Hybrid funds combine the growth prospects of equity with the stability of debt to try to deliver returns with lower volatility.

Among hybrid funds – those with a bias for equity are called hybrid aggressive funds (earlier called equity-oriented funds). Those with more debt are called hybrid conservative funds (earlier called MIP or debt-oriented funds). Over the last few years, a new type of hybrid funds have gained popularity. These hybrid funds employ derivative instruments, like futures and options, to hedge their portfolio, instead of using debt. The hedged portion of the portfolio essentially acts as debt, allowing the fund to lower the risk. At the same time, the unhedged portion generates higher returns. Essentially they are equity-oriented in their portfolio but come with risks similar to debt-oriented funds.

So hybrid low risk funds can be classified as under:

| Category | Classification | Equity | Debt | Tax Treatment |

|---|---|---|---|---|

| Conservative hybrid | Debt-oriented | 10-25% | 75-90% | ST – Marginal rate LT – 20% with indexation* |

| Equity savings | Equity-oriented | Minimum 65%, partially or fully hedged | Minimum 10% | ST – 15% LT – 10% |

| Dynamic asset allocation or balanced advantage | Equity-oriented | Dynamic | Dynamic | ST – 15% LT – 10% |

*10% without indexation for NRIs

While all of the above seek to reduce volatility, they achieve this in different ways. Conservative hybrid funds invest a maximum of 25% of their assets in equity and the remaining goes into debt. Equity savings and balanced advantage funds, on the other hand, typically invest at least 65% of their holdings in equity and hedge a part of it using derivative instruments. Some portion is also invested in debt.

Let’s compare how these funds achieve the job of containing downsides/volatility in different ways.

How have they performed

Volatility and downside containment

The general theory that debt reduces risk in a portfolio is true of hybrid conservative funds as well. This category of funds appears to be marginally better than equity savings funds in containing downsides. The standard deviation of monthly rolling returns over a 3-year period, is slightly lower for conservative hybrid funds as compared to equity savings funds (4.1 vs. 4.7). Given the higher equity exposure of balanced advantage funds, it is no surprise that their annualised risk is highest at 6.7. However, the median probability of getting negative returns on a 1-month basis is pretty much the same for conservative hybrid and equity savings funds at a little over 25%. It slightly higher in balanced advantage funds at 30%.

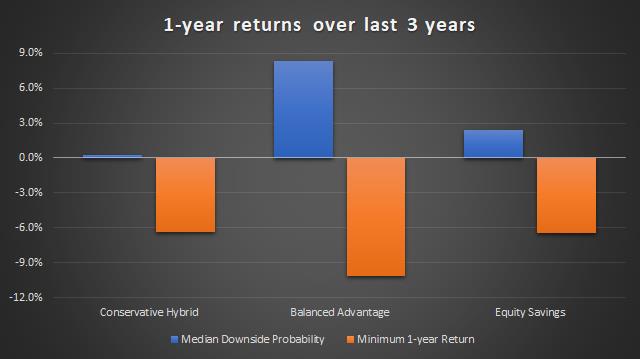

On a rolling 1-year basis though, conservative hybrid funds fare much better than their equity counterparts. The median downside probability of the category is a mere 0.3% while those of equity savings and balanced advantage funds are 2.4% and 8.3% respectively. The extent to which conservative hybrid funds can fall is also lower. The worst 1-year return by a conservative hybrid fund was -6.3% (-4.1% if we ignore funds affected by the IL&FS crisis), whereas those of equity savings and balanced advantage were -6.5% and -10.2% respectively.

Returns

It is mostly clear that even after considering the debt crisis, debt-oriented hybrid funds have a lower risk. But does the higher risk of equity funds translate into higher returns as well?

1-year returns from debt oriented hybrid funds have gone as high as 25.1% during the past 3 years, while those of balanced advantage funds have gone up to 40.3%. The category average of 1-year rolling returns for the last 3 years shows balanced advantage funds in the lead.

So prima facie, it seems balanced advantage funds are indeed providing better returns for the risk. This is not surprising considering that their net exposure to equity is way higher. However, to substantiate this claim, we need to look at the risk adjusted returns. We do this by looking at the sharpe ratio. The following table shows the Sharpe ratio based on 1-year rolling returns over the past 3 years. Here it is evident that the equity-biased funds did better.

| Conservative Hybrid | Equity Savings | Balanced Advantage | |

|---|---|---|---|

| Average returns | 7.55% | 6.95% | 8.64% |

| Median Sharpe Ratio | 0.23 | 0.27 | 0.32 |

But there’s another angle to it as well. Most of these funds are held for a period shorter than 3 years. So while conservative hybrid funds will get taxed at your slab rate, equity-oriented hybrid funds will either be taxed at 15% (for holding period of less than one year) or can be tax free (for holding period of more than a year up to gains of Rs. 1 Lakh) or be taxed at just 10%. So the post tax returns differential may well work out to be higher.

