Okay folks, your gloom and doom picture is now complete as the month of August ends. The volatile equity and debt market and now the GDP numbers announced for the June quarter all provide a respectable funeral to a month that is best forgotten.

But as history suggests, you strike it rich only in a gloomy market. Agreed you are not going to mint money overnight and perhaps not even in a year’s time but just step back and take a look.

The earlier gloom

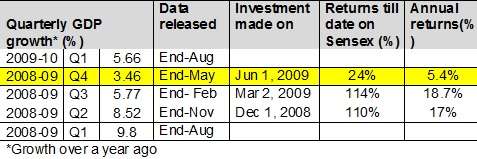

At 4.4% growth over a year ago numbers, the GDP at factor cost is lower than the 4.8% seen in the March quarter. Also, it is the lowest since the 3.5% growth seen in the March quarter of 2008-09. So let us take a leaf out of the 2008-09 gloom. (GDP data considered from 2004-05, when the new base came in to effect).

As seen in the table below, GDP growth started dipping in the 2nd quarter of 2008-09, that is from the quarter ending September 2008. GDP numbers are typically published 2 months after the quarter. Hence, the September quarter numbers would have been released on end-November 2008.

Yes, you would never have known if that was the bottom, but say you simply invested on December 1 (after the November end GDP release), guess what would be your returns today in the Sensex? An absolute 110% or an 17% annual return!

Very well, if you had missed that and waited for the December 2008 GDP numbers (released in February 2009), you would have managed slightly higher returns of 114% or 18.7% annually till date.

Please note that the returns would have been as good (about 2 percentage point lower annualized returns), even if you had invested sometime during the said months (given above) and not exactly on the day following the GDP announcement.

But yes, the markets actually hit their bottom much later, in early March 2009. But then the GDP data was released only in May.

Had you seen this very low GDP growth and invested on say June 1, then your annual returns would have been a mere 5.4%; simply because the markets never wait for the data! There were enough indications from the IIP and Purchasing Manager’s index, besides the many forecasts, for the market to move ahead of the release.

The lesson

You don’t really wait for the bottomed out economic numbers, to invest. Investing ahead helps you quite well.

No doubt, this time around, it has become extremely complex to decipher whether we are seeing the economy at its dumps, going by how the quarterly growth numbers have been swinging (see table below).

But seeing the deep trouble the economy is in and lack of quick fixes on various fronts (whether it is the depreciating rupee and current account deficit or the stubborn inflation), chances are that you will see some more pain points in the economy.

If that be the case, then the good news is that you have not missed an opportunity to invest. Perhaps the GDP for the September 2013 quarter will touch a low of 4%. So be it. If past data is anything, it simply means you need not wait till such a low.

Strategy

Agreed, it’s all easier said on hindsight. But if you are the kind who believes that there are opportunities in gloom, then you should probably be investing now.

While it goes without saying that you need to keep your SIPs going, if you are interested in investing lump sums, set aside a portion and split them into three. Invest them at every dip of 3-5% in the index or simply invest one part right away (in case you are not aware, the Sensex is down over 8% from the high (in July) thus far in 2013. Average with a 3-5% fall.

What happens if the markets fall more even after you average? Stay put. Past lessons suggest that you do not have to time to a ‘T’. Investing between September and December of 2008, for instance, was good enough even as the markets bottomed only in March 2009.

But do this only if you have surplus that you can spare for 5 years at least and not less.

And remember, as the saying goes, the big money is not in the buying or selling, it is in the waiting!

So, if you have decided to invest, where should you be putting your money? If you invest in the markets directly, then index ETFs are an option. Otherwise, choose large-cap funds such as ICICI Pru Focused Bluechip, UTI Equity or HDFC Sensex Index Plus.

madam,

good to hear you and have the wisdom .thanks for the article at the appropriate time.

madam,

good to hear you and have the wisdom .thanks for the article at the appropriate time.

Good article. But this time around we need to consider : Syria war and brightening (frightening for us) US economy and the forthcoming Indian elections and the populist food bill. All the four factors read negative for Indian stocks. Debt is already down and bleeding. The only bright spot is gold . Realty is poised to come down sooner than later.

After factoring all the above, I prefer to invest, albeit slowly, in the US markets. How can i invest in the US economy which will give me diversification? Why don’t FundsIndia have some blue chip US stocks where I can invest?

