Bad news all around..

Coronavirus still not under control..

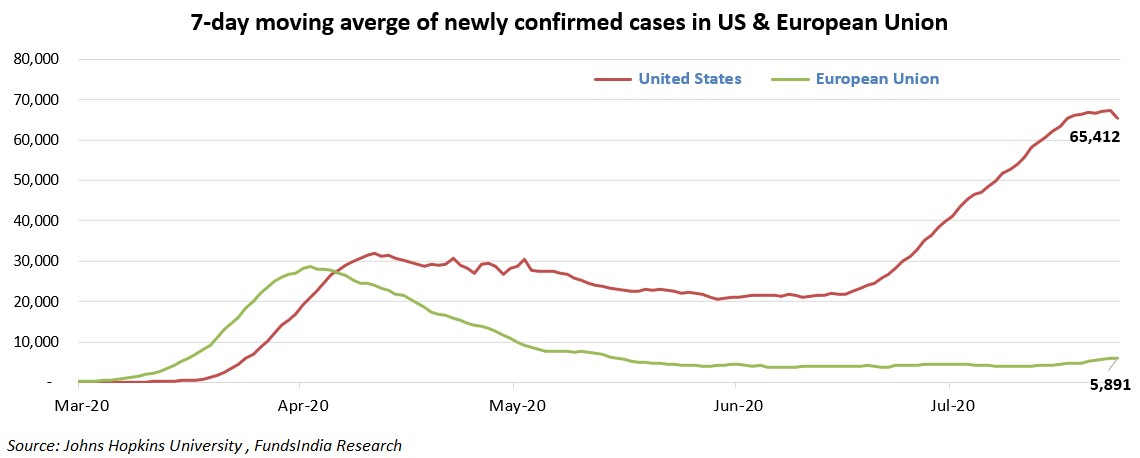

While the outbreak appears to be under control in European Union, the United States is currently facing a resurgence of new infections.

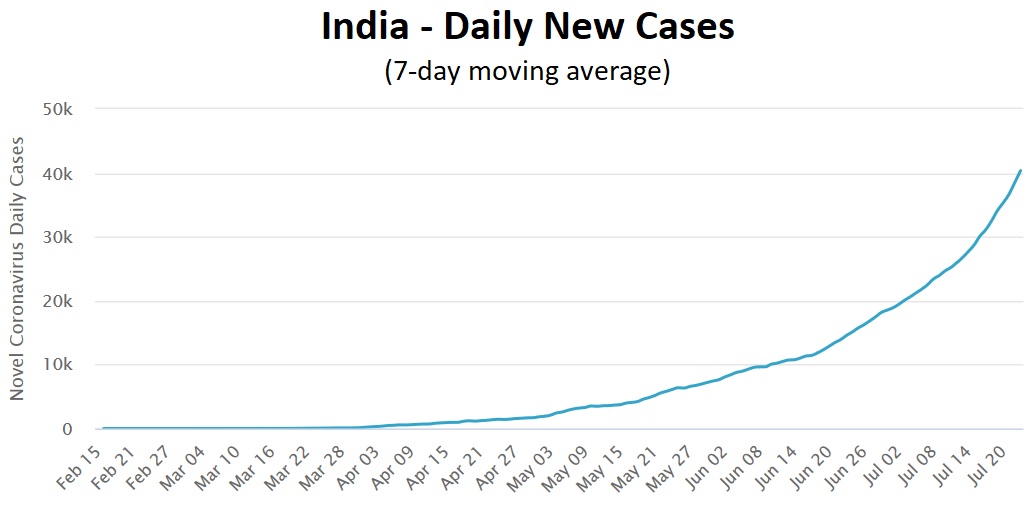

Infections continue to increase in India.