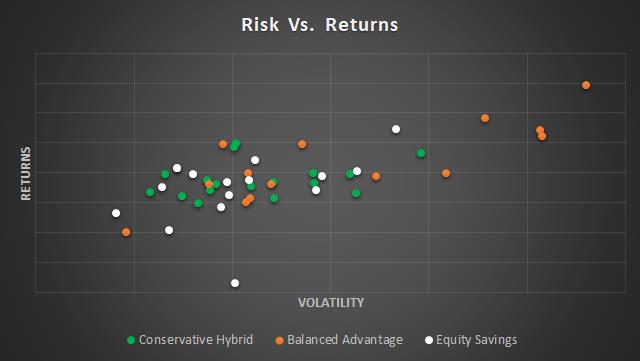

Here is a scatter plot showing risk vs. returns of all the three categories of funds. We can see that the debt-oriented funds are relatively close in their risk returns characteristics while the equity-oriented funds are more spread out.

The risk in low-risk options

It is often assumed that equity = risk. But when the equity portion is hedged, the risk is partly negated. However, the upside returns are also capped. This is what hybrid funds with derivatives do.

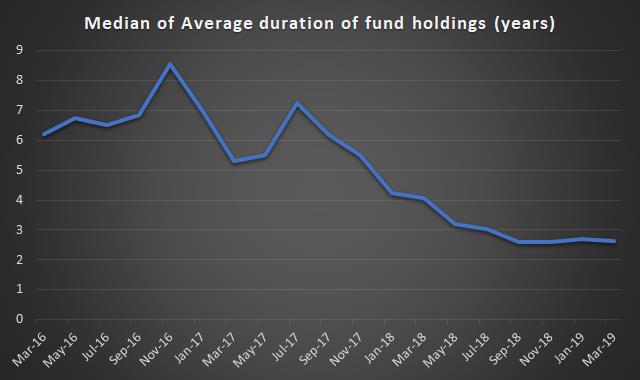

With debt forming the major portion of conservative hybrid funds, they are not without risks. Interest rate risk and credit risk can hurt this category of funds. For instance, in early 2018, when the bond yields had been rising and equity markets turned bearish, hybrid conservative funds with higher average duration fell more. HSBC Regular Savings, SBI Debt Hybrid, and Invesco India Regular Savings were consistently underperforming their category during February and March of 2018. Invesco and SBI managed to reduce their duration exposure quickly, while HSBC has continued to maintain above average duration. The median of the average duration of funds in this category has come down from its peak of 8.55 years in November 2016 to 2.62 years at present.

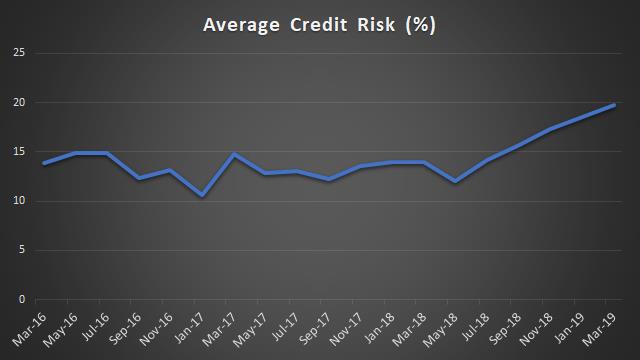

With the turbulence seen in the debt market over the past few months after credit crisis of IL&FS, credit quality of the debt holdings in hybrid conervative also gains importance. Funds like DSP Regular Savings and Aditya Birla Sun Life Regular Savings have suffered significantly due to the IL&FS crisis. Both these funds have given negative returns on a 1-year basis. More recently, more hybrid funds were hurt by downgrades in the Reliance ADAG group papers.

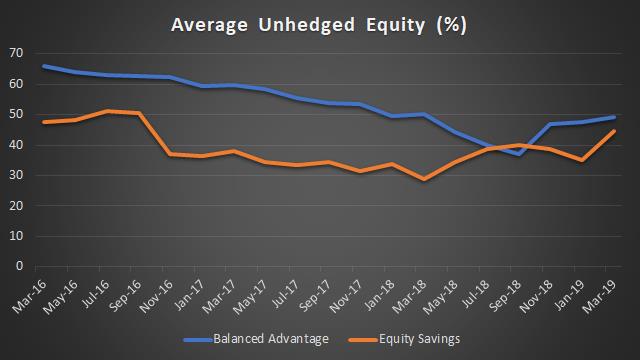

As for the equity-oriented funds, the risk comes primarily from their unhedged equity holdings. Here the average equity holdings of balanced advantage category tend to be higher as compared to that of equity savings funds. However, the percentage of unhedged equity holdings varies considerably across funds even within the same category. Typically, balanced advantage funds have a higher portion unhedged comapred with equity savings funds. Also, within the equity savings category, the unhedged equity holdings vary from 34.8% in Tata Equity Savings to 72% in IDBI Equity savings. However, due to a clearer definition of the requirements by SEBI, we see lesser variation in equity savings funds.

Suitability

The low-risk hybrid options discussed above are meant to be held for 2-3 years. However, which category is suitable for whom would depend on the risk appetite, the purpose of the fund in the portfolio and taxable bracket of the investor. Talk to your FundsIndia advisor to know whether you should stick to the traditional hybrid conservative (earlier called MIP) or do for the low risk equity-oriented options.