Thanks

HI Mohan, Thanks for sharing your inputs. I think the global political opinion is that Syrian issue is not too big in the scheme of things (like Iraq etc.) to cause economic turmoil, expect perhaps to the extent of some flight to safety (gold went up a bit in dollar terms). Yes, elections and food bill hold their uncertainty, which is why the economy may not have bottomed out as yet.

I would suggest you keep exposure to US for the purpose of diversification. In the long term, growth markets such as India ought to outperform. Isn;t it easy for you to invest in international funds that take exposure to the US than directly look at US stks? You hav t least 3 fund hosues offering it, besides a Nasdq 100 ETF from Motital owsal. Buying foreign stks would require a sizeable deposit with most brokerages, besides havign to track the,. Funds offer easier and cheaper alternatives. thanks

I think it is important for domestic investors to be very cautious of US funds offered by Indian AMCs, especially if they have larger amounts to invest. Anybody with more than 10,000$ can go for a discount broker like Interactive Brokers who have an office in India. Moreover, one needn’t track foreign markets. One could simply buy the ETFs available on US exchanges, which are much better than our domestic ETFs, offering excellent liquidity and expense ratios. Schwab and Vanguard US total market ETFs which invest in the entire US market are 0.05% or 0.04% expense ratio.

Why would somebody buy Nasdaq 100 or US active funds for an expense ratio 20-40 times that? This is plain and simple greed on the part of domestic AMCs. It is exploitation of investor ignorance. Active management may work in India, but for the last two decades in US, the majority of active funds have not beat the total market funds or the indices such as S&P 500, let alone provide alpha. Buyer beware.

It is disappointing to see that distributors and fund houses are not pointing out these caveats. If somebody says, I don’t have 10,000$ or the patience to open a brokerage account, fine. Great. That’s an ethical sell. But if people don’t know the alternatives out there and domestic AMCs are charging high expense ratios to feed their active funds in US which in turn have higher expense ratios than passive funds with high probability of negative alpha – that’s unethical.

Hello Adithya,investors who have the money, time and knowledge about foreign markets can consider investing directly. But we are talking of small retail investors here and not HNI. $10,000 i a LOT of money. Shall we say that is a good few lakhs in rupee terms. And we are talking about investors whose annual income is the figure.

Most brokerages require a hefty deposit to do foreign equities. Can you imagine investors buying 5000 rs of intl. equities? Fund houses charge higher expense when they actively manage it (not all of them are feeder funds) and lower exp. otherwise. Of course there is a cost involved in all this too, so do not forget that. And you may check some of performers from Franklin and JP Morgan stable, they have indeed beaten the benchmarks. hence, that ‘US active funds do not outperform’ is a story that is used to make headlines in the media. Yes, not too many but enough to choose from. Thanks.

Dear Vidya, first let me say that I am a fan of your writing, and of FundsIndia as an organization. I recommend it to my friends as I really believe there is a value-add for the retail investor. I do a significant portion of my investments through FundsIndia. So it is out of admiration for your organization, not anything else, that I feel this debate is important.

Let me present the evidence, and then you tell me if I am wrong, and the Indian AMCs are being ethical and fair.

Firstly, on average, 65% of US active funds fail to even match their US benchmarks over a five year period. This is true for all large-caps funds for the last 15 years since 1998. But as you say, why don’t we look at the winners?

That brings me to the second point: the persistence in winners is very low. The top 20% funds based on past 5 year track record went on to show stunning randomness in performance: 58% of those funds slipped to the bottom 40% of their category or simply died out in the subsequent 5 year period. Only 15% of the top funds in the first period remained at the top in the second period. In other words, even if the NFOs recommended by the Indian press are feeding into US winner funds, there is an 85% chance that those guys will no longer be at the top in the next five years, and thus fail to beat their benchmarks. Is that a good probability to bet on? Especially, if, as you say, most investors in these funds are aam aadmi people who cannot afford more than 5000 or 10000 to invest.

Could it be that this statistic reflects just one bad decade for mutual funds, and that the story is different in other decades? No. That past winners do not predict future winners, is demonstrated across decades by Sharpe (1966 study) & Jensen (1968); Carhart (1997), Fama & French (2010). These are Nobel Prize winning experts in the field of finance, and they have looked at the actual performance data of mutual funds. Are they wrong?

