Ashok Kanawala, Head – Products and Business Development, HDFC Asset Management, explains why planning for retirement has been relegated to the back burner for most individuals, and how to get started on building a retirement corpus.

Ashok Kanawala, Head – Products and Business Development, HDFC Asset Management, explains why planning for retirement has been relegated to the back burner for most individuals, and how to get started on building a retirement corpus.

1. Are Indians in general, under-invested when it comes to planning for their retirement? Why is this the case?

Yes. As per Morningstar data, India’s retirement savings as a percentage of the GDP is less than 2 per cent. For developed nations like USA and Australia, this figure is 125 per cent and 85 per cent respectively. This indicates an overall lack of awareness when it comes to retirement planning.

Retired life happens to be the last chronologically, and hence, financial planning for the sunset years tends to get postponed. Sometimes, a young individual who is early in his career tends to ignore the importance of retirement corpus either due to a lack of awareness, or simply by thinking that retired life is far in the future, or he may face occasions that require large expenditure in meeting social responsibilities, personal aspirations, or he may overspend, leaving little money left for retired life.

Retirement is a phase of life that is inevitable. One may be able to postpone retirement by a few years; but it is not possible to avoid it. One needs to remember that joint families are increasingly becoming rare, and one needs to be financially independent post 60 without having to depend on other family members. Increased life expectancy now also means a longer retired life, requiring a larger retirement corpus. How people spend their retirement years is also changing with aspirations to travel the world or to pursue hobbies that require financial readiness.

People also tend to underestimate inflation and its detrimental effects while planning for retirement. Inflation impacts us two ways. The first is through the increasing prices of goods and services we consume in our current lifestyle. The second is that our lifestyle itself changes calling for increased expenses towards newer necessities. Yesterday’s things of luxury have become today’s necessities. If an individual, at retirement, finds himself not able to afford his current needs, or in other words, has to go back to his earlier lifestyle, it would involve a huge mental setback. One needs to provision for such an improved standard of living while planning for retirement. There is also the uncertainty of the time-frame of retired life. So, it is essential to be conservative, and to have a buffer while targeting retirement corpus.

2. There are two stages to retirement planning. One is saving up for retirement, and the other, getting regular income. What should be the approach for these stages?

The working life of an individual that typically spans from age of 25 till 60 could be termed as the Earning and Accumulation Phase. During this period, the investor needs to allocate funds specifically meant for retirement.

An ideal way of planning for retirement could be as illustrated below:

• Starting an SIP with a reasonable goal in mind at an early stage of your career. It ensures that regular investments are made regardless of market cycles towards saving for retirement.

• Ensure that this SIP amount is topped up regularly as your income increases over time. Do not touch the retirement corpus for meeting other personal or social commitments.

• Switch gradually to assets with lesser volatility as you age and take on more responsibilities.

• Continue your topped up SIPs till retirement. Add lump sums along the way if possible.

Upon retirement, the individual’s income stops, and this phase of life can be termed as ‘Distribution Phase’. In this stage, the plan of action could be as below:

• Identify a reasonable standard of living and the monthly costs associated.

• Create a periodic Systematic Withdrawal Plan (SWP) for the said amount which works as a tax-efficient pension scheme.

3. How early is good enough for retirement planning?

Start as early as possible. In investing, if your investment horizon is longer, time will work to your advantage. One can harness the power of compounding better by starting early.

For instance, a person starting to invest Rs. 5,000 per month from the age of 25 would have invested a total amount of Rs. 21 lakh till he reaches the age of 60. At 12 per cent p.a. compounding, he would have amassed a corpus of Rs. 3.2 crore at retirement. In contrast, a person starting to invest Rs. 7,000 per month from the age of 35 also would have invested a total amount of Rs. 21 lakh. But, he manages to build a corpus of only Rs. 1.3 crore, at 12 per cent p.a. compounding, when he reaches 60 years of age.

Further, the working years of Indians, on an average, is on the decline as they pursue higher studies until 25 or 26. The retirement years, however, is on the rise thanks to the improvement in medicine. Hence, savings is of utmost importance. A thumb rule can be that, if you are in your 20s, allocate at least 20 per cent of your monthly take-home towards retirement. As you grow older and as your income increases, you may want to deploy more. So, we go on to say that, in your 30s – save 30 per cent, in your 40s – save 40 per cent and as you near retirement in your 50s – save at least 50 per cent of your income for retired life.

The best time to start retirement planning is on the day you receive your first pay check. In the words of Warren Buffet, “Do not save what is left after spending, but spend what is left after saving”.