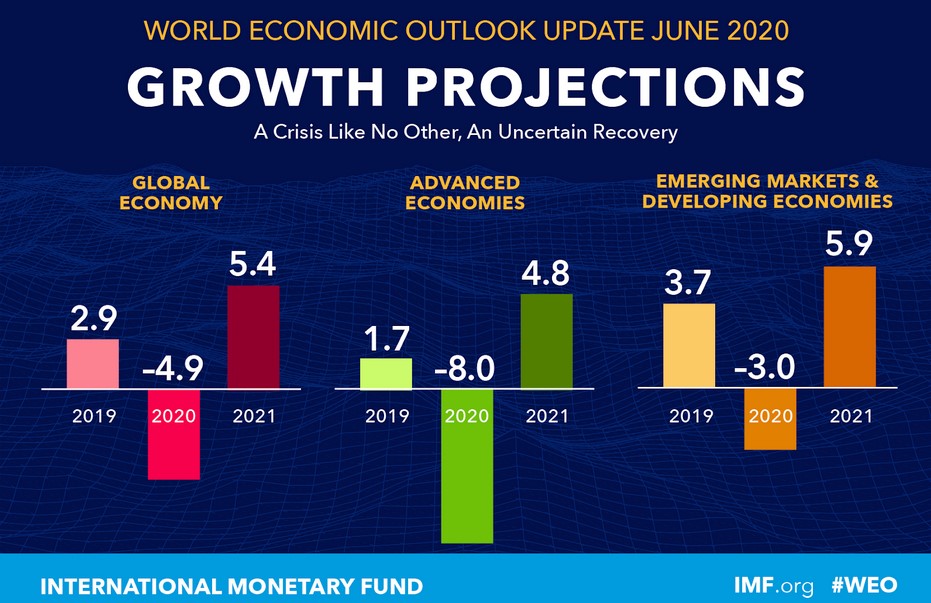

Economic Slowdown across the Globe..

IMF expects Indian GDP to contract by 4.5% for FY21 followed by a recovery of 6% in FY22. While different think tanks have come out with different projection numbers, broadly the consensus is that the Indian GDP will contract for FY21.

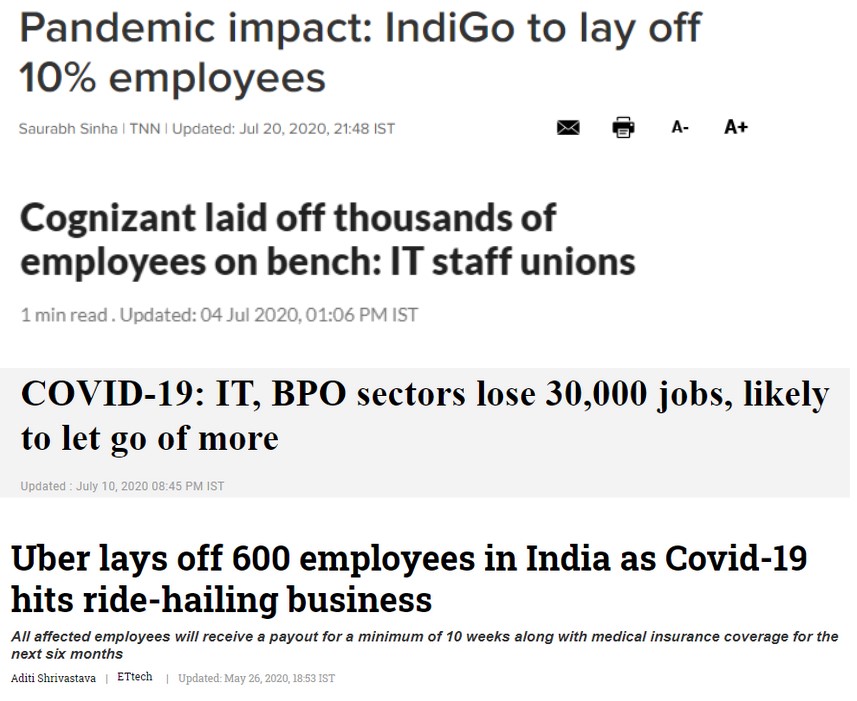

Job losses and Pay cuts..

Here are some of the media headlines which reflect the mood of the current situation

So what happened to equity markets?

A whopping 46% up since 23-Mar-2020..

Now you are like..

Can someone care to explain what is happening?

Making Sense of the market

1. ‘Better or Worse’ tends to matter more than ‘Good or Bad’!

When it comes to the relationship between economic data and stock market behavior, “better or worse tends to matter more than good or bad.”