Third, what if we, or the Indian AMCs, exit the fund if it underperforms a year or two later? Wouldn’t that cancel out the second point? No. Because if you exit a fund and enter another active fund, based on updated track-record of outperformance, your results are the same or worse (Goyal & Wahal study, 2008). Whichever way you look at it, Vidya, the statistics are ugly for active management. And it’s not news headlines we’re talking about. These are good quality analytical studies based on data, and there are more studies.

All this is stuff our Indian AMCs know. Anybody can google these studies, and search for contradictory evidence, and prove me wrong. If I am wrong, I will be delighted so that I too can benefit from the alpha.

Finally, our Indian AMCs could have recovered their costs and made ample profits by doing the smart thing – buying a Vanguard ETF on the US exchange, which has a 0.05% expense ratio, and charging the Indian retail investor 1% total expense ratio. This provides a 0.95% expense ratio spread to cover costs and make loads of profits. The fact that they have decided this is not enough profit – can anybody give me a good reason for that? Costs should not be incurred without reason.

In the face of all these statistics, are you still confident that JP Morgan & Templeton have picked winners for the forward-looking period? Do you still believe that Indian AMCs have done the best they can for our small-amount investors? Are you still comfortable recommending active management, or do you wish they had picked passive management? In future articles, are you as an organization going to include such caveats when you recommend these funds?

Data quote from: http://pressroom.vanguard.com/nonindexed/3.31.2013_The_Case_for_index_fund_investing.pdf

Hi Aditya, Really appreciate the time you have taken and the info. collected to put out your comment. this can be a post by itself 🙂

I do not refute the performance of active funds in the US and also the under performance of many Indian intl. funds in India (mostly started as theme funds). A few though, have successfully beaten their res. benchmark. And yes, ETFs will def. come slowly. Motilal Oswal has it for Nasdaq 100 and more will come.

My only point is that of the feasible options today, intl. funds are the most convenient when you have less money in hand and want to participate. Also, I would like you to note, we do not have ‘recommendations’ on international funds” in any portfolios that we are requested to build. we only highlight features and leave it at that.

@ Vidya: My respect for this blog has shot up a notch. You guys really are fair. A lot of ‘sales’ oriented people in the industry wouldn’t have published the comment. My enthusiastic recommendation of FundsIndia to my friends is vindicated 🙂

As for the time spent on the comment, it’s worth it. You guys put a lot of thought into your articles. It’s only fair that readers return the effort & backup their opinions with data. We all gain from the discussion.

Good article. But this time around we need to consider : Syria war and brightening (frightening for us) US economy and the forthcoming Indian elections and the populist food bill. All the four factors read negative for Indian stocks. Debt is already down and bleeding. The only bright spot is gold . Realty is poised to come down sooner than later.

After factoring all the above, I prefer to invest, albeit slowly, in the US markets. How can i invest in the US economy which will give me diversification? Why don’t FundsIndia have some blue chip US stocks where I can invest?

Thanks

HI Mohan, Thanks for sharing your inputs. I think the global political opinion is that Syrian issue is not too big in the scheme of things (like Iraq etc.) to cause economic turmoil, expect perhaps to the extent of some flight to safety (gold went up a bit in dollar terms). Yes, elections and food bill hold their uncertainty, which is why the economy may not have bottomed out as yet.

I would suggest you keep exposure to US for the purpose of diversification. In the long term, growth markets such as India ought to outperform. Isn;t it easy for you to invest in international funds that take exposure to the US than directly look at US stks? You hav t least 3 fund hosues offering it, besides a Nasdq 100 ETF from Motital owsal. Buying foreign stks would require a sizeable deposit with most brokerages, besides havign to track the,. Funds offer easier and cheaper alternatives. thanks

I think it is important for domestic investors to be very cautious of US funds offered by Indian AMCs, especially if they have larger amounts to invest. Anybody with more than 10,000$ can go for a discount broker like Interactive Brokers who have an office in India. Moreover, one needn’t track foreign markets. One could simply buy the ETFs available on US exchanges, which are much better than our domestic ETFs, offering excellent liquidity and expense ratios. Schwab and Vanguard US total market ETFs which invest in the entire US market are 0.05% or 0.04% expense ratio.

