Recent news headlines have been giddily declaring new market highs – ‘the Sensex is nearing its January peak’, ‘now its past that’, ‘now is 36,500’, ‘now its broken through 37,000’. When it comes to equity funds though, it doesn’t seem to be reflecting all that rally. Why? Should you worry?

In a nutshell, here is what is happening:

- The rally being seen in the Nifty 50 and the Sensex is not reflecting across the market.

- Funds’ strategy of according weights to different sectors and stocks will necessarily mean they invest in a larger basket of stocks. As the market rally is narrow, most stocks will be underperforming.

- The phenomenon of funds lagging main indices this year is not isolated to this year alone. With funds basing investment decisions on metrics such as fundamental business strength and valuations,they had reason to turn cautious over the past two years. This has caused fund underperformance earlier too as the market rally got more exuberant.

- Midcap and smallcap funds are actually better this year than they were last year. The underperformance has deepened in the large-cap and multicap segments.

Rally centred around few stocks

Look at the table below to see the difference between index returns and the returns of underlying stocks. The S&P BSE 100 has returned 10.2% in the last one year. But the underlying stocks have delivered much lower, if we simply take the average returns of these 100 stocks. Why was this so? In the BSE 100 index, if we take the top 30 stocks based on their market caps, half of them have returned more than 20% in the past year. If we take all the 100 stocks the number is only 32, which is only one-third. With 15 of these 32 stocks concentrated at the top, they have a high weightage in the index, pulling it up. BSE 100 and BSE 500 are reflecting the skew because of this reason.

The index and its returns are weighted to marketcap of the constituent stocks. If this weight is removed, the average returns of all 100 stocks in the index falls to 6.3%. 46 out of 100 stocks have actually have gone down during the period.

Now consider the BSE 500. Half the stocks that make up this index are loss-making on a 1-year basis and 70% of them is in losses on a year-to-date basis. While the BSE 100 is up 5.7% YTD, the BSE 500 is up a lower 2.6%. The BSE Midcap and the BSE Smallcap indices also trail the BSE 100 index. The table below summarises some of this.

| 1-year return | Avg. 1-year return of underlying stocks | Stocks delivering 1-year losses | |

|---|---|---|---|

| S&P BSE 100 | 10.2% | 4.1% | 46 out of 100 or 46% |

| S&P BSE 500 | 8.9% | 5.0% | 255 out of 500 or 51% |

| Returns as of 25th July, 2018 | |||

What does this tell us?

- The market rally is focused on a few stocks alone and which are pulling up index levels. Some of the performers are those with higher weight in the both the BSE 100 and the BSE 500 indices, such as TCS, Reliance Industries, HDFC Bank and Infosys. The index’s returns are therefore not reflecting in the majority of the index constituents. In the BSE 100, just 40% of the stocks have delivered index-plus returns.

- Of the stocks that have rallied, several are in the large-cap segment. Midcap index returns of 2.9% and the average 2.7% of underlying constituents are more or less similar, in the past one year. This is because with midcaps, the correction is still continuing.

- There is a dichotomy in market movement with some stocks rising and most others flat or falling. The majority of the stocks in the market are therefore not doing as well as the Sensex or Nifty 50 returns imply.

Should the underperformance worry you?

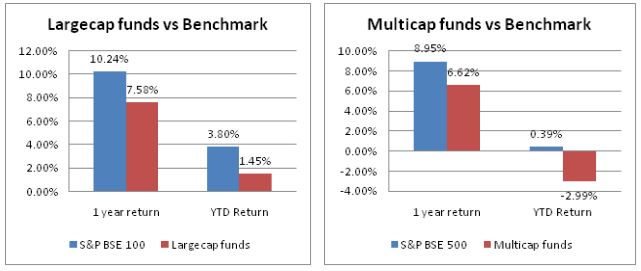

In an earlier post, we had addressed the slide in mid-cap fund performance. In that article, we had noted that mid-cap funds are doing better this year than they were in 2017. For large-cap and multi-cap funds (including the various categories such as value, focused, large-and-midcap, and so on), however, recent returns are faltering. Considering average returns, both the categories are underperfoming the indices in the short term.

Returns as of 25th July, 2018. Categories have been grouped into large-cap and multi-cap based on portfolio marketcaps.

Returns as of 25th July, 2018. Categories have been grouped into large-cap and multi-cap based on portfolio marketcaps.

But we can’t be quick to ascribe this underperformance to sub-optimal investment choices by funds. This has more to do with the nature of the market rally, funds strategy, and caution on part of fund managers.

