A second policy rate hike by RBI, last week, coming on the back of a hike only 2 months ago, was surprising for some. But markets seemed prepared for it. As inflation concerns heightened, RBI hiked the repo rate by 25 basis points to 6.5%. Repo rate is the rate at which RBI lends money to commercial banks. How is that of interest to a retail investor?

Repo rate is the rate at which RBI makes available funds to banks. If this goes up, it essentially means that RBI is making borrowing dearer. It should therefore follow that all lending rates also go up. But this is not a simple equation. At a time when banks are not finding enough takers for their loans, there is little space for banks to hike rates. That also means that deposit rates will not go up in a hurry. But meanwhile, as more credit requirements come to the debt market, this space can be more responsive to the RBI rate hikes and they are already showing such signs. Let’s see how.

Debt funds turn attractive

Debt funds invest in instruments such as commercial papers, certificate of deposits, corporate bonds and government securities. Rise in borrowing rates in the economy also translates to higher coupon rates on these instruments. Accrual based funds which generates returns mainly from the interest income are set to benefit from these higher coupons.

There are different categories of debt funds which invest across maturities. Liquid and ultra short term funds invest in instruments which mature in less than a year and are suitable for really short term needs. Likewise, short term funds invest in papers of 1-2 maturities and so on.

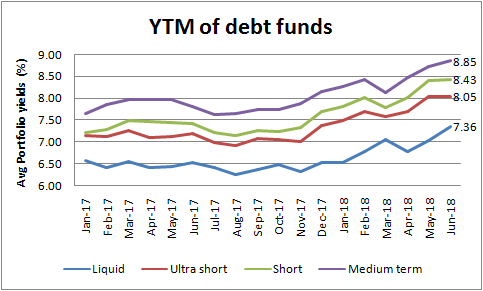

Yields on the rise

Looking at the portfolio yields tell us how attractive portfolio yields have become. Portfolio yield-to-maturity is the return from a fund if all the underlying instruments are held till maturity.

All through 2016, yields were trending lower due to multiple reasons such as abundant liquidity, lower inflation and prospects of rate cuts. Most of 2017 saw yields remain low. But from December 2017, mutual funds saw their average YTM climb up. This was at an uncertain time where the bond market was building in a higher rate scenario although there was no direction from RBI then. That essentially means that the debt markets started anticipating rate hikes well before it actually happened. It therefore follows that the debt fund portfolios have started getting more lucrative even before the RBI rate hike started.

Liquid funds, which are least risky and most liquid, held papers with an average YTM of 7.4% as of June 2018, compared with YTM of 6.5% in December 2017. The coupon is more attractive with longer duration accrual funds. With RBI’s rate hike acting as a signal for direction of rates, it is clear that bond yields may at least stabilise to this new level if not move higher. This makes debt funds an attractive option for investors looking for low risk investments.

The yields given above will tell you, that even post expense ratios, debt funds will sport far higher portfolio yields than traditional bank deposits. Instead of focusing on the past returns of debt funds, check for the portfolio yields to know what is the interest rate of instruments that the funds hold.