We have always remained strong proponents of Systematic Investment Plans (SIPs) in Equities.

Equity SIPs align comfortably with our salary cycle and help us in automating your monthly savings. Most importantly, it eliminates the need to constantly monitor markets and take monthly decisions.

So behaviorally, SIPs make perfect sense but…

Have you ever wondered why an Equity SIP, which simply buys equities every month, provides decent returns in the long run?

Since equity markets fluctuate a lot, depending on when you buy, you may end up buying at a

- Bad Price – meaning low long term returns

- Good Price – meaning reasonable long term returns (in line with underlying earnings growth of companies)

- Great Price – meaning phenomenal long term returns

The only catch here is that whether the buying prices are bad, good or great is only known in hindsight.

Enter SIP!

The SIP starts with the humble confession

‘Hey, I am not intelligent enough to predict if the buying price is bad, good or great. But I have a smart way around this..’

What would that be?

Over long periods of time, the markets usually go through all three different pricing phases – Bad, Good, Great prices.

But thankfully, they are not equally distributed (or otherwise SIPs would have miserably failed)

- Bad Price – happens a small % of times (~10-20% of the times*)

- Good Price – happens the majority of times (~60-80% of the times*)

- Great Price – happens a small % of times (~10-20% of the times*)

*Please note that these are rough approximate nos based on using history as a rough guide*

Cool!

Now here comes the interesting part of how an Equity SIP really delivers despite its simple premise – ‘I will buy every month come what may!’.

In a simple SIP, when you are buying equities each and every month for the same amount over a long period of time…

It is inevitable that you will buy equities at BAD prices in some of the months during your SIP. This happens because you know what is a BAD price only in hindsight.

But here is where it gets super interesting…

It is also inevitable that you will buy equities at GREAT prices in some of the months during your SIP.

What usually happens is that the returns from buying equities at GREAT prices compensate (usually overcompensate) for the lower returns obtained from phases where you bought at BAD prices!

Overall, if you haven’t realized yet – that’s exactly how you end up averaging your buying around the GOOD price and getting decent returns over the long run!

Such a simple and elegant concept right!

So the simple takeaway – If Equity SIPs are given a long enough time frame, they work out well for you.

Here is how this plays out in real life

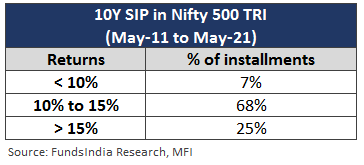

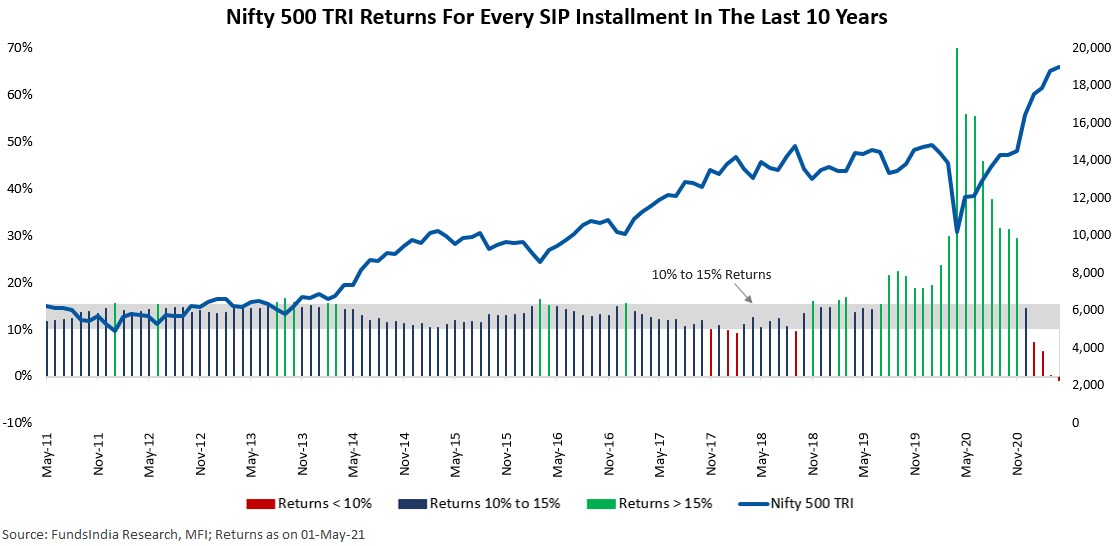

Let us take the example of a 10Y SIP in Nifty 500 TRI (the index which represents the largest 500 companies in Indian Stock Markets)

For the last 10 years, you would have invested every month for 120 months. Let us check how the returns panned out for each and every one of these 120 investments.

Any guesses what was the overall SIP return?

A Cool 13.8%!

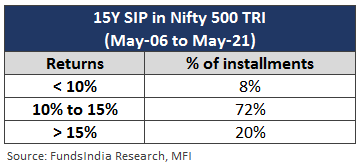

Let us check what happened in the last 15 years…

And, the overall SIP return for the period…

A Cool 12.4%!

As we had explained earlier, what has happened is that, the 10-20% of the times when you invested at GREAT prices you got 15%+ returns. This compensated for the 5-10% of the times when you invested at BAD prices and made sub 10%+ returns.

Overall we ended up with returns close to what we would have expected had we bought at GOOD prices.

The past history exactly shows that – if you have a 10-15 year time frame as seen below you have always ended up with decent returns. In those years where there was a sharp fall leading to lower returns, extending the time frame by 1-2 years brought back the returns to previous levels. This happens as markets have always recovered from temporary falls.

*SIP periods that ended in May-20 had a lower return due to the Covid led sharp market decline. Extending by 1 year led to returns getting back to pre covid levels.

Stopping SIPs when markets decline defeats the whole concept

Some of us tend to get upset during a market fall and stop our SIPs. Now that you know how an SIP works, this becomes a double whammy. Your SIP would have certain periods where it bought equities at BAD prices (which you obviously didn’t know at that point in time). So you will need some periods where you buy at GREAT prices to compensate for this.

Unfortunately, a market fall is usually when GREAT Prices happen.

If you stop your SIP during a market fall, you don’t get to buy at GREAT prices. This means you don’t get to compensate for the few periods where you bought at BAD prices.

Overall your SIP buying ends up looking like 60-80% good price + 10-20% bad price + 0% great price.

As a result, you end up with a lower return experience despite having a long time frame – due to a seemingly innocuous behavior lapse.

So it is important to understand that continuing your SIP in a market fall while it may seem very counterintuitive and painfully boring advice – is essentially the key reason why an SIP works over the long run.

Parting thoughts

Overall the idea of SIP is to provide a good return experience over the long term by deliberately doing something slightly inferior (read as buying at bad prices for a small % of the times) to avoid the likelihood of doing something very inferior (trying to manually time the entry 100% of the times). This small % of inferior buys is compensated over and above by the small % of great buys a SIP carries out during market falls.

Thus the whole success of SIP depends on whether you are able to continue your SIPs in a disciplined manner over the long term without panicking and stopping them during a market fall.