So the key question to ask is not if the economy is good or bad but rather is it getting better or worse?

Trend 1: Economy showing initial signs of normalising

- Nomura India’s business resumption index shows initial trends of business resumption

- India’s manufacturing PMI Index has also improved from 27.4 in Apr-20, 30.8 in May-20 to 47.2 in Jun-20

- GST collection in Jun-20 at ~Rs 91,000 crore was almost three times more than ~Rs 32,000 crore in the month of Apr-20

- Indicators like power consumption, e-way bill generation, petrol & diesel consumption and electronic toll collections showed improvements in Jun-20

- India’s unemployment rate fell rapidly to near pre-covid levels from 27.1% as of 03-May-20 to 7.9% on 19-Jul-20

These are early signs that the overall economy is normalising as the worst of lockdowns are most likely behind us.

Trend 2: Rural India is recovering faster than Urban India

Rural India’s economic recovery has been supported by a good monsoon season, lower intensity of lockdowns and virus spread.

This is getting reflected in the data as seen below –

a) Good Monsoon: The rabi season output was higher than the advanced estimate and the monsoon has been 20% above normal.

b) Higher Fertiliser Sales: Fertiliser sales jumped 83% for Apr-Jun quarter vs last year

c) Significant pickup in Tractor Registrations: Domestic tractor sales growth, often regarded as a chief proxy to gauge health of rural economy recovered sharply relative to other auto segments (22% YoY in Jun-20 compared to a 4% growth in the previous month).

d) Unemployment rate is coming down much faster: Rural unemployment rate (7.1%) is better than urban unemployment rate (9.8%)

