Data Patterns (India) Ltd – Defence and Aerospace Electronic Solutions

Data Patterns (India) Limited is one of the fastest-growing companies in the Defence and Aerospace Electronics sector in India. It is one among the few vertically integrated defence and aerospace electronics solutions providers catering to the indigenously developed defence products industry with end-to-end capabilities and a large addressable market. Incorporated as “Indus Teqsite Private Limited” in 1998, at Bangalore, Karnataka as a Private Limited Company, the company’s name was changed to “Data Patterns (India) [Private] Limited” in August 2021. It was subsequently converted into a public limited company in December 2021. The company is focused on in-house development and manufacturing facilities led by innovation and design and development efforts. It has supplied products catering to various platforms, viz., space, air, land and sea, including products for LCA-Tejas, LightUtility Helicopter, BrahMos missile.

Products & Services

Data Patterns offer products under the business domains of Automatic Test Equipment (ATE) and Rugged Military Electronics (RME). Major products include Avionic and Space Systems, Radar and Electronic Warfare products, COTS Boards, RF & Microwave, Cockpit and Rugged displays, Communication Products, Naval and Navigation Systems etc.

Subsidiaries: As of FY23, the company does not have any subsidiaries, joint ventures or associate companies.

Key Rationale

- Orders from reputed defence organisations – Over more than 3 decades, Data Patterns has established itself to be one of the few companies with product capabilities covering the entire spectrum of Defence and Aerospace platforms, encompassing space, air, land and sea. It has positioned itself to be one of the strong allies with many reputed clients in Defence sector. The major customers include the Ministry of Defence (MoD), Defence Research and Development Organisation (DRDO), BrahMos Aerospace Private Limited, Bharat Electronics Limited (BEL), Bharat Heavy Electronics Limited (BHEL), Hindustan Aeronautics Limited (HAL), Electronic Corporation of India Ltd (ECIL) and units operated by the Indian Space Research Organisation (ISRO).

- Expansion plans – The company is well positioned to benefit from the “Make In India” initiative by Government of India. It has started to participate in large value tenders like Make-1 and Make-2 categories with Ministry of Defence. The company has raised Rs.500 crores through QIP to develop products in radars, EW, communications and satellites. In addition to supplying subsystems, the company is stepping up its business line to provide whole systems to MoD. The order book during Q2FY24 reached Rs.1000 crores, with an order inflow of Rs.145 crores, which includes export order of about Rs.39 crores majorly from Europe, UK and South Korea.

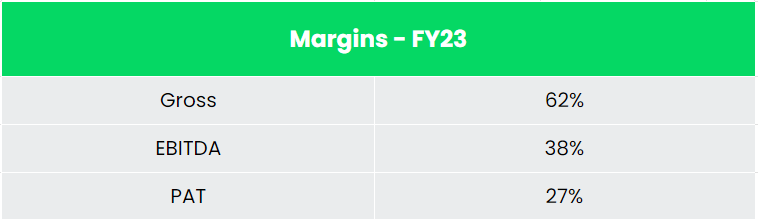

- Q2FY24 – Data Patterns reported a revenue of Rs.108 crores marking an increase of 23% compared to the Rs. 88 crores revenue of Q2FY23. EBITDA stood at Rs. 41 crores compared to the Rs.30 crores of FY23, a surge by 37% YOY. The profit after tax stood at Rs.34 crores which is a robust growth of 62% as compared to the Rs.21 crores of same period in the previous year. The EBITDA and PAT margin were 38% and 31% respectively.

