Imagine there are three bowls of water in front of you – one cold, one hot, and another at room temperature. Assume you put one hand in the bowl with the cold water, and the other in the hot water for about a minute. Now put both hands in the bowl containing room temperature water. The water will feel cold to the hand that originally was in the hot water, and warm to the hand that was in the cold water.

While the actual water temperature remains the same in an absolute sense, you can trick yourself to experience it as either hot or cold based on how it is relative to recent experience.

Now, what does this have to do with equity investing?

Equity investing is for the long term. Based on past history, the return expectation on which you have sold equities will usually be around 12-15%. This is a message that has been beaten to death.

Now, the only issue is you don’t experience long term as a single point of experience. You experience long term as the cumulation of several short terms.

A 10-year return is psychologically experienced as:

- 520 weekly returns or 120 monthly returns or 20 half-yearly returns or 10 yearly returns.

Equities is an extremely volatile asset class in the short term. This means the short term in which you live, measure, and experience the asset class, most of the times will have returns far lower than your expectations.

Unfortunately, you have already dipped your one hand into the “Equities will give 12-15% returns” expectations bucket. Add to it the other hand dipped in “At least FD returns” expectations bucket.

As you measure the equity returns over the short run and dip your hands into the actual short term returns, you suddenly have a reality check vis-a-vis your expectations.

- Less than FD returns – Disappointed (I would have been better off in an FD)

- Negative Returns up to -10% – Anxious (The news is bad. My gut feel says it should fall further)

- Fall extends from 10% to 20% – Regret (My intuition was right. I should have sold it much earlier)

- Further fall – Panic (Let me get out and re-enter once the coast is clear)

This is exactly where the problem lies. While our expectations are set for the long term, the short-term experience is conveniently ignored.

Equities being a variable experience product in the short run, investors will also need to have a rough expectation of what to expect in the short run based on history.

Here is a simple way to do this.

Start setting 6-month expectations. I have not used the 1 year period as it might be too long in the current instant portfolio alert world. While even shorter time frames can be explored, six months is a decent starting point, as it is neither too short not too long.

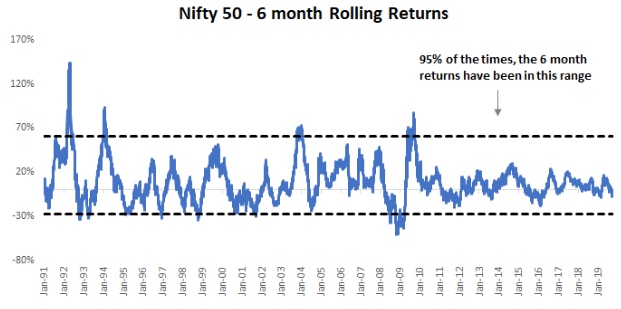

Nifty 6 month Rolling Returns

Now you need to factor in two things:

Normal Volatility:

I would define normal volatility as the 6-month return range which covers 95% of past occurrences leaving out the extremes.

Historically, 95% of the times over the last 29 years (from 1991 till date), the 6-month returns have ranged between -27% to 61%.

Obviously, no one knows where exactly it would land in the next six months. But the idea is that this range would be considered as the normal behaviour from the index.

If your portfolio falls in this range over the next 6 months, this would be considered as the normal expected asset class behaviour.

Major Crash:

The worst-case scenarios – i.e maximum drawdowns that have happened in the past are:

- In Subprime crisis (2008), Nifty 50 had declined -60% (requires +150% upside to recover the losses)

- In Dotcom bust (2000-2001), Nifty 50 had declined -50% (requires +100% upside to recover the losses)

Mentally, we must be prepared to see our equity portfolio decline by 50-60% at least once every ten years. Now let us check as to how this new framework helps us set better expectations.

You have ₹50 lakhs and are planning to invest in equities. Based on the long-term past returns, you are expecting around 12-15% returns over the long run. In other words, you are looking to double your money every 5-6 years.

Wow! That looks great. You are all set to invest.

Here is where you take a pause.

Just the click of a button to invest, logically can’t be the only effort for such higher returns.

You need to ask the key question – What am I expected to pay for this?

As you guessed it right, you need to pay a cost. While the monetary cost in terms of expense is visible, the more important cost is invisible via the emotional fees to be paid. This takes the form of frequent uncertainty and sleepless nights you will face in terms of “Will my portfolio fall further?”.

That is where our framework comes in. If you want to invest ₹50 lakhs in equities, you should be ok to see your portfolio value anywhere between 36 lakhs to 80 lakhs over the next 6 months. This would be considered normal.

In the case of a severe crash like 2008, you must be ok to tolerate a fall of up to 60%. That is, the portfolio value can fall up to ₹20 lakhs.

If you are uncomfortable with this range, then you will need to add more debt allocation to reduce the near term decline range. The tradeoff is that you might need to compromise on the expected higher long-term equity investing returns from equities.

Understanding and consciously deciding on an asset allocation based on the tradeoff between long-term equity investing returns and short-term volatility is where the trick to successful long-term equity investing lies.

Summing it up

Thus, the key to having a good experience while investing in equities remains in setting the right expectations – both long term and most importantly the short term. The above framework can be a good starting point.