Why would somebody buy Nasdaq 100 or US active funds for an expense ratio 20-40 times that? This is plain and simple greed on the part of domestic AMCs. It is exploitation of investor ignorance. Active management may work in India, but for the last two decades in US, the majority of active funds have not beat the total market funds or the indices such as S&P 500, let alone provide alpha. Buyer beware.

It is disappointing to see that distributors and fund houses are not pointing out these caveats. If somebody says, I don’t have 10,000$ or the patience to open a brokerage account, fine. Great. That’s an ethical sell. But if people don’t know the alternatives out there and domestic AMCs are charging high expense ratios to feed their active funds in US which in turn have higher expense ratios than passive funds with high probability of negative alpha – that’s unethical.

Hello Adithya,investors who have the money, time and knowledge about foreign markets can consider investing directly. But we are talking of small retail investors here and not HNI. $10,000 i a LOT of money. Shall we say that is a good few lakhs in rupee terms. And we are talking about investors whose annual income is the figure.

Most brokerages require a hefty deposit to do foreign equities. Can you imagine investors buying 5000 rs of intl. equities? Fund houses charge higher expense when they actively manage it (not all of them are feeder funds) and lower exp. otherwise. Of course there is a cost involved in all this too, so do not forget that. And you may check some of performers from Franklin and JP Morgan stable, they have indeed beaten the benchmarks. hence, that ‘US active funds do not outperform’ is a story that is used to make headlines in the media. Yes, not too many but enough to choose from. Thanks.

Dear Vidya, first let me say that I am a fan of your writing, and of FundsIndia as an organization. I recommend it to my friends as I really believe there is a value-add for the retail investor. I do a significant portion of my investments through FundsIndia. So it is out of admiration for your organization, not anything else, that I feel this debate is important.

Let me present the evidence, and then you tell me if I am wrong, and the Indian AMCs are being ethical and fair.

Firstly, on average, 65% of US active funds fail to even match their US benchmarks over a five year period. This is true for all large-caps funds for the last 15 years since 1998. But as you say, why don’t we look at the winners?

That brings me to the second point: the persistence in winners is very low. The top 20% funds based on past 5 year track record went on to show stunning randomness in performance: 58% of those funds slipped to the bottom 40% of their category or simply died out in the subsequent 5 year period. Only 15% of the top funds in the first period remained at the top in the second period. In other words, even if the NFOs recommended by the Indian press are feeding into US winner funds, there is an 85% chance that those guys will no longer be at the top in the next five years, and thus fail to beat their benchmarks. Is that a good probability to bet on? Especially, if, as you say, most investors in these funds are aam aadmi people who cannot afford more than 5000 or 10000 to invest.

Could it be that this statistic reflects just one bad decade for mutual funds, and that the story is different in other decades? No. That past winners do not predict future winners, is demonstrated across decades by Sharpe (1966 study) & Jensen (1968); Carhart (1997), Fama & French (2010). These are Nobel Prize winning experts in the field of finance, and they have looked at the actual performance data of mutual funds. Are they wrong?

Third, what if we, or the Indian AMCs, exit the fund if it underperforms a year or two later? Wouldn’t that cancel out the second point? No. Because if you exit a fund and enter another active fund, based on updated track-record of outperformance, your results are the same or worse (Goyal & Wahal study, 2008). Whichever way you look at it, Vidya, the statistics are ugly for active management. And it’s not news headlines we’re talking about. These are good quality analytical studies based on data, and there are more studies.

All this is stuff our Indian AMCs know. Anybody can google these studies, and search for contradictory evidence, and prove me wrong. If I am wrong, I will be delighted so that I too can benefit from the alpha.

Finally, our Indian AMCs could have recovered their costs and made ample profits by doing the smart thing – buying a Vanguard ETF on the US exchange, which has a 0.05% expense ratio, and charging the Indian retail investor 1% total expense ratio. This provides a 0.95% expense ratio spread to cover costs and make loads of profits. The fact that they have decided this is not enough profit – can anybody give me a good reason for that? Costs should not be incurred without reason.

In the face of all these statistics, are you still confident that JP Morgan & Templeton have picked winners for the forward-looking period? Do you still believe that Indian AMCs have done the best they can for our small-amount investors? Are you still comfortable recommending active management, or do you wish they had picked passive management? In future articles, are you as an organization going to include such caveats when you recommend these funds?