4. In traditional retirement plans such as a Provident Fund (PF) there is hardly any component of equity. How much can this impact one’s planning?

Wealth creation in the long term primarily depends on two factors – the investment horizon and the rate of compounding. The first factor, time, is on our side since retirement is a long-term objective. The rate of compounding, the second factor, depends on how wisely you choose your assets.

An investment of Rs. 1 lakh for 30 years would grow to over Rs. 10 lakh at 8 per cent compounding, which is approximately the returns expected from risk-free investments. At 15 per cent compounding, the investment of Rs. 1 lakh would grow to a staggering amount of over Rs. 66 lakh in 30 years. If you look at the historical returns of equities, the S&P BSE SENSEX has compounded at nearly 15 per cent over the past 25 years (Source: CLSA).

One should not shy away from equities, branding them to be risky investments. Equities can be volatile in the short term. However, as your holding period increases, the volatility reduces. One needs to create a portfolio of assets that offers potentially higher returns as compared to the rate of inflation. Assuming an inflation rate of 7 per cent, which has been the case with India over the last 3 to 4 decades, an investment with a return of 8 per cent will yield you a real return of 1 per cent. Planning your retirement with investments that can potentially earn a positive real rate of return (read equities) would mean improved standard of living post retirement.

Each asset class has a different risk-return profile, and there is no one-size-fits-all formula when it comes to asset allocation. The younger you are, higher is your risk taking ability, and so should be the equity exposure. As you age and approach retirement, the equity exposure can be brought down gradually.

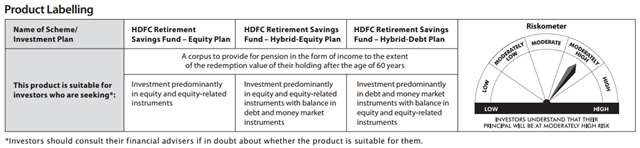

5. What does HDFC Retirement Savings Fund Offer?

HDFC Retirement Savings Fund, an open-ended notified tax savings cum pension scheme with no assured returns, targets the retirement corpus for an investor. The fund offers three different plans suitable for investors of different age groups and risk profiles. They are:

• Equity Plan: Suitable for younger investors with a relatively higher risk appetite with equity exposure between 80 per cent to 100 per cent.

• Hybrid Equity Plan: Suitable for middle-aged investors with a moderate risk appetite having equity exposure between 60 per cent to 80 per cent, and the rest invested in debt and money market instruments.

• Hybrid Debt Plan: Suitable for investors nearing retirement or investors with relatively low risk appetite. The exposure to debt and money market instruments is expected to be 70 per cent to 95 per cent and the equity exposure is expected to be between 5 per cent to 30 per cent.

Within equity, the focus will be on businesses with superior growth prospects and good management that are available at a reasonable price. Within debt, the fund will retain the flexibility to invest across all the debt and money market instruments of various maturities.

The fund has a lock-in period of five years from the date of allotment of units, during which the units cannot be redeemed or switched out. Upon completion of the lock-in period of five years, the units can be redeemed with an exit load of 1 per cent till the age of 60 for an investor. After completion of 60 years of age, the investor can redeem the units without any exit load. Post completion of the initial lock-in period of five years, the investor can switch between plans within the scheme without any exit load. The investments are eligible for tax benefits under section 80C of the Income Tax Act, 1961.

6. What is the fund’s strategy and what should be the holding time frame? How does one plan for post-retirement period with this investment?

Our offering is extremely long term in nature. The idea of holding period for retirement planning brings about the concept of mental accounting. When a person saves specifically for a particular target in mind, chances that he will withdraw from the corpus for any other purpose is lower. For instance, if a person wants to migrate to a bigger car resulting in a large outflow of money, he is likely to withdraw from an FD or an open ended mutual fund. But he is not likely to withdraw from the retirement corpus, like PF, that is specifically meant (mentally earmarked) for retirement.

HDFC Retirement Savings Fund targets the corpus intended for the retired life, and inherently brings about the discipline required as to stay invested in the fund until actual retirement. The fund requires three commitments from the investor’s end. They are to start saving early, invest regularly, and to stay invested until retirement.

Disclaimer: The views expressed are the author’s own views and are not necessarily those of HDFC Asset Management Company Limited. Any calculations made are approximations and are for illustrative purposes based on assumed figures. The information contained in this document is for general purposes only but it should not be construed as providing any kind of investment advice or as a substitute for any kind of financial planning. Mutual fund investments are subject to market risks, read all scheme related documents carefully.