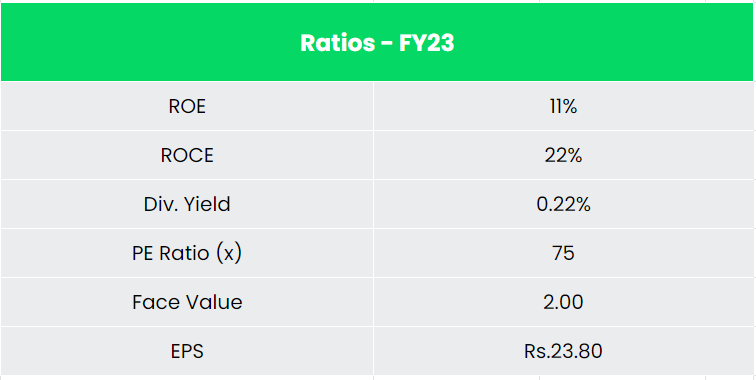

- Financial performance – The company has generated a revenue and PAT CAGR of 52% and 151% over the period of 5 years (FY18-23). Average 5-year ROE & ROCE is around 18% and 25% for FY18-23 period. The company has strong balance sheet and financial risk profile with zero debt outstanding, indicating its prudent financial management.

Industry

India is one of the strongest military forces in the world and hold a strategic importance for the Indian Government. To modernise its armed forces and reduce reliance over external dependence for defence procurement, several initiatives have been taken by the government to encourage ‘Make in India’ activities via policy support initiatives. Ministry of Defence has set a target of achieving a turnover of INR 1.75 lakh crore in aerospace and defence Manufacturing by 2025, which includes exports of INR 35,000 crore. The government has also announced 2 dedicated Defence Industrial Corridors in the States of Tamil Nadu and Uttar Pradesh to act as clusters of defence manufacturing that leverage existing infrastructure, and human capital.

Growth Drivers

In the Union Budget 2023-24, the Capital Allocations pertaining to modernisation and infrastructure development of the Defence Services has been increased to INR 1,62,600 crores representing a rise of 6.7% over FY22-23. The industry got INR 5.94 Lakh crores in Budget 2023-24, a jump of 13% over previous year. Under the Atmanirbhar Bharat or Self-Reliant India Initiative, four positive indigenization lists of 411 products have been promulgated by Department of Military Affairs and Ministry of Defence to be manufactured domestically for the defence sector, instead of being sourced via imports.

Competitors: Bharat Electronics Limited (BEL), Bharat Dynamics Ltd (BDL) etc.

Peer Analysis

Among the above competitors, Data Patters is generating a higher revenue from the amount of capital invested. The company has strong balance sheet and financial risk resistance with zero debt in the capital structure.

Outlook

The Indian defence manufacturing industry is a significant sector for the economy. The industry is likely to accelerate with rising concerns of national security. We believe Data Patterns is emerging to be a strong player in the industry with its vertically integrated production strategy and marquee client base. In the recent years, the company has raised capital through IPO and QIPs, indicating its capital abundance to invest in niche projects and sustenance of existing business lines. The company is developing new products to meet the requirements of defence forces making itself ready to zero in new orders as any requirement arises. The company is aiming to position itself as an end user system manufacturer while also developing the sub systems vertical.