Data quote from: http://pressroom.vanguard.com/nonindexed/3.31.2013_The_Case_for_index_fund_investing.pdf

Hi Aditya, Really appreciate the time you have taken and the info. collected to put out your comment. this can be a post by itself 🙂

I do not refute the performance of active funds in the US and also the under performance of many Indian intl. funds in India (mostly started as theme funds). A few though, have successfully beaten their res. benchmark. And yes, ETFs will def. come slowly. Motilal Oswal has it for Nasdaq 100 and more will come.

My only point is that of the feasible options today, intl. funds are the most convenient when you have less money in hand and want to participate. Also, I would like you to note, we do not have ‘recommendations’ on international funds” in any portfolios that we are requested to build. we only highlight features and leave it at that.

@ Vidya: My respect for this blog has shot up a notch. You guys really are fair. A lot of ‘sales’ oriented people in the industry wouldn’t have published the comment. My enthusiastic recommendation of FundsIndia to my friends is vindicated 🙂

As for the time spent on the comment, it’s worth it. You guys put a lot of thought into your articles. It’s only fair that readers return the effort & backup their opinions with data. We all gain from the discussion.

Its a good take on the current situation maam.

Apart from continuing with our SIPs, if you have a lumpsum amount with you and wish to invest without bothering it for 10 years (please, I am a value investor, shortest tenure of equity investment is 10 years for me, on the lower side). Then you may consider putting the same in a liquid/short term debt funds (with exceptionally low expense ratio) and transfer the same periodically to an equity fund. During gloom, times you would get little bit return from the liquid funds and during the so called ‘boom’ times (i consider those time hyperactive exuberant human behaviour) you get more from your equity investments.

PS: Please choose growth option in both funds. Div option simply defeats the long term investing idea. Remember div payout is simply your money coming back to from the AMC.

Its a good take on the current situation maam.

Apart from continuing with our SIPs, if you have a lumpsum amount with you and wish to invest without bothering it for 10 years (please, I am a value investor, shortest tenure of equity investment is 10 years for me, on the lower side). Then you may consider putting the same in a liquid/short term debt funds (with exceptionally low expense ratio) and transfer the same periodically to an equity fund. During gloom, times you would get little bit return from the liquid funds and during the so called ‘boom’ times (i consider those time hyperactive exuberant human behaviour) you get more from your equity investments.

PS: Please choose growth option in both funds. Div option simply defeats the long term investing idea. Remember div payout is simply your money coming back to from the AMC.

A wonderful article, people know this but keep missing from their memory, it’s hard to control human brain.

My simple strategy is continue with SIP’s and invest surplues (i don’t invest equal amount of SIP though) amount when you see Nifty falling 2-3 % a day.

I have observed this over a period of 6 months (short duration though), and found that my Surplus investment is in green while my SIP’s return is in RED…. so when market bottoms out and takes a U turn i will have my surplus amount portfolio acting as a Satellite portfolio, while my Core will remain as it is (From my SIP’s).

I have taken this strategy on my own after reading a few articles on Core and Satellite aproach.

Dear Vidya madam, can you point me out few good funds to have in a Satellite portfolio.

As of today i have Reliance Pharma (I agree with the risks a sectoral fund has) and IDFC Premier (for small and Mid cap).

Shall i continue with these or are there any better options.

Sorry for the legthy post though.

Thanks in anticipation,

Sunil.

Hello Sunil, IDFC Premier should actually be a core holding in my opinion. A core portfolioc an certainly do with some solid mid-cap fund. International funds or more aggressive midcaps like Magnum emerging Businesses or opportunity funds such as Reliance Equity Opportunities can also be a satellite holding. Tks.

Dear Vidya,

Many thanks for the response.

Regards,

Sunil.

“Those who treat stock market as casino will be treated as gamblers”

– A great investor (not me)

At this time, we should have 50% allocation to equity, the next 6 to 9 months are not good for Indian economy , clearly the micro numbers are not good, these all are sign of economic slow down and some serious problem. At this time 50 – 50 % strategy works better , allocate your 50% funds in equity and rest in Liquid funds, any dip of 5% or more in equity allocation is the best time to re balancing , when equity allocation goes below 45% , put some more money in equity and bring the allocation to 50 -50 % in Equity and Debt. In long run it will work best for you. Because Indian equity is not going into bull run at least less than 1 to 2 years. Things takes time to improve at ground level.