e) Cement sales and two-wheeler sales are normalising

f) Higher MNREGA allocation and MSP hike

g) Long Term structural measures to increase farm income

- Removing the Essential Commodities Act

- Freeing up the APMC market

- Supporting contract farming

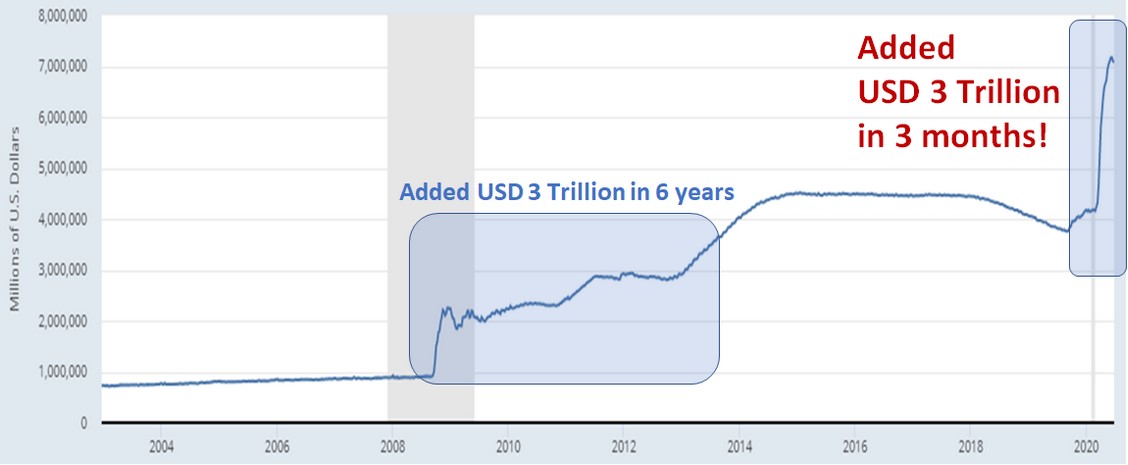

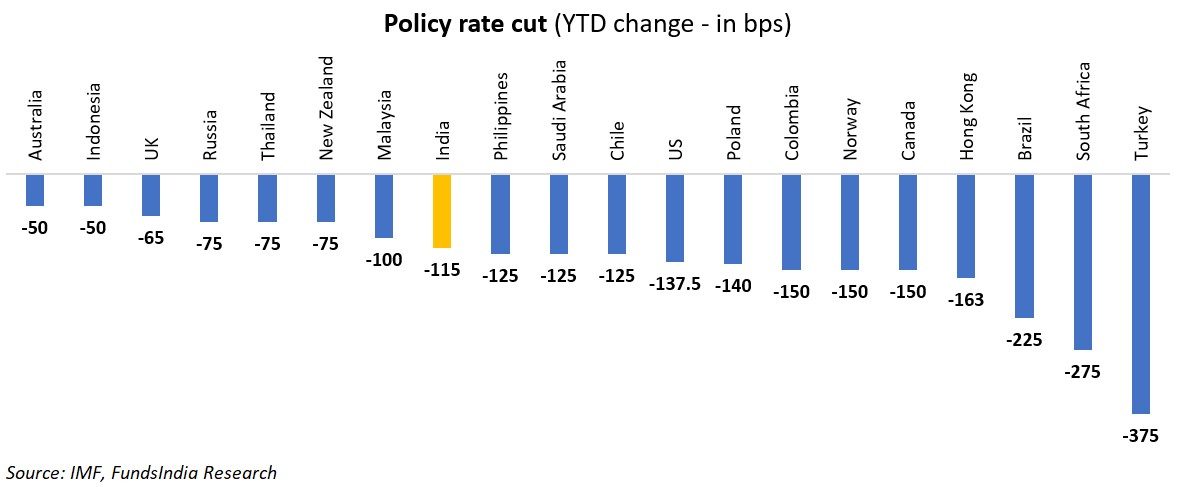

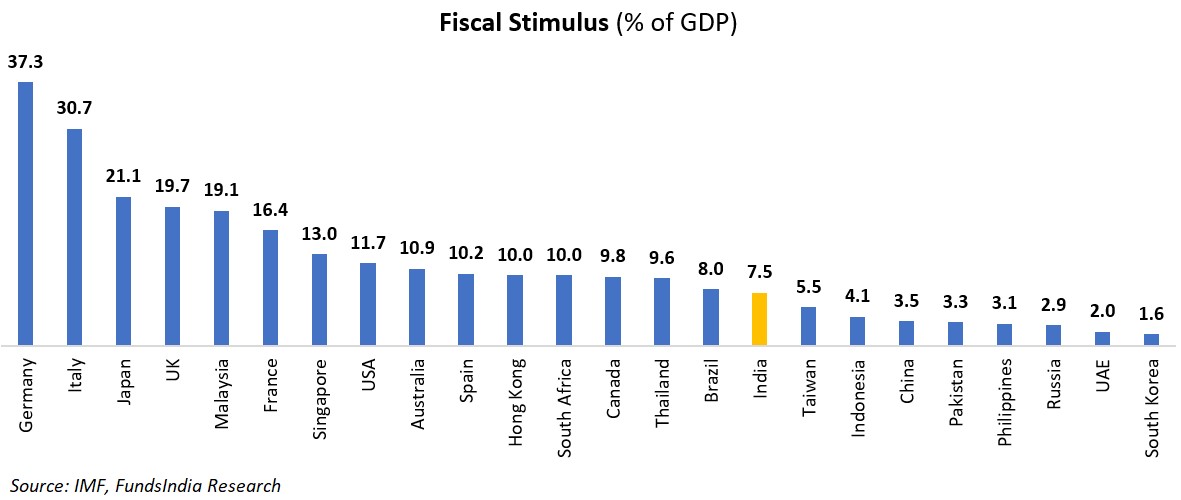

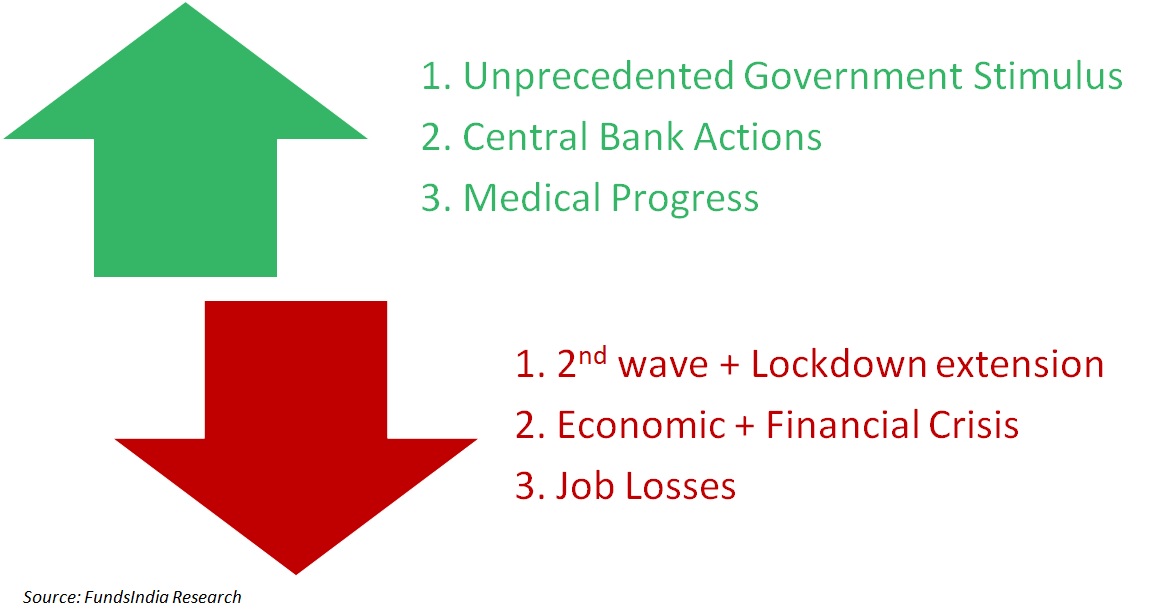

2. Significant Stimulus from Global Central Banks & Governments

Central Banks globally reacted promptly by announcing policy rate cuts to support growth..

Massive fiscal & monetary stimulus has been witnessed across the world..

These interventions have been a combination of:

- Direct cash transfers

- Support to business in the form of cheap loans

- Injection of liquidity by Central Banks

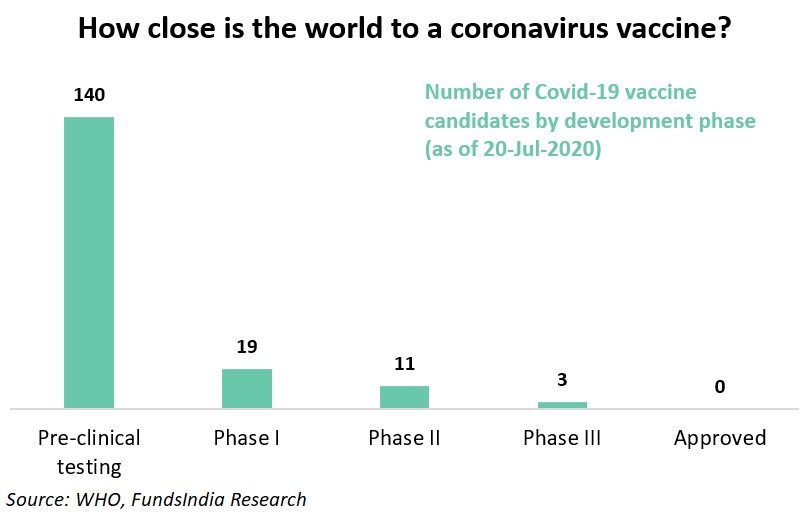

3. Medical Progress continues

- Researchers worldwide are racing to develop and test a vaccine for the coronavirus

- Many coronavirus vaccine have reported promising results in early stage trials

- 3 vaccines are in the final phase 3 stage

Putting all this together

The above three factors together have counteracted the near term concerns on virus spread, weak economic growth and job losses.

This has led to the significant recovery in the equity markets.

What are the markets factoring in the expectations?

The equity markets are usually not focused on what is happening now, but are more about what is going to happen next.

Let us find out what the markets are pricing in..

- Continued global liquidity driven by both Central Bank and Government Stimulus

- Resumption of normal economic activities with a medical solution to the Covid-19 in the near term (within next 6 months)

- While economic growth for this fiscal year will be negative, the Fiscal and Monetary stimulus announced by the Government and the Reserve Bank of India is expected to lay the foundation for a strong rebound in FY22 GDP growth

- The market is pricing in flows from FPIs (foreign portfolio investments) due to increase in India’s weight in the MSCI and FTSE Index

If the actual scenario plays out to be better than what is priced by the market, the equity market can rise from here. If the actual scenario plays out worse than what is priced by the market, equity markets may fall from the current level.

