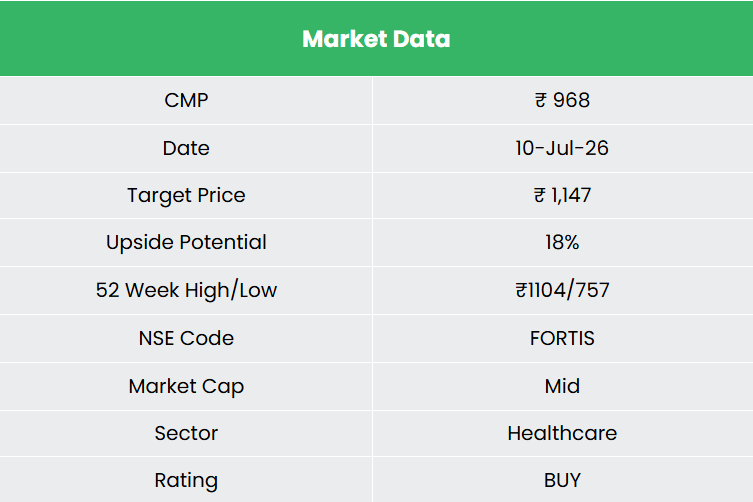

We believe Fortis will continue its earnings trajectory, underpinned by capacity-led growth and margin expansion. We recommend a BUY rating in the stock with the target price (TP) of ₹1,147, 55x FY28E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.