“Should I go for growth option or take out the dividends in my fund?” – is a question frequently asked by many of you, when venturing into mutual fund investments. We have already discussed how dividends are paid out and how your NAV reacts in our last week’s article “What are dividend and growth options in a mutual fund?”

We also summarized what to choose. This week, we elaborate on which option to go for, based on your cash flow need.

Which one to choose?

Your cash flow requirements and tax efficiency will be the two factors that will determine whether you need to go for dividend or growth option. Let us look at these within the category of equity and debt funds.

Equity funds

Equity funds are meant for the long term. Your reason for choosing an equity fund must be to build wealth towards some goal which is perhaps at least few years away. Equity funds cannot be used to generate near term income options for you.

That simply means you should stay invested in an equity fund and not take the cash out (unless you will invest the dividends back diligently)to help compounding work for you.

Since, long-term capital gains are free of tax, the solution here is simple: As a general principle, go for growth or dividend reinvestment in equity funds.

But there are exceptions: One, in case of theme funds or sector funds that you hold tactically, you may wish to either opt for dividend payouts or book profits as the fortunes of themes can take a turn after one good cycle.Two, in case of ELSS, given that your money is locked in, you may wish to go for a dividend payout if you are in say your 50s and are a bit averse to risk and want some profits in cash during the lock-in.

Young investors should allow their tax saving fund to grow with growth option.

Debt funds

This category gets a bit tricky because the dividend suffers dividend distribution tax (DDT).DDT is nothing but the tax on your dividend. While it is not deducted on your dividend directly in your hands, it is reduced from your NAV.

Given this tax component, dividend payout and dividend reinvestment can be tax inefficient. Let us look at whether you need to opt for it.

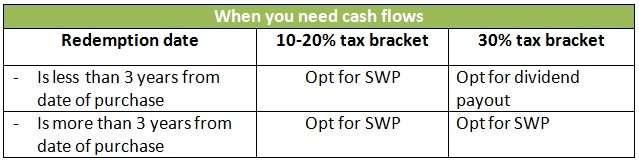

1. You need some cash flows from your debt fund:In this case, you can choose the dividend payout or the systematic withdrawal plan (SWP) under growth option. Look at the table below. The SWP is a clear winner for those in the 10% and 20% tax brackets. But please ensure that you do not end up paying exit load. Opt for SWP post the exit load period if you wish to avoid the load.

Those in the 30% tax bracket, can go for dividend payout, if you intend to hold the fund for less than three years. But if you are invested for more than 3 years and redeem post that then growth option makes sense, since you will get capital gains indexation benefit. In such a case go for SWP for regular cash flows. Each such redemption will get capital gain indexation benefit if your investment is over 3 years old.

Remember, switching between options will also unnecessarily entail capital gains tax if you have profits. Hence, get your investment time frame right when you start your investment.

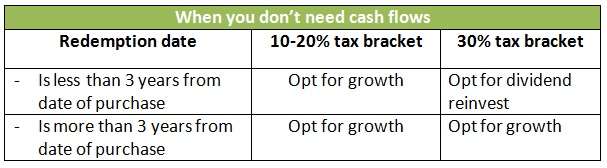

- You don’t need cash flows from your debt fund:In this case, dividend payout and SWP are not needed since you have no cash flow need.

You therefore have 2 options – to go for growth or dividend reinvestment. Look at the table below – growth option scores in most cases, except when you are in the 30% tax bracket and redeem in less than 3 years.

This will be true in case of liquid funds or ultra-short-term funds that you may park for a short while. In that case you will suffer DDT of 28.33% (including surcharge and cess) on the dividend reinvested. This will be slightly lower than the income tax slab of 30.9% (including cess).

Consider your fresh investments through the above routes. But if you make your switches now,do take into account the exit load and the capital gains, (will vary for each fund) if any,you may suffer on the fund now.

Dividend amount can be reinvested and further tax deduction in the new financial year could be claimed. It is really beneficial for all those in the braket of 30% or 20% tax.

Kaushika, most people do not reinvest their dividends. It lies in their bank account 🙂 Also it is often very small an amount to be reinvested. If you mean dividend reinvestment option, it still suffers DDT. Vidya

Dividend amount can be reinvested and further tax deduction in the new financial year could be claimed. It is really beneficial for all those in the braket of 30% or 20% tax.

Kaushika, most people do not reinvest their dividends. It lies in their bank account 🙂 Also it is often very small an amount to be reinvested. If you mean dividend reinvestment option, it still suffers DDT. Vidya

I am existing client in FUNDSINDIA and it’s been almost two years here but let me tell you that this portal till today has no such portion made avl to his clients where they can put their experience with fundsindia. its very slow and customer support is so lethargic. If you ask a simple query today that how to resume my existing SIPs they would reply you – we will revert back and it may take time more than 24 hours also. Customer support is having no technical know-how about some basics of MUTUAL FUNDS – the only time they show urgency or agility, when you are about to open your account first time. very poor services. Highly disappointed with the lackadaisical approach of fundsindia.

Hello sir,

Thanks for your comment, and sorry for your bad experience. Our target for responding to a customer query or issue is within 1 business day. In days such as yesterday, when the teams would have had to deal with 2-3 days of pending customer queries, this time line would have become extended. Else, our support teams respond within a few hours at best. Regarding mutual funds, many of our support people have sufficient mutual fund knowledge, but I admit that not all of them do. I would urge you to write to advisor@fundsindia.com if you have questions about your investments and/or need advice.

thanks,

Srikanth

Now thats what I call customer service! A top brass responding directly to a blog comment and acknowledging a potential delay in response time. I’ve never dealt with their customer service, but their advisors and those writing these blog posts are clearly very knowledgeable and insightful about mutual funds and the markets in general.