What can go wrong?

- 2nd wave of virus leading to further lockdowns

- US Elections: The current opinion polls in the US point to a change in the Presidency from supposedly market friendly Republicans to higher tax mandate of Democrats.

- US-China Tensions

- India China Border Dispute

How do we prepare?

1. Base Case

In our base case we are looking at 2 phases

– Phase 1 (current phase) – Liquidity driven rally where there is a valuation rerating primarily led by global liquidity and perception change from “extremely bad” to “bad”

– Phase 2: Eventually fundamentals will have to catch up. Earnings growth led by economic recovery will be required for the current rally to sustain. A medical solution over the next 6 months remains the key

- Valuations (except for PE ratio due to depressed earnings) remain close to long term average (measured via MCAP/GDP, Price to Book)

- Earnings growth are at cyclical lows – we expect earnings growth to pick up over the next 3-5 years led by low base, low interest rates, pick up in credit growth, lower corporate taxation, low commodity prices aiding margins

- Overall, we continue to suggest investing at your long term equity allocation levels with a 5 year view – at the current levels valuations are not high enough to go underweight nor are they low enough to go overweight

- That being said, the markets may remain volatile in the near term as earnings growth may be patchy and will continue to be driven by news flows

2. Humility – “We can’t predict”

While we laid out our base case above, the honest truth is there are still several questions for which no one has clear answers:

- How will the virus spread in the coming months?

- When will a treatment that improves the mortality rate be discovered?

- When will we get a vaccine?

Without any certainty on any of these issues, no one can have any certainty about the near-future performance of the market. Anyone who makes a prediction with any certainty as to how the market will perform over the next 3 to 12 months is making a (hopefully intelligent) guess.

While over the long run, the market is fairly predictable, over the short run, it is never predictable, especially in times like this when there are a lot of unknowns.

So in a situation like this, it is always better to prepare for different outcomes rather than trying to predict and position for a precise outcome.

3. How to prepare?

– Build an Emergency Fund in safe high quality lower duration debt funds covering 1 year of your expenses

– For goals that are nearing (read as less than 5 years) – avoid equity allocation

– Revisit your risk profile – Here is a quick practical way to re-evaluate your risk profile. During the recent equity market crash, if you

- Sold: low risk tolerance

- Held: moderate risk tolerance

- Bought more: high risk tolerance

- Bought more and hoped for further declines: very high risk tolerance

– Stick to your long term asset allocation – not the time for underweight or overweight equities

- For example, if at the start of the year you had 50% in Equities and 50% in Debt in line with your long term asset allocation, continue with the same asset allocation. Do not overweight and make your equity allocation to say 65% or underweight and make it to say 35%.

– ‘What if things go wrong’ plan – Keep a written plan of action ready on how to act if the market starts correcting

- If markets are down -20% from previous peak (i.e Sensex at 34,000)

- If markets are down -30% from previous peak (i.e Sensex at 30,000)

- If markets are down -40% from previous peak (i.e Sensex at 26,000)

– How to invest incremental money

a) Option 1: Invest in Balanced Advantage Fund over 3 month STP

b) Option 2:

1. Allocate as per Asset Allocation – Stagger Equity Allocation over 3-6 months – convert to one-time investment if market falls or a medical solution is announced

2. From the previous high,

- If markets decline by 25% i.e Sensex@32,000 – Invest up to 20% of your earmarked amount in equities.

- If markets decline by 30% i.e Sensex@30,000 – Invest up to 40% of your earmarked amount in equities.

- If markets decline by 35% i.e Sensex@28,000 – Invest up to 70% of your earmarked amount in equities.

- If markets decline by 40% i.e Sensex@26,000 – Invest up to 100% of your earmarked amount in equities

This in a nutshell is how we are navigating and adapting to the current market conditions.

As always happy investing 🙂

Thanks for Sharing this nice blog, It’s so helpful for equity investor

Thanks for Sharing this nice blog, It’s so helpful for equity investor