Hi Kuldeep, Thanks for sharing your thoughts. Vidya

Hi,

Looking at how PSU bank stocks have fared this year, I am tempted to buy these shares in large quantities. Do you think it is a good idea? Mr. Rakesh Jhunjhunwala says they have low earnings potential and thus would not recommend a buy. What is your opinion on this matter?

Hello Shreyas, I think you shoudl wait for september earnings of PSU banks and let the NPAs be known before you consider investing. Vidya

Is this time right for a new player like me to invest in SIP funds…if ‘yes’ then which funds should i choose and if ‘no’ the when i should start with SIP.Please kindly help me on this query

Anuj, Volatile markets amke for good starting points for SIP investors in equity. So the answer is a ‘yes’. But I will be constrained from answering portfolio queries here. Pl. route it through the ‘Ask Advisor’ feature available for free to all FundsIndia investors. We will help you build a portfolio that suits your time line, risk and savings and also review the anytime on request. Thanks.

Ok thanks Vidya… will seek there advice when i finish paperwork and open my account

Hi,

Looking at how PSU bank stocks have fared this year, I am tempted to buy these shares in large quantities. Do you think it is a good idea? Mr. Rakesh Jhunjhunwala says they have low earnings potential and thus would not recommend a buy. What is your opinion on this matter?

Hello Shreyas, I think you shoudl wait for september earnings of PSU banks and let the NPAs be known before you consider investing. Vidya

Is this time right for a new player like me to invest in SIP funds…if ‘yes’ then which funds should i choose and if ‘no’ the when i should start with SIP.Please kindly help me on this query

Anuj, Volatile markets amke for good starting points for SIP investors in equity. So the answer is a ‘yes’. But I will be constrained from answering portfolio queries here. Pl. route it through the ‘Ask Advisor’ feature available for free to all FundsIndia investors. We will help you build a portfolio that suits your time line, risk and savings and also review the anytime on request. Thanks.

Ok thanks Vidya… will seek there advice when i finish paperwork and open my account

At this time, we should have 50% allocation to equity, the next 6 to 9 months are not good for Indian economy , clearly the micro numbers are not good, these all are sign of economic slow down and some serious problem. At this time 50 – 50 % strategy works better , allocate your 50% funds in equity and rest in Liquid funds, any dip of 5% or more in equity allocation is the best time to re balancing , when equity allocation goes below 45% , put some more money in equity and bring the allocation to 50 -50 % in Equity and Debt. In long run it will work best for you. Because Indian equity is not going into bull run at least less than 1 to 2 years. Things takes time to improve at ground level.

Hi Kuldeep, Thanks for sharing your thoughts. Vidya

“Those who treat stock market as casino will be treated as gamblers”

– A great investor (not me)

Dear Vidya,

Many thanks for the response.

Regards,

Sunil.

A wonderful article, people know this but keep missing from their memory, it’s hard to control human brain.

My simple strategy is continue with SIP’s and invest surplues (i don’t invest equal amount of SIP though) amount when you see Nifty falling 2-3 % a day.

I have observed this over a period of 6 months (short duration though), and found that my Surplus investment is in green while my SIP’s return is in RED…. so when market bottoms out and takes a U turn i will have my surplus amount portfolio acting as a Satellite portfolio, while my Core will remain as it is (From my SIP’s).

I have taken this strategy on my own after reading a few articles on Core and Satellite aproach.

Dear Vidya madam, can you point me out few good funds to have in a Satellite portfolio.

As of today i have Reliance Pharma (I agree with the risks a sectoral fund has) and IDFC Premier (for small and Mid cap).

Shall i continue with these or are there any better options.

Sorry for the legthy post though.

Thanks in anticipation,

Sunil.

Hello Sunil, IDFC Premier should actually be a core holding in my opinion. A core portfolioc an certainly do with some solid mid-cap fund. International funds or more aggressive midcaps like Magnum emerging Businesses or opportunity funds such as Reliance Equity Opportunities can also be a satellite holding. Tks.