First, as we’ve seen, the market rally has not been broad-based. Fund strategy is going to see them invest across stocks; they are hardly going to invest in only those that rallied. With more laggards than gainers, it is inevitable that several stocks that funds own would be poor performers and drag fund returns lower. When we compare a fund to its benchmark, we are seeing if a fund manager’s selection is better than simply buying an index which will have stocks weighted to its market cap. In a narrow market like this, with only a few stocks generating very high returns, the indices become a skewed representation of the market.

Next, in the stocks that have rallied sharply and have high index weights, funds already have high exposures which cannot be increased further. In the BSE 1o0, for example, HDFC Bank and Kotak Mahindra Bank have gained sharply, up 14% and 31% in the year to date. The two stocks feature in the top holdings of most funds and funds cannot indiscriminately lift the holdings here and reduce it in other stocks. For example, Franklin India Bluechip, Motilal Oswal Focused 25, Mirae Asset India Equity, SBI Bluechip and such have 8-9% of their portfolios in HDFC Bank. They would not be able to raise it still further. Similar trends emerge in stocks such as Kotak Mahindra Bank or IndusInd Bank, where exposures are around 4-5% for several funds.

Third, with the lack of a sector-wide trend gains may have been offset by losses in others. In the rally, there are no clear sector trends barring software. There are some pharma stocks that have rallied, some FMCG, some auto, some capital goods, some banks. With the steady rally over the past four years, sector-wide trends have slowly given way to stock-specific trends. So while Reliance Industries gained, ONGC, HPCL, IOCL have lost. Aditya Birla Sun Life Frontline Equity holds both Reliance Industries and ONGC as do ICICI Prudential Bluechip and HDFC Top 100. Similarly, funds that held good performers Mahindra & Mahindra or Maruti Suzuki along with stocks such as Tata Motors, Bajaj Auto, Eicher Motors or Motherson Sumi Systems may have not benefited much from the gainers.

Fourth, funds have been cautious. The steady market rally since 2014 has lifted valuations of several stocks without any strong growth in underlying earnings. It has also lifted stocks without strong fundamentals. Quality funds go by metrics such as earnings visibility, profitability, valuations and so on. This saw them turn cautious a long time ago, staying away from several of the gainers. For instance, Hindustan Unilever is a massive outperformer; its valuations have also skyrocketed to 69 times trailing 12-month earnings. Bajaj Finance has seen its consolidated price-to-book an expensive 8.95 times.

Funds have instead preferred more value-based stocks such as ITC, several from the power space such as Power Grid Corporation and NTPC, cement stocks such as Ultra Tech and ACC, telecom stocks, and have maintained exposure to commodity stocks such as Vedanta and Tata Steel.

Funds have also been cautious on adding too much to riskier outperformers such as Graphite India, Jubilant Foodworks, Mphasis, Page Industries, Tata Elxsi, Biocon, Godrej Properties. They have stayed away from massive but extremely risky gainers such as Meghmani Organics, Bombay Dyeing or Indiabulls Ventures. This is prudent given that such stocks can give up gains equally quickly as was the case with other market momentum favourites Rain Industries, Manpasand Beverages, Can Fin Homes or PC Jewellers.

In fact, funds have been wary of the market for a long time now. From around end-2016 onwards, more and more funds began lagging their benchmarks as they turned cautious of the market rally. While this prudence has paid off well for mid-cap and small-cap funds in the recent correction, it is yet to be seen in large-cap and multi-cap funds.

What should you do

- Stay invested. Stock markets have been running on steam without a strong underlying growth. Fund caution in the face of an irrational market has led to the current underperformance. Such blips are par for the course and will even out over the next few years. The correction in the broader market will help bring valuations and expectations back in line. That fund managers are toeing the line of caution clearly distinguishes their strategy from pure trading strategy that equity traders may follow. For long-term wealth-building, holding on to rationality is the only way.

- Don’t try to switch funds citing a 1-year underperformance. This is a time when ill-founded advice on churning portfolios will be aplenty as funds flounder. You may be tempted to go behind funds that have outperformed in recent times. But remember this: Funds that are currently doing well are primarily because they hold higher weights to the few stocks gainers. Axis Bluechip, Invesco India Largecap, or Canara Robeco Bluechip are such examples. But remember, these funds made those returns from those stocks that are now very high on valuations. Their ability to repeat the feat therefore stands reduced.

This is not to undermine the influence of fund strategy and choice of stocks. It is just that simply going by the top performers is going to result in constant churn and chasing returns that eventually turn out to be detrimental to your portfolio. Switching out to chart toppers is even less sensible a tactic in a narrow market.

As long as you hold an otherwise quality fund with a sound strategy, the recent slide in returns should not force you into changing funds or questioning markets. In the current market, looking at the benchmark to assess a fund’s short term performance no longer holds. Wait for a more rational market, where a larger number of stocks participate, before assessing your fund. When that is to be – we are always there to let you know!

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.