Agree !!

They provide prompt response !! Satisfied till now!

I am existing client in FUNDSINDIA and it’s been almost two years here but let me tell you that this portal till today has no such portion made avl to his clients where they can put their experience with fundsindia. its very slow and customer support is so lethargic. If you ask a simple query today that how to resume my existing SIPs they would reply you – we will revert back and it may take time more than 24 hours also. Customer support is having no technical know-how about some basics of MUTUAL FUNDS – the only time they show urgency or agility, when you are about to open your account first time. very poor services. Highly disappointed with the lackadaisical approach of fundsindia.

Hello sir,

Thanks for your comment, and sorry for your bad experience. Our target for responding to a customer query or issue is within 1 business day. In days such as yesterday, when the teams would have had to deal with 2-3 days of pending customer queries, this time line would have become extended. Else, our support teams respond within a few hours at best. Regarding mutual funds, many of our support people have sufficient mutual fund knowledge, but I admit that not all of them do. I would urge you to write to advisor@fundsindia.com if you have questions about your investments and/or need advice.

thanks,

Srikanth

Now thats what I call customer service! A top brass responding directly to a blog comment and acknowledging a potential delay in response time. I’ve never dealt with their customer service, but their advisors and those writing these blog posts are clearly very knowledgeable and insightful about mutual funds and the markets in general.

Agree !!

They provide prompt response !! Satisfied till now!

Hello Madam / Sir

I have invested in some liquid funds in lump sum for emergency need in Dividend-Reinvestment option. I would like to know if growth option fetches around 8% annual return, what is the return in dividend-reinvestment option. And secondly when I redeem, Shall I have to pay tax?

Hello Sir,

In debt funds, dividend reinvestment will be lower than growth option return since DDT of 28.3% is lost every time a dividend is declared. For any redemption less than 3 years, if you have capital gains, you will pay your slab rate tax. For over 3 years, it is 20% but with indexation benefit on cost. thanks, Vidya

Thanks Vidya for quick reply….

Hello Madam / Sir

I have invested in some liquid funds in lump sum for emergency need in Dividend-Reinvestment option. I would like to know if growth option fetches around 8% annual return, what is the return in dividend-reinvestment option. And secondly when I redeem, Shall I have to pay tax?

Hello Sir,

In debt funds, dividend reinvestment will be lower than growth option return since DDT of 28.3% is lost every time a dividend is declared. For any redemption less than 3 years, if you have capital gains, you will pay your slab rate tax. For over 3 years, it is 20% but with indexation benefit on cost. thanks, Vidya

Thanks Vidya for quick reply….

This is an interesting article, thanks for putting this together. I fall in the 30% bracket, can you help with a comparative between FD / KVP / NSC and Debt Funds / Hybrid Funds for the efficiency and returns (post tax) point of view. Also for example if one is trying to build a corpus, for emergency what is advisable – park in FD (higher liquidity) or in Debt Funds.

Prithviraj,

Comparisons hardly needed for FD. At 7.5% FD rate it will be lower than debt funds especially in the high tax bracket and if you plan to hold for 3 years. KVP is an outdated product at 7.8% return now, please leave it. NSC, if you want to invest for tax purpose and are ok with 5 year lock in you may. For regular saving purpose go with debt funds.

Vidya

This is an interesting article, thanks for putting this together. I fall in the 30% bracket, can you help with a comparative between FD / KVP / NSC and Debt Funds / Hybrid Funds for the efficiency and returns (post tax) point of view. Also for example if one is trying to build a corpus, for emergency what is advisable – park in FD (higher liquidity) or in Debt Funds.

Prithviraj,

Comparisons hardly needed for FD. At 7.5% FD rate it will be lower than debt funds especially in the high tax bracket and if you plan to hold for 3 years. KVP is an outdated product at 7.8% return now, please leave it. NSC, if you want to invest for tax purpose and are ok with 5 year lock in you may. For regular saving purpose go with debt funds.

Vidya

My father has recently retired and received hi PF amount. We wan to invest the same in low risky funds and hence high rated debt funds. Monthly income requirement is not very high as he still receives his pension. Should we go for the dividend option or the growth option ? Also, would you suggest some good rated debt funds with low risk and decent returns (FD+ returns) ?

Anubhav, if he is not tax payer or is in the 10 or 20% option, he should go for growth option if he is investing for less than 3 years. if he is investing for over 3 years, then growth is the better option as he will get indexation benefit. For Fund recommendations, kindly send in your queries through you FundsIndia account.

Vidya

My father has recently retired and received hi PF amount. We wan to invest the same in low risky funds and hence high rated debt funds. Monthly income requirement is not very high as he still receives his pension. Should we go for the dividend option or the growth option ? Also, would you suggest some good rated debt funds with low risk and decent returns (FD+ returns) ?

Anubhav, if he is not tax payer or is in the 10 or 20% option, he should go for growth option if he is investing for less than 3 years. if he is investing for over 3 years, then growth is the better option as he will get indexation benefit. For Fund recommendations, kindly send in your queries through you FundsIndia account.

Vidya