Valuation

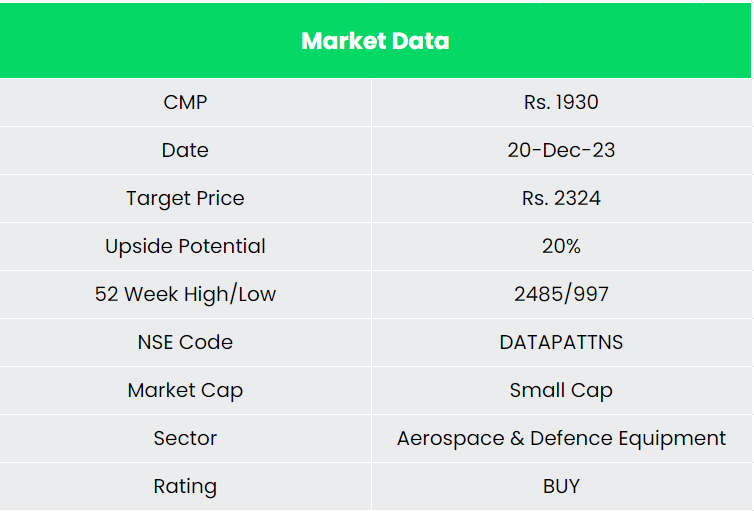

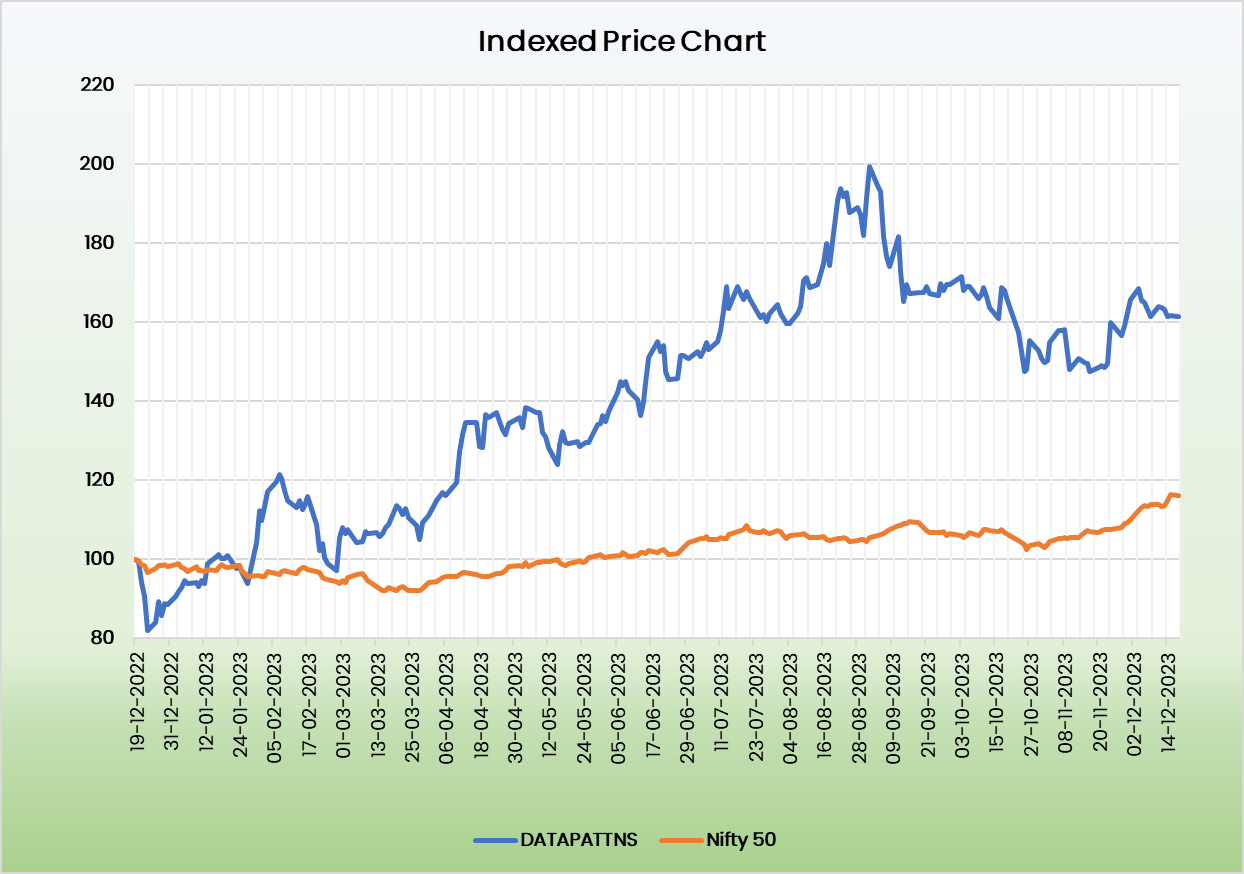

We believe Data Patterns (India) Limited is in a position for robust growth in the coming years. It’s growing market share in the existing business and upcoming projects the company has in pipeline places it in a position for a upside growth potential. We recommend a BUY rating in the stock with the target price (TP) of Rs. 2324, 21x FY25E EPS.

Risks

- Project getting delayed – There is likelihood of projects being deferred due to procedural delays, which might lead to order deferment, an inherent risk of defence industry.

- Regulatory risk – The industry is highly susceptible to regulatory changes, and this might result in ban/redundance of certain products, affecting revenue.