Section 80C of the Income Tax Act of India specifies certain investments which allow you to avail income deduction and reduce your tax liability. ELSS mutual fund also known as tax-saving fund is one such specified instrument.

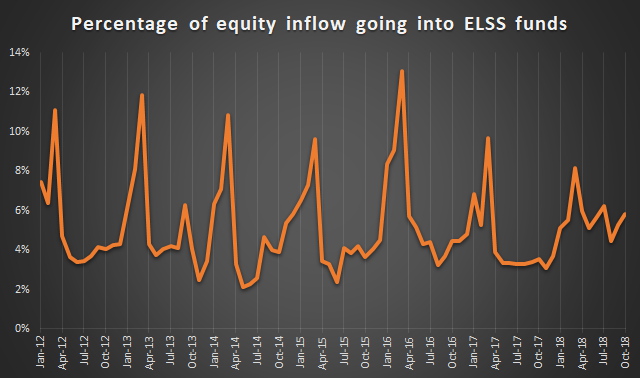

Investments can be made anytime during the financial year to gain this deduction. However, to assess your tax burden, employers might ask you to submit your tax planning a few months prior to the financial year end. And this is typically the time when investors rush to make their investments. The following graph shows how much of the money invested in equity mutual funds goes towards ELSS funds. The data has been taken month-wise.

The trend is clearly visible. Each year, there is a small spike in inflows in February, followed by a bigger spike in March, followed by a steep decline in April.

Investors put more money in ELSS funds during the month of February and March. The data confirms what financial advisors already know – most people don’t think about tax savings till the end of the year. However, there are two problems with this approach.

First is the problem of picking the wrong product to save taxes. Insurance and bank salesmen are especially active during these months. Because you don’t have time to carry out due diligence on the recommended products, you often go by the words of the salesmen. Consequently, you might end up buying insurance policies you don’t need, or put your money in poor returning bank FDs and PPF. By picking these products, you will forego gains which are higher than the amount of tax saved. As this article demonstrates, ELSS funds are the best product for your tax saving needs.

Even if you don’t make any mistakes in choosing the right product, there is a large element of timing risk when you invest in market-linked products like tax-saving funds. And that is the second problem with end-of-the-year approach to tax saving investments.

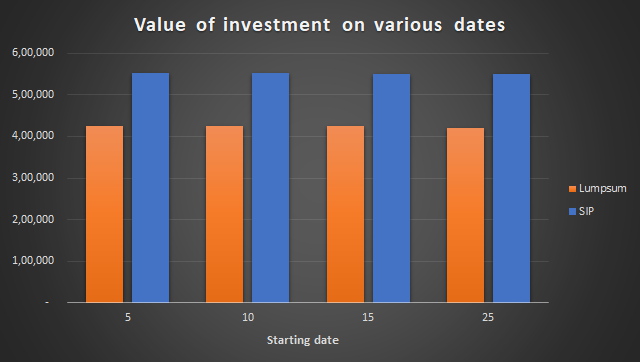

We analysed fund returns for an SIP of Rs. 5,000 through April to March every year and compared it to a lumpsum investment of Rs. 60,000 in March every year over the last 5 years. The following graph shows the difference between SIP and Lumpsum values based on various starting dates. These values are based on investments in Tata India Tax Savings fund. Fund selection is only for illustrative purpose and should not be taken as a recommendation.

Even though the graph shows only four dates, the SIP outperforms the lumpsum approach on all dates. Please note, dates beyond 28th have not been considered as SIP is not available on those dates.

So setting up a SIP helps you avoid the last minute rush while also making more money from you. It also:

- Saves you from missing the 31st March deadline

- Reduces the chances of you not having enough money when you want to invest

- Prevents you putting your money in an ill-suited financial product

But if your employer has issued a deadline now to show your tax prove and you don’t want the hassle of claiming it all when filing, here’s what you can do: invest a lump sum needed for your tax proof and start a SIP. This way, you will ensure that you start the process for future tax savings right away and also take advantage of the present market turbulence, especially pre-elections.

My saving habits were also used to be the same. Save only during Jan and Feb just to submit the tax saving investment proof to my employer.

But starting a SIP helped me to have disciplined approach towards savings. Thanks for the article

My saving habits were also used to be the same. Save only during Jan and Feb just to submit the tax saving investment proof to my employer.

But starting a SIP helped me to have disciplined approach towards savings. Thanks for the article